tang90246/iStock Editorial via Getty Images

One of Singapore’s big three banks, United Overseas Bank (OTCPK:UOVEY)(OTCPK:UOVEF)(“UOB”) has been on my radar for a while as a potentially conservative way to play increasing wealth, economic growth and trade in Southeast Asia.

There is a lot to like about UOB. I’ve alluded to growth already – and the purchase of various Citigroup (NYSE:C) Southeast Asian retail businesses further bolsters the long-term outlook here. On profitability and valuation, too, this bank appears to be crossing all the right boxes, especially with interest rate hikes now providing a nice tailwind to income. At 1.3x tangible book value and a 3.9% trailing-twelve-month dividend yield, this looks like an attractive entry point for long-term investors. Buy.

An Overview of UOB

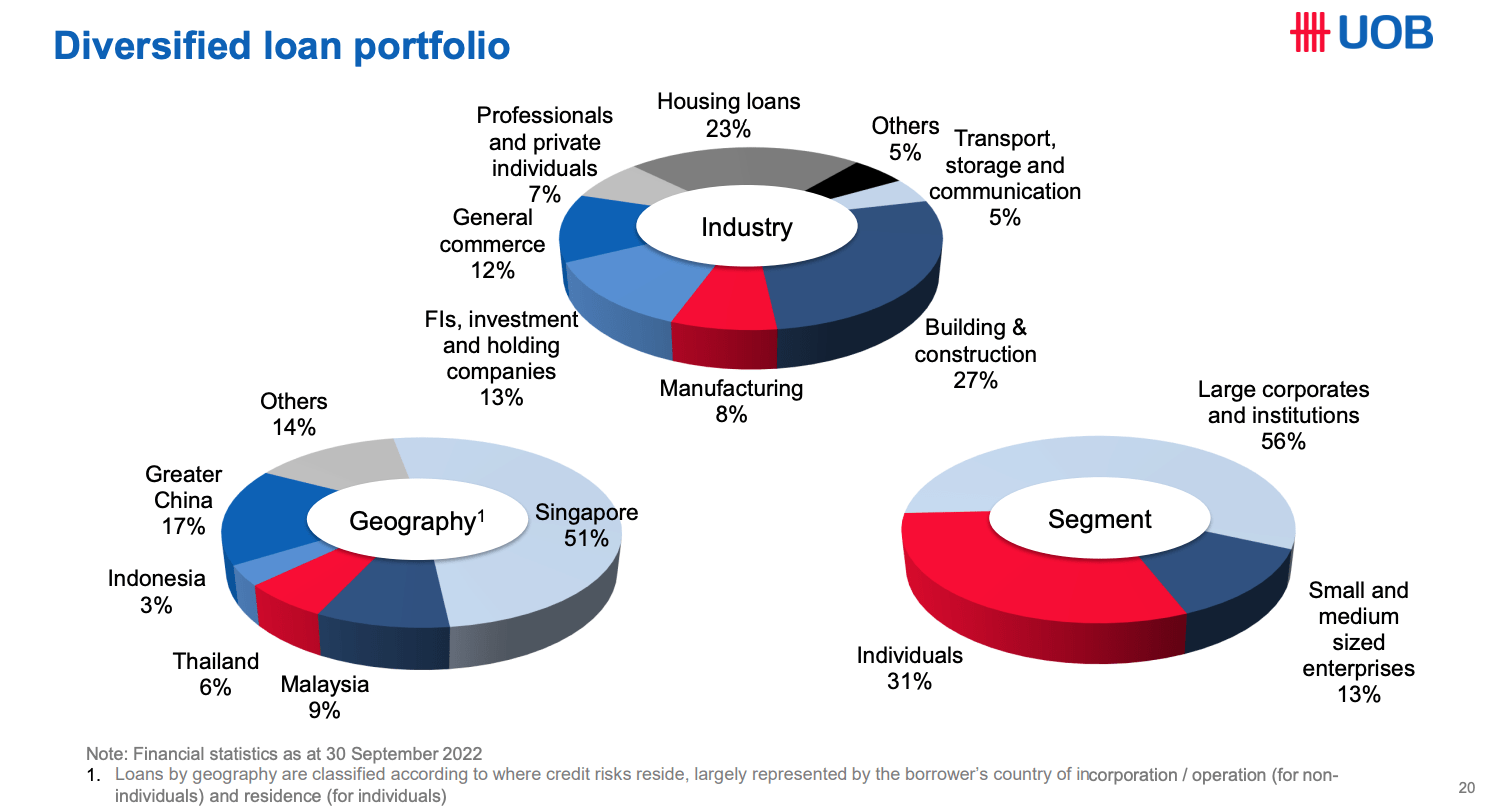

UOB is leveraged to growth in Southeast Asia and Greater China. Around 50% of its loan portfolio is in Singapore, with Greater China (~17%), Malaysia (~9%), Thailand (~6%) and Indonesia (~3%) the bank’s next largest markets.

Source: UOB Corporate Presentation Q4 2022

UOB is primarily a lender. Net interest income makes up around two-thirds of its revenue, with franchises across retail, commercial and wholesale banking. Total assets currently stand at around S$510B (~US$380B).

Not reflected in those figures is the bank’s most recent M&A activity. In early 2022, UOB announced a deal to acquire Citigroup’s retail banking businesses in Indonesia, Malaysia, Thailand and Vietnam for around S$5B (~US$3.7B). The Thai and Malaysian portions of the acquisition closed early Q4, with the Indonesian and Vietnamese businesses expected to follow by the end of 2023. This will add circa S$4B in net assets and S$0.5B of net income, while roughly doubling UOB’s customer base in those countries.

Crossing The Right Boxes

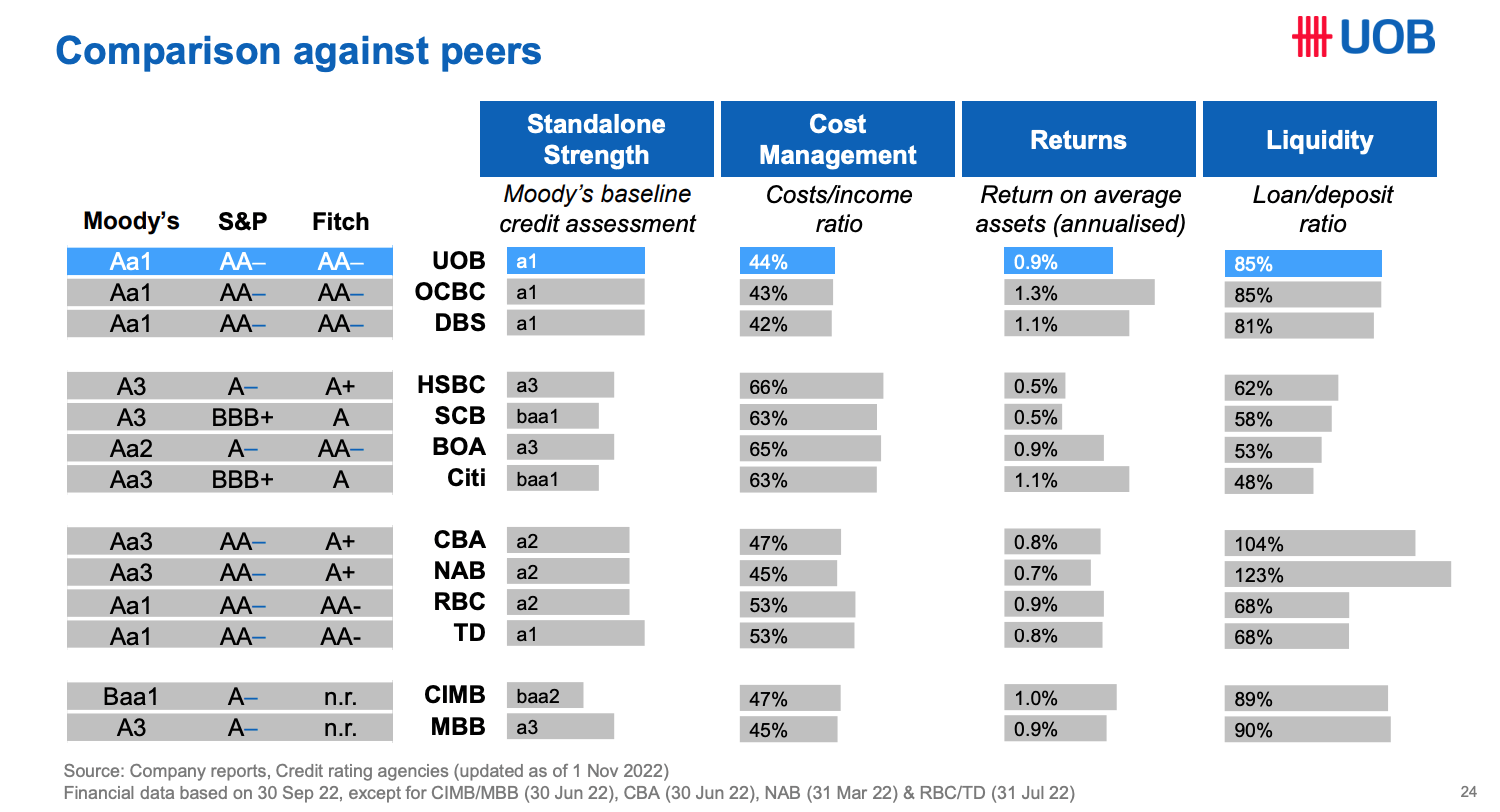

UOB appears to score highly on profitability, growth and, currently, valuation. On profitability, the bank has an attractive funding mix courtesy of its position in its domestic market, Singapore. The big three in order of deposit share – DBS (OTCPK:DBSDY)(OTCPK:DBSDF), UOB and OCBC (OTCPK:OVCHY)(OTCPK:OVCHF) – collectively account for over 60% of the nation’s deposits. In total, customer deposits of S$375B fund around 75% of UOB’s total asset base, with the bank’s CASA ratio currently at circa 50%. The wholesale funding it does utilize benefits from its strong credit rating. UOB is rated Aa1/AA-/AA- by Moody’s, S&P and Fitch respectively.

Source: UOB Corporate Presentation Q4 2022

On top of that, the bank is very efficiently run, with its cost/income ratio in the 45% region. Funding costs and efficient operations have allowed the bank to average a double-digit return on tangible equity in recent years, notwithstanding the negative impact of both COVID and lower interest rates.

On growth, UOB is leveraged to economic growth in Southeast Asia and Greater China. Singapore is the bank’s main profit engine, contributing over half of total group operating profit, and although it is a highly advanced, developed economy GDP growth has been solid.

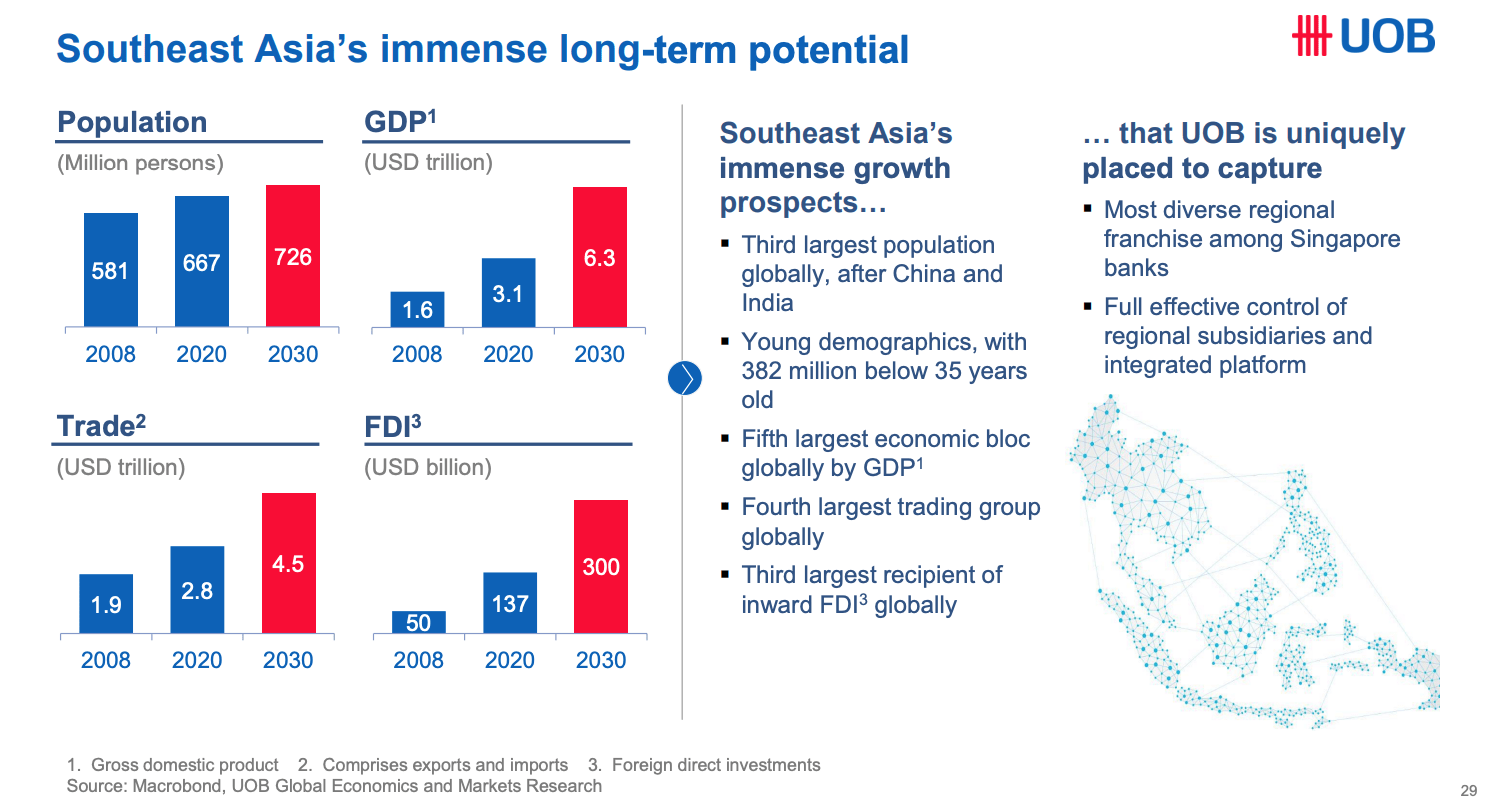

UOB’s emerging market operations offer investors an attractive long-term growth story. Increasing regional trade and economic growth have helped fuel strong loan growth, and this has helped offset the impact of low interest rates on margins. Although the bank’s net interest margin declined by over 25bps between 2018 and 2021, net interest income remained resilient, growing by over S$150m to circa S$6.4B.

Source: UOB Corporate Presentation Q4 2022

Southeast Asia has very attractive long-term growth potential, which will further increase demand for both credit and non-interest-linked products like wealth management.

Leveraged To Higher Interest Rates

In recent years, UOB’s profitability has taken a hit from both lower interest rates and above-average provisioning for potential bad debt due to the COVID pandemic.

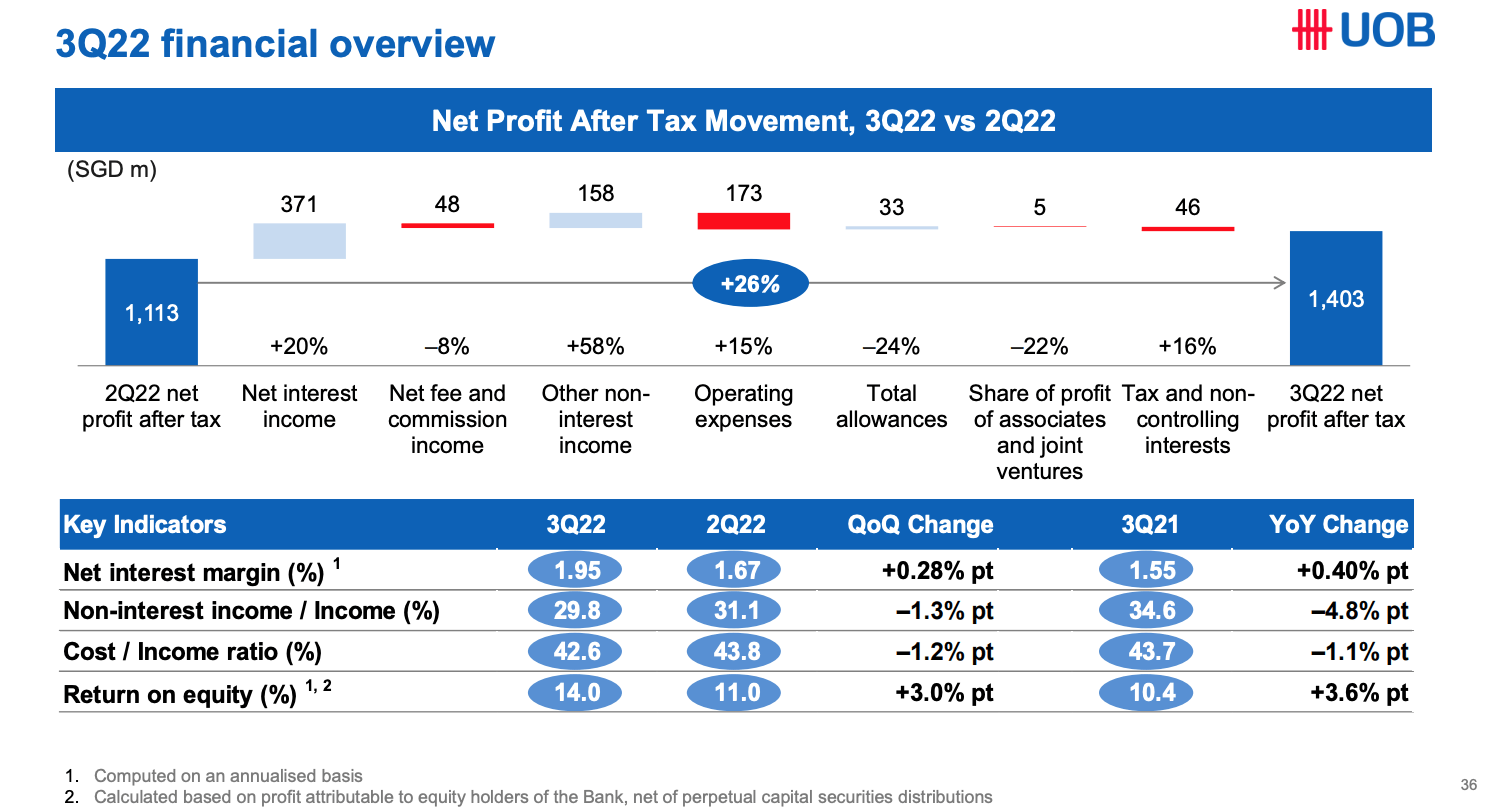

With interest rates now rising, the bank is enjoying a nice tailwind to its income. Net interest income was S$5.8B in the first nine months of 2022, an increase of over 20% year-on-year. Loan growth helped, with gross customer loans advancing 6% year-on-year in that time, but growth was mainly margin driven, with net interest margin of 1.74% up from 1.56% in the year-ago period. Q3 2022 net interest margin of 1.95% was up 40bps on Q3 2021, driving a 39% year-on-year rise in net interest income. Management expects Q4 margins to be in excess of 2%, peaking in Q1 2023. This will help sustain growth in 2023.

Source: UOB Corporate Presentation Q4 2022

At 19bps and 17bps for 9M22 and 3Q22 respectively, credit costs have normalized at UOB having spiked in 2020 due to the COVID pandemic. This helped the bank post a strong 15% return on tangible equity (“RoTE”) in the third quarter.

Looking ahead, a weakening global economy is obviously a significant potential headwind for bank stocks like UOB. Estimated full-year 2022 credit costs of circa 20bps are on the low-side versus the bank’s historical average, and I’d pencil in a future average closer to 30bps. Note that the Citi portfolio will likely have a slight upwards impact on credit costs due to its higher weight of unsecured consumer loans, though on the flip side it should also be positive for NIM.

A significant economic downturn could cause credit costs to spike more in the near-term, though on the plus side, UOB looks reasonably well provisioned following the COVID-related build. Coverage for non-performing assets currently stands at around 100%.

Slower loan growth is the more pressing issue, with gross loans up just 1% sequentially in Q3. The 2022 outlook is also down to the lower end of initial mid-to-high single digit growth expectations. Current expectations are for 2023 credit growth in the mid-single-digits, which may prove slightly optimistic.

Valuation Looks Very Reasonable

UOB shares trade for S$30.80 apiece in Singapore at the time of writing, putting them at around 1.3x tangible book value.

That looks quite low to me, given the bank is guiding for a terminal net interest margin above 2%. That implies a sustainable RoTE in the 15% region even after baking in higher future credit costs. Integration of the Citi assets may dampen RoTE slightly in 2023, though in the medium term balance sheet growth and positive jaws will help maintain profitability at attractive levels. An equivalent bank in the US could easily command a valuation of 1.6x tangible book value, which would put UOB’s fair value at closer to S$37 per share, or 20% above the prevailing price. A 3.9% dividend yield also looks enticing, with a payout ratio below 40% implying attractive growth potential. Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment