PonyWang/E+ via Getty Images

Elevator Pitch

I assign a Hold investment rating to Unity Software Inc.’s (NYSE:U) stock.

Investors will view the company’s outlook for the rest of the year very differently, depending on whether they are bearish or bullish on Unity Software. Bears will point to U’s weak revenue guidance for full-year FY 2022 driven by issues linked to Audience Pinpointer. On the other hand, bulls will focus on the potential improvement in Unity Software’s future profitability assuming that the ironSource Ltd. (IS) deal is completed before year-end. In my view, the risk-reward for U is fair, justifying a Hold investment rating.

U Stock Key Metrics

It is relevant to review U’s key financial metrics for the most recent quarter, prior to touching on Unity Software’s outlook for the remainder of the current year.

Unity Software issued the company’s Q1 2022 financial results press release on May 10, 2022, and U’s first quarter sales met market expectations. The company’s top line rose by +36% YoY to $320 million in the first quarter of 2022, which is in line with Wall Street analysts’ quarterly revenue estimate of $321 million according to S&P Capital IQ.

But it was really a mixed quarter for U, if one looks beyond the in-line revenue.

On the positive side of things, the number of clients delivering more than $100,000 in trailing twelve months’ sales for Unity Software grew by +29% YoY from 837 as of end-Q1 2021 to 1,083 as of end-Q1 2022. Separately, U benefited from positive operating leverage in the recent quarter, as non-GAAP operating costs increased by a relatively lower +29% YoY in Q1 as compared with its +36% top line expansion over the same period.

On the negative side of things, Unity Software’s net expansion rate declined from 140% as of end-Q1 2021 to 135% as end-Q1 2022. The company defines the net expansion rate as a comparison of “revenue from the same set of customers across comparable periods, calculated on a trailing 12-month basis” in its Q1 results media release.

At its Q1 2022 investor call on May 10, 2022, U explained that the decrease in its net expansion rate was mainly attributable to advertisers “spending less, because they’re getting less performance out of Audience Pinpointer.” Unity Software also mentioned at the recent quarterly earnings briefing that it was “a combination of different things that reduced the accuracy for our Audience Pinpointer.”

A Brief Description Of Unity Software’s Audience Pinpointer

Unity Software’s Corporate Website

In the subsequent two sections, I review Unity Software’s year-to-date share price performance and its current valuations.

How Has Unity Stock Performed This Year?

Unity Software’s in-line revenue for Q1 2022 didn’t boost the stock’s share price performance this year; in fact, U’s underperformance relative to the broader market widened after it reported Q1 2022 results.

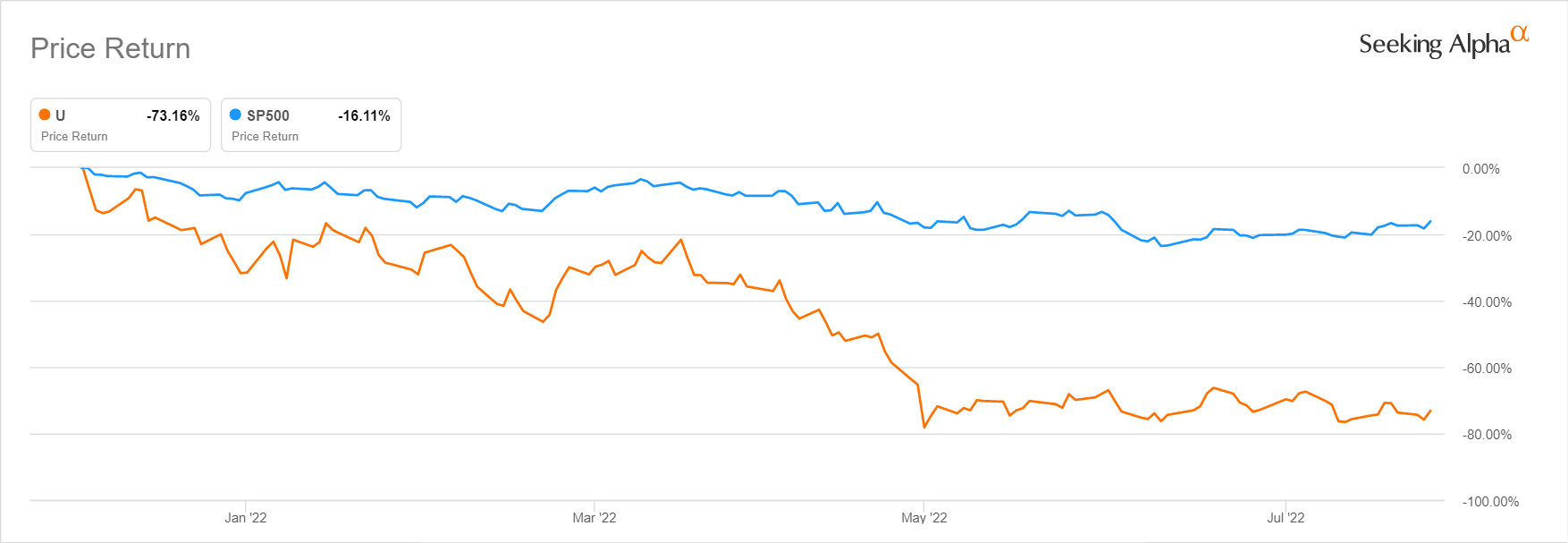

U’s 2022 Year-to-date Stock Price Chart

Seeking Alpha

Specifically, Unity Software’s shares were down by -73.2% in 2022 thus far, while the S&P 500 did far better on a relative basis declining by -16.1% over this same period.

Is Unity Software Stock Undervalued?

U’s valuations have compressed by a large extent in recent months in line with its share price correction highlighted in the preceding section.

Unity Software’s shares have been listed on the NYSE since September 18, 2020. U has traded between 6.0 times and 50.5 times consensus forward next twelve months’ Enterprise Value-to-Revenue in the past two years, based on S&P Capital IQ’s valuation data. Unity Software’s last done share price of $37.22 as of July 27, 2022, translates into a consensus forward next twelve months’ Enterprise Value-to-Revenue multiple of 7.7 times.

Although U’s valuations appear to be relatively low as compared to history, I am of the view that Unity Software is fairly valued rather than undervalued.

One reason is that U is still more expensive than the average growth stock. According to Goldman Sachs’ (GS) July 25, 2022, research report (not publicly available) titled “US Thematic Views – Challenges Remain For Unprofitable Growth Stocks”, the median Enterprise Value-to-Revenue valuation multiple for high growth stocks (revenue growth greater than +30%) has compressed from 14 times at its highest in 2021 to just 4 times now. In this GS report, it was also noted that the historical trough for growth stocks was around 2 times Enterprise Value-to-Revenue. In other words, Unity Software’s shares aren’t that cheap and there is still room for further valuation downside.

Another reason is because U’s forward-looking top line guidance was a disappointment which explains Unity Software’s stock price correction and valuation de-rating, and I will elaborate on this point in the next section.

Where Is U Stock Heading For The Rest Of 2022?

U stock should be heading sideways for the remainder of 2022, as there are both positives and negatives associated with the company’s outlook for the rest of this year.

On one hand, the issues relating to Audience Pinpointer, which I discussed earlier, will continue to be a drag on Unity Software’s top line performance for the whole of 2022. This is reflected in U’s management guidance released in tandem with its Q1 2022 financial results. Unity Software sees its revenue increasing by a modest 6%-8% for Q2 2022, and it expects that its full-year 2022 top line expansion will be in the 22%-28% range, which is much lower than the +30% revenue growth that the market expects from such high-growth names.

More importantly, there is always the risk that the drag from woes relating to Audience Pinpointer might extend into 2023. U noted at its Q1 2022 results briefing that the expectations that the negative impact of Audience Pinpointer issue is limited to 2022 is based on the assumption that “when we (Unity Software) deliver value, we are confident that they will scale up their business with us again.”

On the other hand, Unity Software has guided at its first quarter earnings briefing that it will deliver positive non-GAAP adjusted operating income for Q4 2022 and FY 2023. But it must be noted that U is still expected to be loss-making (at the bottom line) for both FY 2022 and FY 2023. This makes it critical that U successfully completes the ironSource Ltd deal that it recently announced.

Earlier on July 13, 2022, Unity Software disclosed that it had entered into a deal with IS where “ironSource will merge into a wholly-owned subsidiary of Unity via an all-stock deal”. The deal is targeted to be closed by end-2022. At the investor call to discuss the proposed deal, U stressed that this deal “transforms Unity’s financial profile as of day 1 after closing into a highly profitable and cash flow-positive company.” As per S&P Capital IQ, ironSource boasted net profit margin and free cash flow margin of around 10% and in the mid-twenties percentage level, respectively in FY 2021.

In summary, it is hard for U’s shares to perform well for the remainder of 2022, given that its revenue growth rate this year is expected to dip below +30% and it remains unprofitable. On the flip side, the proposed ironSource deal, if successfully completed, could become a gamechanger in enhancing U’s future cash flow and profitability profile.

Is U Stock A Buy, Sell, Or Hold?

I rate U stock as a Hold. Unity Software’s 2022 revenue outlook is disappointing, although the proposed IS deal might have a positive effect on U’s future profitability. More significantly, U’s valuations are fair in my opinion, which warrant a Hold rating for the stock.

Be the first to comment