Khanchit Khirisutchalual

Investment Thesis

Even though the inflation rate in the U.S. has decreased slightly in the past months, it continues to be relatively high when compared to the historical average inflation rate of the country: while the inflation rate was 7.7% in October 2022, it was 7.1% in November 2022 and 6.5% in December 2022.

The annual average inflation rate from 1914 until 2022, however, was 3.29%. These numbers show us that the current inflation rate is still significantly higher than its average. As a result, investors should search for ways to protect their money against inflation.

In order to help you protect your investment portfolio against inflation, I have selected 5 companies that I consider to be excellent picks when aiming to hedge against inflation. All of these companies have the following characteristics in common:

- Strong competitive advantages that provide an economic moat

- Among the leading companies in its Industry

- A strong brand image that enables the company to pass on higher costs that result from inflation to its customers

- Strong financials in order to better deal with higher costs

- Attractive in terms of risk and reward

- Attractive Valuation

- Pay its shareholders a dividend and have shown Dividend Growth for at least the past 5 years.

The 5 companies I have selected to help hedge your investment portfolio against inflation are as follows:

- PepsiCo, Inc. (NASDAQ:PEP)

- The Procter & Gamble Company (NYSE:PG)

- BlackRock, Inc. (NYSE:BLK)

- Apple Inc. (NASDAQ:AAPL)

- Visa Inc. (NYSE:V)

PepsiCo

Over the past decades, PepsiCo has managed to build a brand image that provides it with a strong competitive advantage over smaller competitors, thus enabling the company to pass on higher costs to its consumers. This is one of the reasons why I believe PepsiCo will be able to help hedge your investment portfolio against inflation.

Furthermore, I consider PepsiCo to currently be fairly valued: my opinion is based on the fact that its current P/E [FWD] Ratio of 24.39 is in line with its Average P/E [FWD] Ratio over the past 5 years (23.65). In addition to that, PepsiCo’s Valuation is slightly lower than its competitor Coca-Cola (NYSE:KO) (P/E [FWD] Ratio of 26.98).

Moreover, PepsiCo has shown higher Growth Rates in the past than its competitor: while PepsiCo’s Revenue Growth Rate [CAGR] over the past 5 years has been 5.66%, Coca-Cola’s has only been 2.56%. This provides us with another indicator that PepsiCo seems to be fairly valued at this moment of writing (since its valuation is lower, but its Growth Rate is higher than Coca-Cola).

PepsiCo pays its shareholders a Dividend Yield [FWD] of 2.68%. It can be highlighted that the company has been able to raise its Dividend with an Average Dividend Growth Rate of 7.39% over the past 5 years, providing us with evidence that the company is an attractive pick for dividend growth investors. When comparing PepsiCo’s Dividend Growth Rate of 7.39% with the one of Coca-Cola (3.53%), it is indicated that PepsiCo seems to be the slightly better pick for dividend growth investors in comparison to its rival.

The company’s Payout Ratio of 66.92% can be interpreted as a signal that it has enough room for further Dividend enhancements, at least in the near future, which serves as more evidence that the company is a good fit for dividend growth investors.

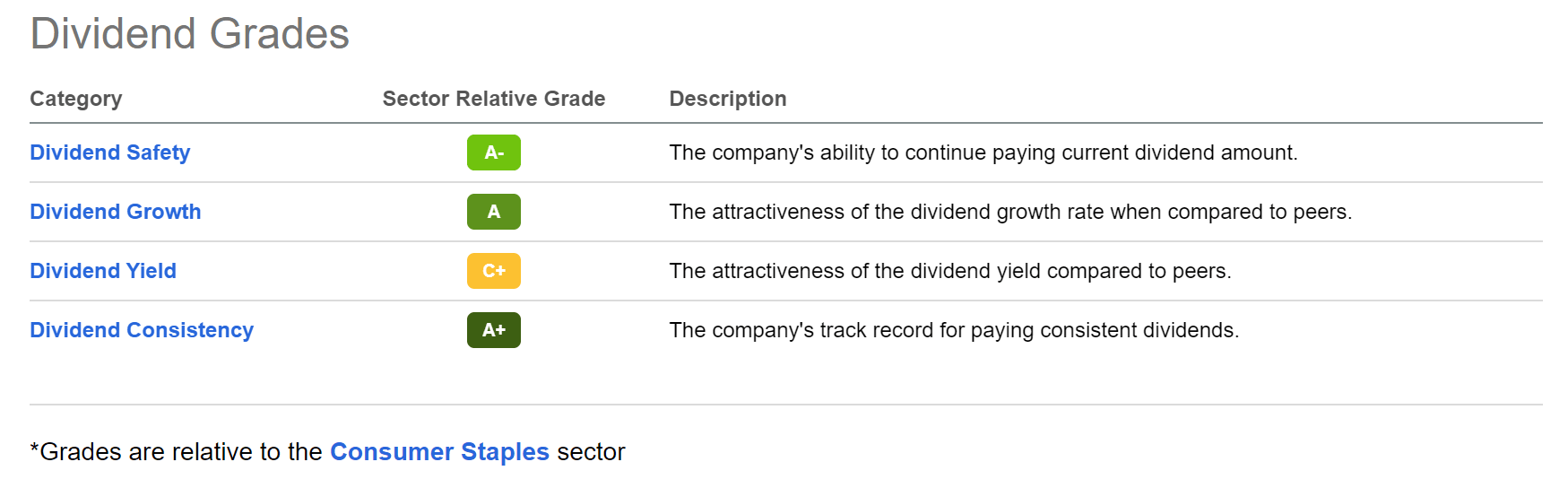

The Seeking Alpha Dividend Grades are a further indicator that PepsiCo is an attractive choice for those looking for Dividend Income and Dividend Growth. The company is rated with an A+ for Dividend Consistency, an A for Dividend Growth, and an A- for Dividend Safety. Only for Dividend Yield, is the company rated with a C+.

Source: Seeking Alpha

Furthermore, I would like to highlight that you can reduce the volatility of your investment portfolio by adding PepsiCo to it. This assumption is underlined by the fact that PepsiCo’s 24M Beta is 0.51 and its 60M Beta is 0.60.

Procter & Gamble

I consider Procter & Gamble to be a company that can help protect your investment portfolio against inflation. The company has a broad and well diversified product portfolio and due to the strong brand images of its products, it can pass on higher costs to its customers.

I currently consider Procter & Gamble to be fairly valued. The reason being that its P/E [FWD] Ratio of 25.02 is in line with its Average P/E [FWD] Ratio over the past 5 years (which is 23.59). In addition to that, Procter & Gamble’s P/E Ratio is slightly lower than competitors such as Colgate-Palmolive Company (NYSE:CL) (P/E [FWD] Ratio of 26.47) and similar to Unilever (NYSE:UL) (23.19). These are further indicators demonstrating that Procter & Gamble is currently fairly valued.

Procter & Gamble’s EBIT Margin [TTM] is 23.12%, underlying the company’s strong competitive position within its Industry. This is proven further by the fact that its EBIT Margin is 196.88% higher than the EBIT Margin of the Sector Median (which is only 7.79%).

When comparing the company’s current EBIT Margin of 23.12% with its Average EBIT Margin [TTM] over the past 5 years (22.62%), we can see that it has been able to increase its margins in that time period.

The company’s high Return on Equity of 32.29%, which is 205.03% above the Sector Median (10.59%), is another indicator of Procter & Gamble enormous Profitability and financial strength. All of this contributes to the fact that I consider the company to be an excellent choice in order to hedge against inflation.

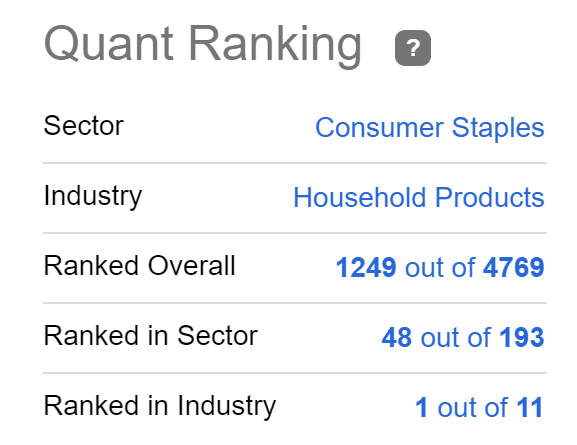

The Seeking Alpha Quant Ranking support my theory to currently rate Procter & Gamble as a buy: the company is ranked 1st out of 11 in the Household Products Industry and 48th out of 193 in the Consumer Staples Sector.

Source: Seeking Alpha

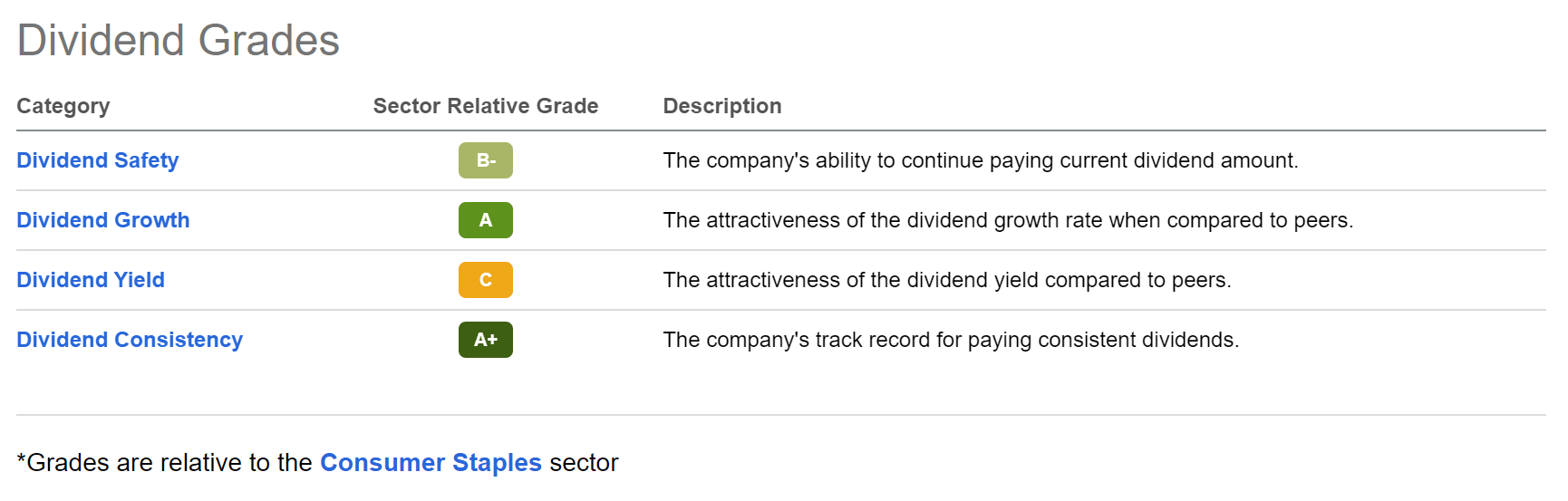

The Seeking Alpha Dividend Grades serve as another indicator that Procter & Gamble is a great pick for investors seeking Dividend Income and Dividend Growth: the company receives an A+ rating for Dividend Consistency, an A for Dividend Growth, a B- for Dividend Safety and a C for Dividend Yield.

Source: Seeking Alpha

Similar to PepsiCo, Procter & Gamble can also contribute to reducing the volatility of your investment portfolio: the company has a 24M Beta Factor of 0.58. This makes Procter & Gamble an appealing pick to not only hedge against inflation, but also to protect your portfolio against the next stock market crash.

BlackRock

In my opinion, BlackRock is an excellent base investment for any investor: it provides you with a relatively attractive Dividend Yield [FWD] of 2.61%, with Dividend Growth (Dividend Growth Rate [CAGR] of 12.52% over the past 10 years) and I consider the company to be an attractive pick when considering risk and reward.

When taking a closer look at BlackRock’s P/E [FWD] Ratio of 21.65, we can see that the company is currently fairly valued: the reason being that its P/E Ratio is only slightly higher than its Average P/E Ratio [FWD] over the past 5 years (19.13).

The company has an enormous financial strength: proof of this is its EBITDA Margin [TTM] of 38.55%. This is 78.68% higher than the EBITDA Margin [TTM) of the Sector Median (21.57%).

BlackRock’s Return on Equity [TTM] is 13.83%. If we compare the company’s Return on Equity with that of the Sector Median, we discover that it’s actually 19.70% above the Sector Median (ROE of the Sector Median is 11.56%). This provides evidence that the company is efficient in using shareholder’s equity with the aim of generating income. BlackRock’s financial strength is further underlined by its Aa3 credit rating by Moody’s and AA- credit rating by S&P.

Below you can find the Seeking Alpha Profitability Grades, which confirm, once again, BlackRock’s enormous financial strength.

Source: Seeking Alpha

Additionally, the company has proven in the past that it is a reliable dividend payer for its shareholders: the company has shown 13 consecutive years of Dividend Growth, providing us with a strong indicator that it’s an excellent fit for investors seeking Dividend Growth.

Apple

In my recent analysis on Apple, I discussed that I currently rate the company as an attractive buy, particularly due to its current high Free Cash Flow Yield [TTM] of 5.13%.

But this is only one of several reasons why I think Apple is an attractive buy and why I consider it to be among the companies that can protect your investment portfolio against inflation: it is ranked as the number 1 brand in the world in terms of brand value, providing the company with an enormous competitive advantage (among other factors, such as its high customer loyalty and its own eco-system, etc.) and enabling it to pass on higher costs to its customers that may incur as a result of inflation.

In that previous analysis on Apple, I also explained that I currently consider the company to be undervalued. Proof of this is the fact that my DCF Model shows an upside of 10.3%. Furthermore, this model indicates a compound annual rate of return of approximately 11% for Apple at the company’s current stock price, making it an excellent choice when considering risk and reward from my point of view.

When comparing Apple to some of its competitors, my theory of it having an attractive current Valuation is supported: while Apple currently has a P/E [FWD] Ratio of 21.90, Microsoft’s (NASDAQ:MSFT) is 24.73 and Netflix’s (NASDAQ:NFLX) is 31.87, indicating that Apple’s Valuation is currently lower than those competitors.

Furthermore, Apple is ahead of competitors such as Dell (NYSE:DELL) and HP (NYSE:HPQ) when it comes to Growth: Apple’s EPS Diluted Growth Rate [CAGR] over the past 3 Years is 27.18%, which is significantly higher than Dell (-21.83%) or HP (13.79%): these numbers indicate that Apple has been able to raise its earnings at significantly higher rates than these competitors and I expect the company to continue doing so in the near future: the reasons for that are its strong competitive advantages and high custumer loyalty.

All these factors contribute to the fact that I consider Apple to be an excellent choice to help you protect your investment portfolio against inflation.

Visa

Visa is one of my favorite choices when searching for companies to hedge your investment portfolio against inflation. The reason being that the company benefits from increasing prices due to the fact that it charges transaction fees that earn a percentage of the revenue generated by the credit and debit cards it issues.

Several metrics can serve as strong indicators that Visa disposes of an excellent competitive position and has strong financials: it has an EBITDA [TTM] Margin of 70.35%, which is 507.78% above the Sector Median (11.58%). Furthermore, its Net Income Margin [TTM] is 51.03%, which is 1,483.71% above the Sector Median (3.22%), underlying, once again, the company’s financial strength.

Furthermore, I see Visa being on track when it comes to Growth: the company has shown an EBITDA Growth Rate [FWD] of 15.12%, which is 21.94% above the Sector Median (12.40%). In addition to that, its EPS Diluted Growth Rate [FWD] of 17.94% is 37.58% above the Sector Median (13.06%), indicating that the company has been able to increase its earnings at a significantly higher rate when compared to its competitors.

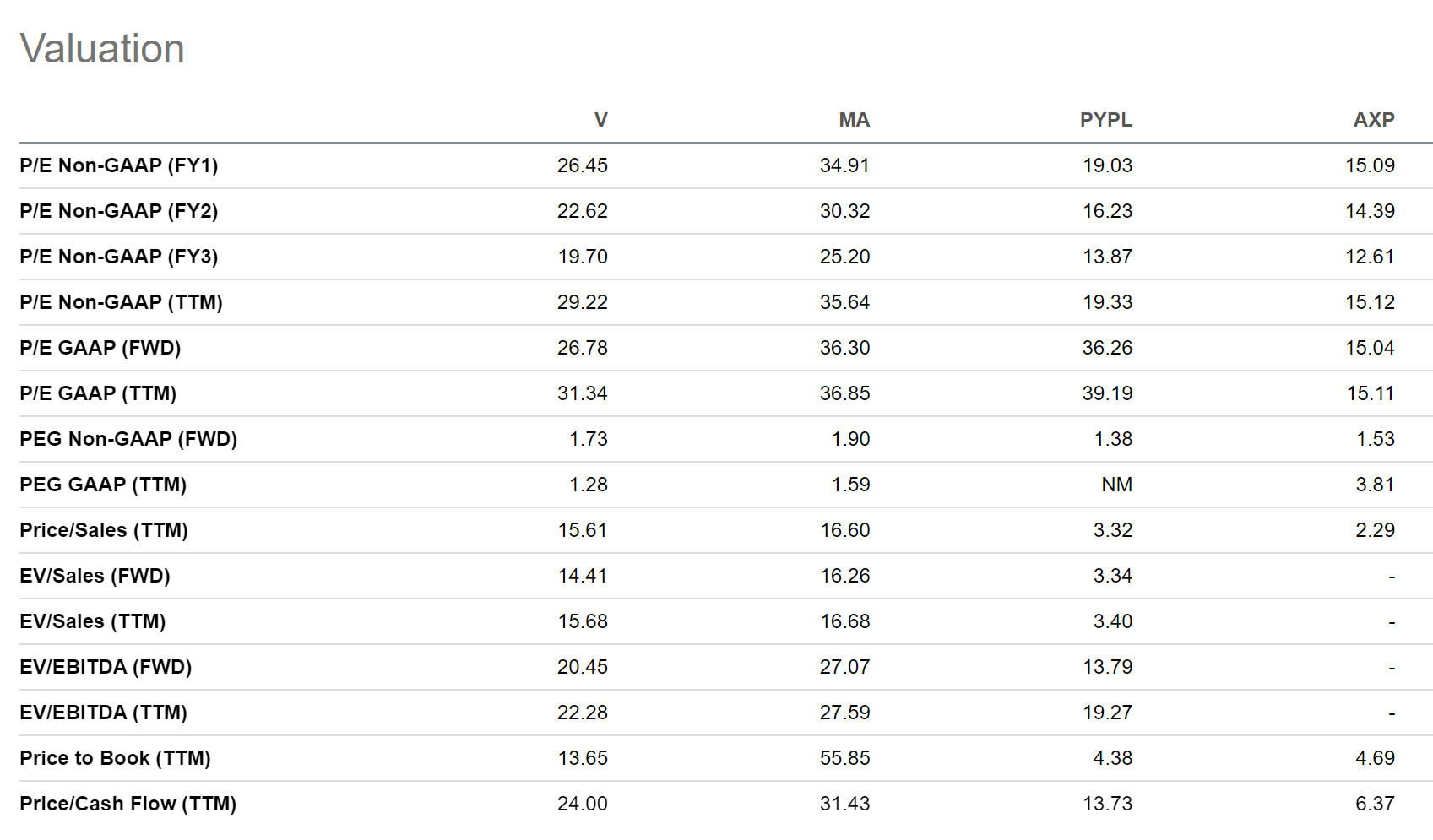

In addition to the factors mentioned above, I think that Visa is currently available at an attractive price level: the company’s current P/E [FWD] Ratio of 26.78 is -17.31% below its Average P/E Ratio over the last 5 years, indicating that the company is undervalued at this moment of time. This is also underlined by the fact that Visa is less expensive than its competitors Mastercard (NYSE:MA) (P/E [FWD] Ratio of 36.30) or PayPal (NASDAQ:PYPL) (36.26).

However, if you are looking for a stock that is currently available for an even cheaper Valuation than Visa and also operates in the Payment Industry, then you might want to look at American Express (NYSE:AXP), which currently shows a P/E [FWD] Ratio of only 15.04, making the company an even more appealing choice than Visa in terms of Valuation.

Below you can find an overview of the different Valuation Metrics in order to compare Visa to competitors such as Mastercard, PayPal and American Express in terms of Valuation.

Source: Seeking Alpha

Conclusion

The still relatively high inflation rate of 6.5% from December of 2022, contributes to the fact that your money loses value over time. This makes it unavoidable for you to think about how to protect your money against inflation. For this reason, I have selected five companies that can help you to hedge your investment portfolio against inflation.

All of these companies have strong competitive advantages, including a strong brand image, which enables them to pass on the higher costs caused by inflation to their customers.

In addition to that, the five companies are undervalued or at least fairly valued at this moment of writing, thus providing you with an attractive entry point when making the acquisition.

In addition to that, I consider them to be attractive in terms of risk and reward and they are also among the leading companies within the Industry in which they operate. Additionally, all of them pay you a Dividend, which helps you to earn an additional amount of extra income each year. Furthermore, they have shown Dividend Growth over the past years or even decade, which helps you as this additional extra income increases year over year.

All of these factors make these companies excellent choices for contributing to protecting your money against inflation over the long term.

I would love to know what you think about these 5 picks and which companies are among your favorite stocks to hedge against inflation?

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment