selvanegra/iStock via Getty Images

2seventy bio (NASDAQ:TSVT) is now a commercial-stage pharmaceutical company, as its cancer therapy Abecma is marketed by Bristol Myers Squibb (BMY). So far, however, revenue to 2seventy itself has been slow to ramp up. The key questions for investors are how quickly Abecma revenue will ramp, including potential long-term ramping from label expansion, and the timeline for the potential therapy in the pipeline to mature. My take is that the company is currently priced about right, but the stock should go up on more positive revenue or drug trial data.

Q3 2022 Results

For Q3 2022 2seventy reported U.S. Abecma sales by Bristol Myers Squibb of $75 million. BMS reported $107 million in Abecma sales in Q3, of which $75 million was in the U.S. However, under the terms of their agreement, 2seventy revenue was only $13.4 million, consisting of $7.9 million collaboration revenue, $0.9 million royalty revenue, and $4.6 million service revenue. Meanwhile, 2seventy spent nearly $62 million on research and development plus $20 million on general expenses. That resulted in a net loss of $67.9 million or $1.76 per share. That was worse than the net loss of $60 million in Q3 2021. In short, 2seventy is a long way from cash flow breakeven.

At the end of the quarter, 2seventy had cash and equivalents of $325 million. If $70 million is taken as a cash burn rate, the company could run out of cash as early as Q4 2023. That would likely mean a cash raise and stock dilution for current investors.

Abecma

Abecma (idecabtagene vicleucel) is a CAR T therapy currently approved for treating multiple myeloma, but only after at least three prior lines of therapy have failed. 28% of patients tested in this very sick, therapy-resistant patient population achieved a complete response, and 72% had a partial or complete response. It is currently in clinical studies that could expand its label to earlier lines of therapies. The Phase 3 KarMMa-3 trial showed Abecma compared to standard combination regimens in adults with relapsed and refractory multiple myeloma after two to four prior lines of therapy met its primary endpoint for progression-free survival and the secondary endpoint of overall response rate. In November, 2seventy bio announced that data from two cohorts of the KarMMa-2 study of Abecma, in patients who have suboptimal response to transplant or early relapse, will be presented at the 64th American Society of Hematology Annual Meeting and Exposition. Data from KarMMa-2 cohorts 2a and 2c suggest the potential for early treatment with Abecma in patients with second line and newly diagnosed multiple myeloma, and for patients with suboptimal response after transplant.

In September 2022, 2seventy bio announced plans to initiate the KarMMa-9 study, in partnership with BMS, to evaluate Abecma in newly diagnosed multiple myeloma patients who have suboptimal response to transplant. While many multiple myeloma patients eventually progress through multiple lines of therapy, treatment with Abecma earlier may be effective. That would greatly expand the revenue opportunity for 2seventy and BMS. At this point, the timing of potential label expansion has not been announced.

Clinical Pipeline

2seventy has two drugs in clinical trials besides Abecma. DARIC33 is being tested in pediatric acute myeloid leukemia. It is in Phase 1. The highly engineered, CAR T therapy bbT369 is being tested for B-cell non-Hodgkin lymphoma.

Pre-clinical Pipeline

2seventy has four therapies known to be in preclinical trials, plus multiple undisclosed potential candidates. DARIC33 NEXT-GEN is an enhanced version of DARIC33 for acute myeloid leukemia, likely including for adult patients. bbT4015 is a CAR T targeting MUC16 mutated ovarian cancer. There is an enhanced, next-generation CAR T therapy for multiple myeloma, not yet named. MAGE-A4 is a TCR T cell therapy potentially for solid tumors. So far, the CAR T and TCR therapies put on the market via various companies have been limited to treating blood cancers. One engineered to successfully attack a solid tumor would be an important advance.

Valuation

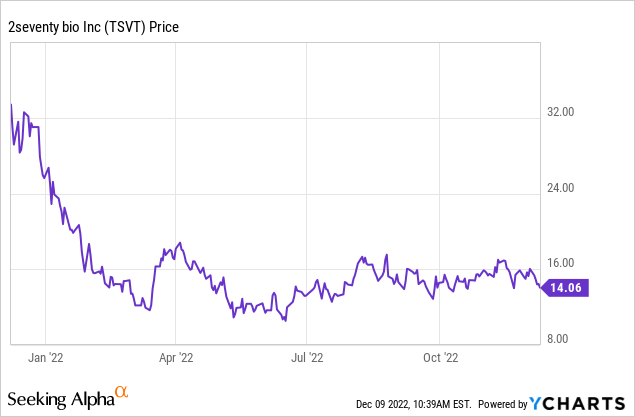

Although technically 2seventy is a commercial-stage pharmaceutical company, it has many of the characteristics of a clinical-stage company, like its high research and development spend compared to its revenue. At its closing price of $14.45 on December 8, 2022, it had a market capitalization of $548 million. It has been a volatile year for the company: the 52-week low was $9.91, the 52-week high was $34.02. Given its $325 million in cash, the success of Abecma, and the strength of the pipeline, I see the stock as undervalued. For once, my own opinion is aligned with major brokerages. SVB Leerink has a price target for 2seventy bio of $41 per share; Morgan Stanley has a price target of $29.00. As with any early commercial or late clinical-stage biotechnology company, there remains a fair amount of risk from pipeline failures or commercialization failure. So 2seventy may be too risky for many portfolios, despite being undervalued by my standards.

Be the first to comment