GrigoriosMoraitis/iStock via Getty Images

Turning Point Brands (NYSE:TPB) manufactures and sells rolling papers, cigars, moist snuff tobacco, chewing tobacco, and other tobacco/vape related products through brands such as Zig-Zag, Stoker’s, and multiple other names. In addition, the company now sells nicotine pouches through the FRE brand and nicotine infused cotton through the Cotton Mouth brand, acting in a better-growing market. The company gets the overwhelming majority of revenues from the United States, but also sells internationally.

Since the company had an IPO in 2016, the stock has returned very well, despite a poor performance from 2021 forward. The stock has again started to perform very well in the past year, with higher margins sustaining themselves after 2021. Turning Point Brands also pays a growing dividend in addition, although quite a modest one at a current yield of only 0.84%.

Stock Chart From IPO (Seeking Alpha)

FRE Could Revitalize Poor Growth

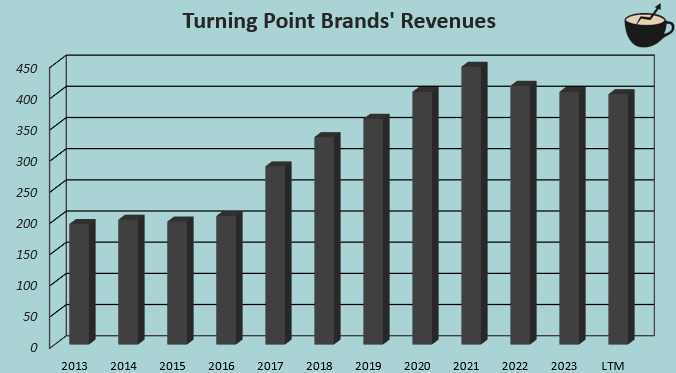

Turning Point Brands mainly sells tobacco-related products, and acts on a highly mature industry, achieving significant growth is difficult for the company. While the company achieved growth in prior years aided by $106 million in cash acquisitions from 2016 to 2021, revenues have turned into negative growth territory from Q3/2021 forward. The market didn’t like poor the revenue trajectory, as the stock had its peak in February of 2021 – stronger revenues are needed to satisfy investors.

The Creative Distribution Solutions segment has been Turning Point Brands’ major driver of poor revenue growth, responsible for the company’s online platform for cannabidiol and vape product distribution. The segment’s topline was down by -14.3% in 2023, and has only had an even more dramatic fall in the past couple of quarters. As the segment’s revenues come down, it represents a smaller portion of total revenues, and eventually should have a non-significant total effect on Turning Point Brands’ total revenue growth.

Author’s Calculation Using TIKR Data

An entry into the nicotine product market could aid Turning Point Brands in achieving future growth. The company has stepped into the rapidly growing nicotine pouch market with the FRE brand to capture a share in the market. While the brand was already launched in 2020, the market has since grown rapidly, slowly making the brand’s revenues more significant for the company. For example, Philip Morris (PM) has grown shipment trailing volumes by 289% from 114 million cans in 2020 into 443 million as of Q1/2024. Turning Point Brands doesn’t report FRE revenues separately, but clearly communicates the brand as a good growth opportunity. In my opinion, the effect on total revenues is likely to be modest but could still revitalize growth into a healthier level.

Earnings and Cash Flows Continue at a Good Level

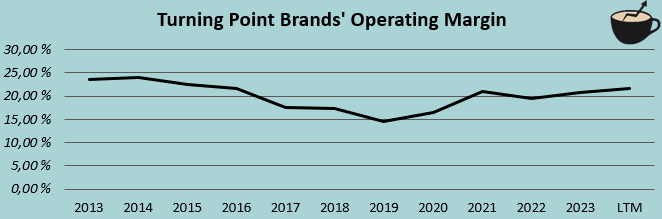

Historically, Turning Point Brands’ margins have been mostly unrelated to revenue growth. Turning Point Brands continues to achieve high and stable operating margins, even achieving good margin expansion from 2019 forward despite weak revenues in the past couple of years. If continued, the past couple of years’ negative revenue growth should eventually affect margins negatively, but with FRE potentially aiding future growth, the effect shouldn’t be dramatic.

Author’s Calculation Using TIKR Data

Along with healthy earnings, undisturbed by macroeconomic pressures, the company is able to constantly generate good cash flows. The company has relatively low capital expenditures with only $3.6 million in the past twelve months, and with stable revenues, the need for additional working capital is low. In the past twelve months, free cash flow has reached $70.5 million, partly aided by lowering working capital.

Q1 Financial Report

Turning Point Brands reported its Q1 results on the 2nd of May. The company posted revenues of $97.1 million, down -3.9% year-over-year but flat quarter-over-quarter. The normalized EPS ended up at $0.80, up significantly from $0.62 in Q1/2023 despite lower revenues. Both revenues and the normalized EPS surprised analysts’ estimates significantly, sending the stock up by 12% for the day. The company also reaffirmed the 2024 outlook.

By segment, Zig-Zag showed a growth of 11.5%, Stoker’s a growth of 8.0%, and Creative Distribution Solutions a dramatic decline of -44.9% – Turning Point Brands’ core focus segments are showing a great performance. The CDS segment’s revenue fall makes the segment worth only 14% of revenues in Q1, making potential future revenue declines not as significant for the company. The reported quarter was overall very good, as the market interpreted it, with Zig-Zag and Stoker’s showing a very good performance.

Valuation Gives a Great Cash Flow Yield

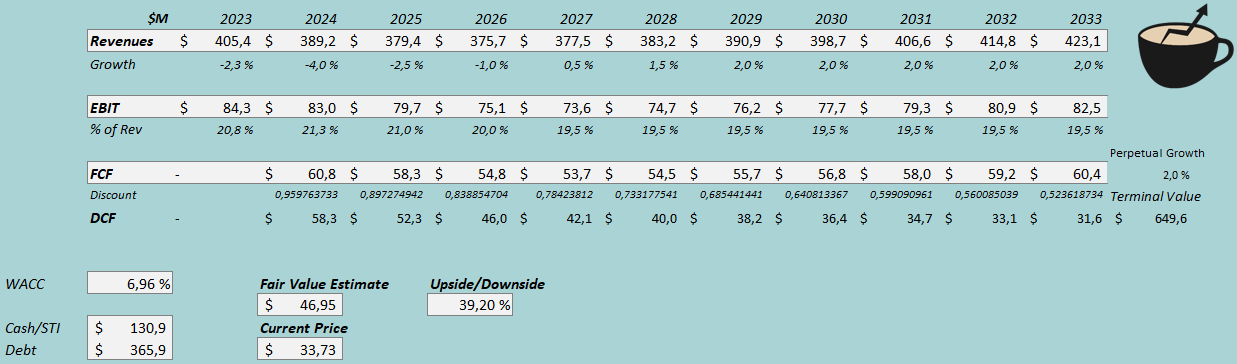

To estimate a fair value for the stock, I constructed a discounted cash flow model. In the DCF model, I estimate a modest recovery into an eventual revenue growth of 2% from 2029 forward, representing near stable real growth. Prior to the year, I estimate growth to stay at even a lower level, with further declines. As for the EBIT margin, I estimate some deleverage into 19.5% from 20.8% in 2023 in the next couple of years due to weak revenues. Turning Point Brands should continue to generate very healthy cash flows with minimal investment requirements.

With the mentioned estimates, the DCF model estimates Turning Point Brands’s fair value at $46.95, around 39% above the stock price at the time of writing. The company yields very good cash flows, and despite weak growth estimates, seems to be an attractive investment at the current price. Elevated growth through lower CDS revenues and good FRE growth could easily turn the stock even more valuable, but for the time being, conservative estimates are in my opinion justified.

DCF Model (Author’s Calculation)

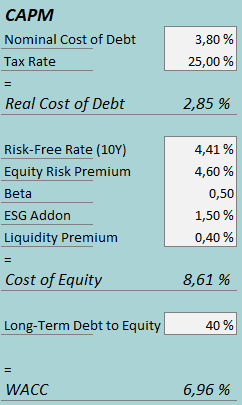

A weighted average cost of capital of 6.96% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q1, Turning Point Brands had around $3.5 million in interest expenses. With the company’s current amount of interest-bearing debt, Turning Point Brands’s annualized interest rate comes up to quite a low level of 3.80%. As Turning Point Brands has non-volatile earnings, the company is able to leverage a large amount of debt, and I estimate a long-term debt-to-equity ratio of 40%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.41%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. Yahoo Finance estimates Turning Point Brands’ beta at a figure of 0.5, as tobacco sales are highly resistant to macroeconomic turbulence. Finally, I add a small liquidity premium of 0.4% and an ESG addon of 1.5%, creating a cost of equity of 8.61% and a WACC of 6.96%.

Takeaway

Turning Point Brands yields stable and good cash flow yield. While the company’s growth has lagged in the past couple of years due to a mature industry and very weak CDS revenues, future growth could be better as the FRE nicotine pouch brand scales. The first quarter of 2024 already showed an elevated growth in the company’s main segments and shows potential for better growth in coming years. With the valuation having good space upwards even with modest earnings estimates, I have a buy rating for the stock for the time being.

Be the first to comment