bymuratdeniz

Commodities vs. S&P (Rotation Report)

For this first article of 2023, I’m not going to get granular – I don’t think we need get excited about oil and gas, at least for the first few weeks of 2023. Instead, I want to try and get a grip on what we might expect for the coming year and why I think 2023 might turn out to be even better for energy investors than 2022 was.

Energy completely bucked the trend for investors in 2022 – the stock markets had their seventh worst year in the last 100, with the averages settling about 20% lower. Everything that had been golden in the marketplace (namely tech and growth stocks) had their worst year since the 2000 disaster. So, in evaluating the gains made in energy, they’re even more impressive.

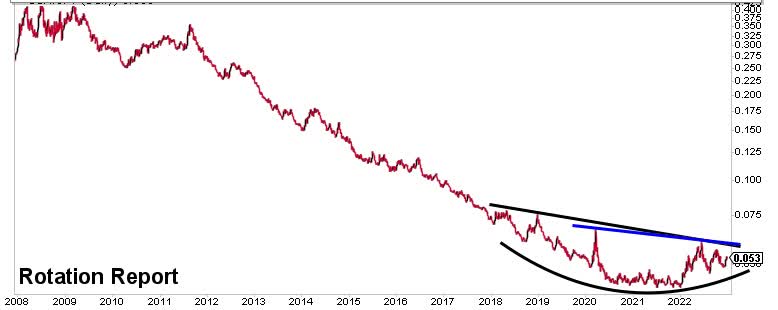

So, for me to be optimistic about 2023, I must not be expecting a repeat of overall languid markets as in 2022 and banking on one nearly universal prediction NOT coming true – that is, the horrifying, very bad, cataclysmic recession that virtually every economist is predicting for the coming year. I’m also banking on a trend continuing through the coming year – that is, the resurgence of commodities and commodity stocks that had been on the bottom of the investing heap for the last more than 10 years (see above chart).

I’m not exactly alone in both of these ideas – but the folks who are with me are swamped by the monsters taking the other side of these bets. Jamie Diamond, Mohammad El-Erian and Michael Burry vs. Howard Lindzon, AVC and me is not a street cred battle that I’d look forward to winning.

But I’ve got some good data on my side, as well as my own 40-year investing success.

We can dissect the 2022 investing horror pretty simply – a supply and employment disaster fueled by the pandemic, central banks with a desire to stop the inflationary spiral – all topped off with a war in Ukraine and a web3/crypto collapse that was probably long overdue.

Which parts of these trends are liable to be different in 2023?

Let’s start with the pandemic, still raging in China where global growth begins and ends. I think we’re still looking at a bunch of trouble there. Recently, some 50% of plane passengers coming from China were found to be infected with COVID, and that’s with the Chinese travel bans starting to come off. Go get your third or fourth booster, folks, and do it quick because that strain of COVID will likely be floating heavy through New York City (and beyond) in a matter of weeks. For reasons I can fathom but not understand, Xi Jinping and the Chinese government have continued to rely upon lockdowns and inferior vaccines to combat their endless battle with COVID, and I have been waiting for Xi to throw in the towel on this strategy – because it’s clearly not working. When this latest strain of the COVID-19 virus starts being felt in the streets of New York, London and Tokyo like it’s being found today in Milan, I think the world will become fed up with it all and demand a universal (Pfizer/Moderna) vaccine on the Chinese. The sooner that decision is made, the better for the markets.

With the central banks, these quick interest rate increases we saw in 2022 haven’t seen their parallel since the Volcker days. But again, despite the fact that virtually everyone thinks the Fed will continue to tighten, I think there’ll be a moment of release after the next Fed meeting on January 31, and Powell will signal it then – at the very least, that would suggest that January is no time to get aggressive.

I also think it possible that Vladimir Putin will find an exit to the clearly now unwinnable war in Ukraine, keeping part of the Donbas and acceding to Ukrainian independence, while keeping his dictatorship intact.

If we get both a Chinese policy shift on COVID and a “break” on tightening from the Fed, the recession that everyone is expecting could in fact be just like the last four we’ve had – that is, about two years long, with a 23%-35% dip in stock indexes – very much in the neighborhood of what we’ve already endured. I, for one, don’t believe a “soft landing” is impossible.

So, I’m not nearly as pessimistic about all markets in 2023 as most others, except for perhaps the first three months – and I’m even more optimistic on energy in particular:

2022 did one thing clearly – it redefined the energy world and put to rest (at least practically) the idea of “replacing” fossil fuels with renewables – an idea held as dogma through much of Europe and here in the United States – and an idea I’ve tried to consistently debunk, most strongly in my last book.

Whatever dreams climate advocates had of seeing oil companies go broke and stop drilling and burning oil and gas are now only spoken about in hopeful tones at COP27. The Ukraine war and the Euro energy crisis quickly demonstrated how deeply we all rely and will rely for many years to come on fossil fuels. Do you want to guess which was the strongest sub-sector of Energy for 2022? It was Coal – filthy, left for dead coal. That says something very real about the future of oil and gas.

Fundamentally, the supply of global oil is far below the demand, and the latest 2 million barrel a day cut from OPEC has only added to the shortage. However, those supply fundamentals have recently been masked by the financial inputs of rising interest rates, a strong dollar and a paralyzing fear of recession. And all of my predictions for energy are based on the thought that those inputs are about to start fading through the new year.

That should make for a gangbusters commodity rally, with oil and gas leading the way.

Have a look again at the chart at the top of this article – it basically shows how commodities have fared against the S&P for the last 15 years (courtesy of the Rotation Report). As much as people love to complain about the price of corn flakes, coffee and gasoline, this is a group of products that simply have not kept up either with the path of inflation nor the prices of every other hard asset. That turnaround, in my mind, only began in 2022 and should certainly have at least another two to three years to run – and possibly run very hard indeed. This could supercharge the returns of US majors faves of mine like Exxon Mobil (XOM) and Chevron (CVX) as well as US independent oil producers like EOG Resources (EOG) and Pioneer Natural Resources (PXD).

But I have another chart that outlines another “turnaround” trend that could supercharge a different energy sub-sector even more than these great primary oil and gas E&Ps.

Tune in next week for that one.

Be the first to comment