Andrii Sedykh

Blue chip stocks can be found in nearly every sector, and doesn’t have to be reserved for household names like Microsoft (MSFT) or Berkshire Hathaway (BRK.A) (BRK.B). For income investors who prize high yield, BDCs and REITs can be great places to start.

This brings me to the following picks, which have a combination of scale and moat-worthy assets that should continue to generate strong returns for investors in the foreseeable future, and both currently trade at valuations that belie their long-term total return potential.

Pick #1: VICI Properties

VICI Properties (VICI) is a premier experiential REIT that’s headquartered in New York City, and holds iconic gaming and hospitality properties along the Las Vegas strip and around the U.S. It kicked off with a bang in 2018, when it was spun-off from Caesars Entertainment (CZR).

VICI benefits from having a steady revenue stream from 100% triple net leases, meaning that tenants are responsible for paying property tax, maintenance, and insurance.

Moreover, 80% of its rent roll come with master lease provisions, thereby lessening the likelihood that a tenant will default on any single property being leased. Plus 76% of VICI’s annual base rent comes from S&P 500 tenants, who generally have more funding sources than private enterprises.

VICI is well-positioned to take advantage of mispricing opportunities on the market, as some players seek to exit stakes in “bond-like” assets in response to higher interest rates. This is supported by high interest from bond investors, as reflected by VICI’s $5.0 billion bond issuance last year, marking the largest REIT investment grade (BBB- rating) debt issuance ever.

This helped to enable VICI’s recent closing of its acquisition of the remaining 49.9% stake in the joint venture that owns MGM Grand Las Vegas and Mandalay Bay Resort from Blackstone (BX) Real Estate Income Trust for $1.27 billion.

There also appears to be no shortage of opportunities as VICI is expanding into Canada through its acquisition of 4 PURE Canadian gaming properties this year. This portfolio comes with minimal Capex requirements of just 1% annually, and has a long-duration initial lease term of 25 years with four 5-year renewal options. Annual rent escalators range from 1.25% in years 2 and 3, and the greater of CPI or 1.5% in years 4 and beyond (capped at 2.5% escalation per year).

Moreover, VICI is more than just a gaming REIT, as it also has a loan portfolio as well, including one for Great Wolf Resorts in Connecticut that was announced this month. This is VICI’s fourth loan investment with Great Wolf for a total capital commitment of $553 million.

Importantly, VICI has grown its dividend meaningfully in recent years, and its dividend is well-covered by a 79.5% AFFO payout ratio. As shown below, VICI has grown its dividend in the 8% to 11% range every year except for one since 2018.

Investor Presentation

While VICI doesn’t appear to be cheap at the current price of $34.18 with forward P/FFO of 23 (based on 2022 expectations). It’s worth noting that analysts expect 61% FFO per share growth this year, as VICI’s recent investments begin kicking in income.

This brings the forward P/FFO down to 14.4 based on 2023 analyst expectations. Analysts have a consensus Strong Buy rating on the stock with an average price target of $37.75, implying mid-teens total return potential over the next 12 months.

Pick #2: Ares Capital

Ares Capital (ARCC) is the largest BDC by asset size and is externally managed by the well-respected Ares Management (ARES), a leading alternative asset manager that operates in the credit, real estate, and private equity spaces. Notably, it was one of the few BDCs to actually grow its asset size during 2020, when most of its peers were hunkering down.

ARCC benefits from an experienced management team with a 28 years average investment experience. Since inception, ARCC has invested $85 billion with an impressive realized asset level gross IRR of 14%. It’s also known for conservative management practices, as it’s realized a 1.0% average annual net realized gain in excess of losses since IPO.

At present, ARCC carries a sizeable $21.8 billion portfolio, with 85% of its portfolio companies being controlled by PE sponsors that have significant resources to support their investments. The portfolio consists of 466 companies that’s well-diversified, with the largest investment being just 2% of the portfolio total, and the average position representing just 0.2% of portfolio total.

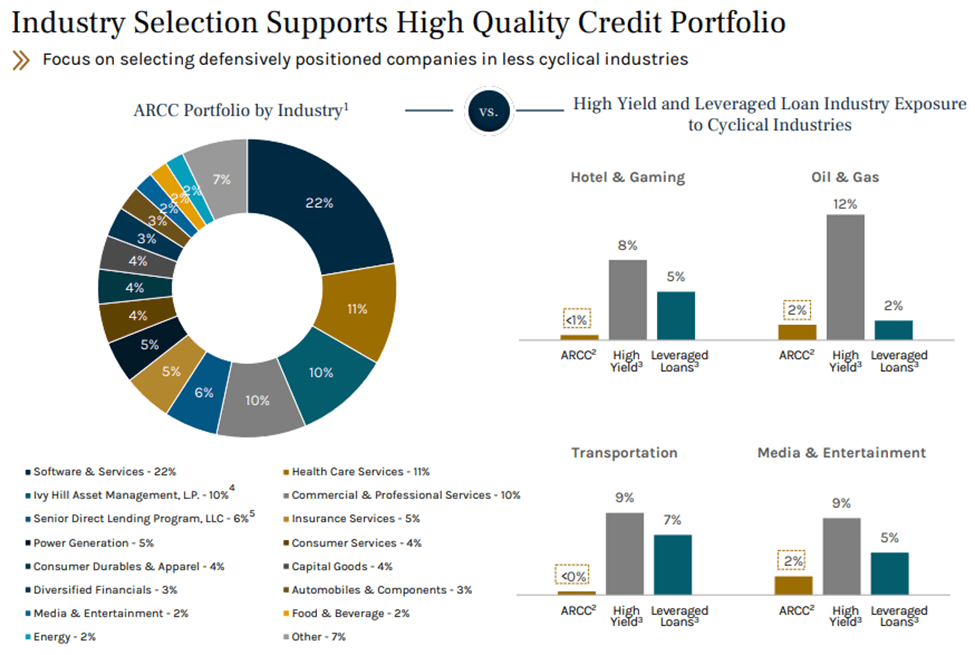

Moreover, 65% of ARCC’s portfolio consists of senior secured loans. As shown below, the portfolio is comprised largely of defensive and growing industries such as software, healthcare, and professional and insurance services, and low exposure to cyclical industries such as oil and gas.

Investor Presentation

Meanwhile, ARCC continues to demonstrate solid results, generating Core EPS of $0.63 during the fourth quarter, which is well in excess of its $0.48 regular quarterly dividend. Investments on non-accrual remain low, at just 0.5% of portfolio fair value, and the weighted average portfolio grade was at 3.2 (on a scale from 1 to 4, with 4 being the lowest risk), comparing favorably to the 3.1 grade at the end of 2021.

Importantly, ARCC’s balance sheet is in good shape, with a debt to equity ratio of 1.26x, sitting well below the 2.0x statutory limit. This gives ARCC plenty of balance sheet flexibility to handle potential for economic uncertainty, as noted by management during the recent conference call:

We do have an expectation that a slower U.S. economy and the higher rate environment will create more stress in the portfolio, and we’re focused on getting ahead of it as we have in past economic and market cycles.

Led by partners with an average of over 15 years tenure at Ares, we believe we have the largest and most experienced portfolio management team when compared with other direct lenders. And this team works in collaboration with our core investment teams to actively monitor and engage with our borrowers and sponsors.

Our goal is to identify problems early and develop strategies to maximize our outcomes in companies that are underperforming to plan or having more difficulty in the higher interest rate environment.

Lastly, I see value in ARCC at the current price of $19.61 with a price-to-book ratio of 1.07x. As shown below, this sits at around the middle of ARCC’s normal valuation outside of the 2020 period. Analysts have a Strong Buy rating with an average price target of $21.13, implying a 1.15x price-to-book multiple and a potential 18% one-year total return over the next 12 months.

Seeking Alpha

Investor Takeaway

Income investors seeking blue chip quality ought to consider VICI Properties and Ares Capital. Each pick is diversified from one another and offer the combination of scale, reputation, and high quality assets. Both carry Strong Buy ratings from the analyst community and offer a combined average 7.2% yield, which may fulfill the income needs for many investors.

Be the first to comment