Whiting Petroleum’s (NYSE:WLL) shares and bonds tumbled after reports that it was considering an exchange of some of its unsecured debt for second-lien debt. That result seems like a bit of an overreaction (particularly for Whiting’s near-term notes), given that there was already a high likelihood that Whiting would be looking at secured debt to help address its debt maturities.

The current situation (with oil dropping below $50) would be unsustainable for Whiting in the long term. However, it could buy itself additional time with a successful debt exchange offer.

I consider Whiting’s 1.25% convertible notes due 2020 to be the most attractive of its securities due to the lack of strategic rationale for Whiting to default on those notes. Those notes have traded at around 90 to 96 cents on the dollar recently.

Debt Structure

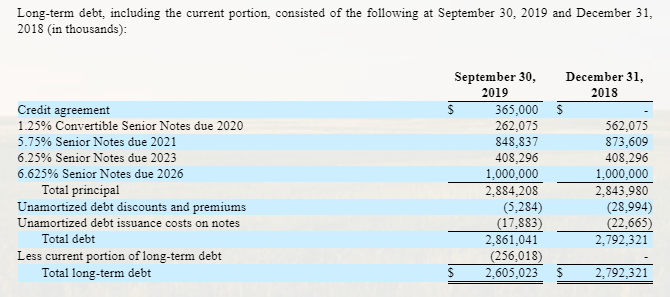

As of Q3 2019, Whiting’s debt structure was as follows. While Whiting does have leverage issues (debt is around 3.0x unhedged EBITDAX at low-$50s WTI oil), its more pressing problem is the series of unsecured debt maturities it has coming up. Without a second-lien debt exchange, it could use its credit facility to deal with its 2020 and 2021 debt maturities, but it would probably have challenges dealing with its debt maturities for 2023 and beyond. Whiting’s credit facility currently matures in April 2023 anyway.

{kind=link}

Source: Whiting Petroleum

Potential Debt Exchange Offer

I’ve outlined a potential debt exchange scenario below. In order to address its maturities, I can see Whiting attempting to offer $1 billion in 8.0% second-lien notes (which would be around 1.1x unhedged EBITDAX at $52 WTI oil) due 2025. The exchange would be for Whiting’s 2021, 2023, and 2026 unsecured notes, while it would use its credit facility to redeem its 2020 convertible notes.

Based on the approximate relative prices of the bonds before the reports of a possible debt exchange, Whiting may offer $1,000 in second-lien notes for $1,000 principal of the 2021 notes, around $750 to $800 in second-lien notes for $1,000 principal of the 2023 notes, and $600 to $650 in second-lien notes for $1,000 principal of the 2026 notes.

The acceptance priority ranking would be the 2021, 2023, and 2026 notes, in order. Assuming that around 45% of the 2021 notes tender, 55% of the 2023 notes tender, and 71% of the 2026 notes tender, then Whiting would end up with the following capital structure (around mid-2020).

| $ Million | |

| Credit Agreement | $627.1 |

| 8.00% Second-Lien Notes due 2025 | $1,000.0 |

| 5.75% Senior Notes due 2021 | $466.8 |

| 6.25% Senior Notes due 2023 | $183.7 |

| 6.625% Senior Notes due 2026 | $290.0 |

| Total | $2,567.6 |

Whiting’s total debt would be reduced by over $300 million, and its leverage would be around 2.7x EBITDAX at $52 WTI oil. Whiting’s annual interest expense would be reduced by around $3 million as a result of the exchange. Using its credit facility to redeem its 2020 notes may increase its interest costs by around $7 million (resulting in a net increase of $4 million), but that’s probably unavoidable.

In this scenario, Whiting would end up with around $1.09 billion in credit facility debt if it wants to use its credit facility to address its remaining 2021 notes, which seems more manageable than the $1.475 billion it would end up with on its credit facility in a scenario without a debt exchange. Whiting is currently allowed to repurchase debt using its credit facility as long as it has at least 15% availability remaining after, which puts a limit of around $1.488 billion at the moment.

This debt exchange would also likely give it the ability to use its credit facility to redeem its 2023 notes if needed, which it would not be able to do without the debt exchange.

Whiting’s primary debt concern in this hypothetical scenario would be then addressing its 2025 second-lien notes.

Whiting’s 1.25% bonds due April 2020

I view Whiting’s 1.25% convertible bonds due April 2020 as being a good value at the lower end of its recent trading range. These bonds have been trading at 90 to 96 cents on the dollar in recent days.

These bonds should have a very low risk of default, as there is only $262 million outstanding. If Whiting uses its credit facility to redeem the 2020 notes, it would still have around $1.1 billion in liquidity, and its credit facility borrowings would still add up to around only 0.7x to 0.8x EBITDAX at $50 WTI oil.

Thus, it would be a very perplexing move for Whiting to default on its April 2020 notes. Whiting has a decent amount of oil hedges in the first half of 2020 as well, so it isn’t going to incur significant cash burn at upper $40s oil for now. The fall in Whiting’s convertible bond price appears to be more of an opportunity for Whiting to save some money by buying those bonds back on the open market a discount now rather than paying full price in a month.

Whiting’s 2021 unsecured debt maturity is a much bigger item (at $849 million) that it may not want to pay in full without a debt exchange first.

Conclusion

A second-lien debt exchange offer does make sense for Whiting as it would buy it some additional time and also modestly deleverage the company. Offering around $1 billion in 8.00% second-lien notes due 2025 may work and would allow Whiting to use it credit facility to redeem its 2021 notes without coming close to maxing out its credit facility borrowings.

Whiting’s 2020 bonds appear to be quite attractive at the lower end of its recent trading range. This maturity is relatively small, and with Whiting having plenty of liquidity and being able to operate at neutral or near cash flow in 2020, there is no good reason for Whiting to default on it. The risk for Whiting’s 2021 bonds is significantly greater without a debt exchange due to the large size of that maturity.

Free Trial Offer

We are currently offering a free two-week trial to Distressed Value Investing. Join our community to receive exclusive research about various energy companies and other opportunities along with full access to my portfolio of historic research that now includes over 1,000 reports on over 100 companies.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment