Jeremy Woodhouse/DigitalVision via Getty Images

Trustmark Corporation (NASDAQ:TRMK), incorporated in 1968 and headquartered in Jackson, Mississippi, offers banking and other financial solutions in Alabama, Florida, Mississippi, and Texas.

This is a company with strong liquidity and a long history, but the long-term performance is not attractive and the dividend yield is too low to offset a potential opportunity cost here, which is very likely considering the shares are currently not undervalued.

Business & Portfolio

Though Trustmark was incorporated in 1968, its principal subsidiary, Trustmark National Bank, traces its history back to 1889 when it was founded in Mississippi. The subsidiary had total assets of $18.3 billion on March 31, 2024, which accounted for the overwhelming majority of the holding company’s assets.

Trustmark’s deposits were $15.3 billion and its total loans amounted to $13 billion as of the end of the last quarter. Further, its current market capitalization is around $1.8 billion these days.

Its business is mainly focused on commercial and consumer banking, but it also provides insurance solutions, as well as wealth management and Trust services.

As of March 31, 2024, 72.2% of its revenue came from the interest and fees it collects on its loan portfolio. As you can see below, the majority of this asset is commercial RE:

10-Q

As the most impactful loan type, you should be aware that 3% of it was rated Special Mention and Substandard during the last quarter. While these are performing loans, the ratings indicate some signs of potential deterioration. Moreover, 8.29% of C&I loans are also regarded as Special Mention and Substandard by the bank and this is a big segment too. More importantly, 2.15% of 1-4 family residential loans are nonaccrual.

Allowance for credit losses had a linked-quarter increase of 2.6% to $143 million in the last quarter, out of which 0.93% were allocated to commercial loans held for investment (LHFI) and 1.63% to consumer and home mortgage LHFI, suggesting expected losses coming from those segments.

That being said, the NPL ratio was not that high at 0.75% in the last quarter and the net charge-offs in 2023 accounted for 0.06% of the portfolio. Still, the context of valuation will put all this in perspective.

Performance

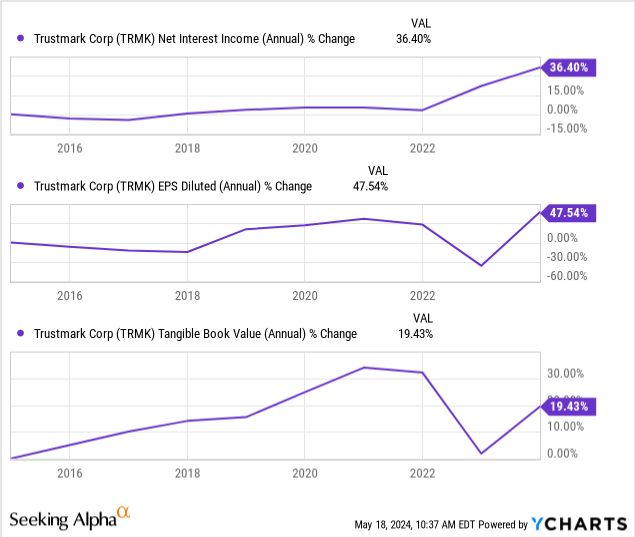

By looking at the long-term performance, things don’t look good either. The growth of NII, EPS, and TBV over the last decade has been both very slow and a bit volatile (slow expansion is understandable for the industry but such erratic growth is problematic):

The same can be observed for the deposits, with single-digit YoY increases for the most part:

Seeking Alpha

Similarly, the loan portfolio grew at a slow pace but more steadily:

Seeking Alpha

As of the end of the last quarter, the yield on its loan portfolio was 6.4%, while it was 5.79% in the same quarter last year. However, the rate of interest-bearing deposits grew as well from 1.53% in 1Q23 to 2.74% in the last quarter. Naturally, interest income decreased by 3.4% to $132.8 million YoY and NIM declined from 3.39% to 3.21%. However, non-interest income, being an enough large contributor to revenue, increased by 7.73%; somewhat offsetting the decline in EPS diluted which fell to $0.68 (a 17.07% decrease).

Looking forward, management expects that NII will decline by low single digits this year. NIM is forecast to be at 3.2%, reflecting no change than the margin on March 31. As for the loan portfolio, it’s expected to grow by mid-single digits and deposits to expand by low single digits. So while there might be some additional pressure on net interest income, the margin seems to stabilize because deposit costs might also be stabilizing given that interest rates are held steady; loan growth appears to continue but at a slower pace than that in 2023.

Liquidity

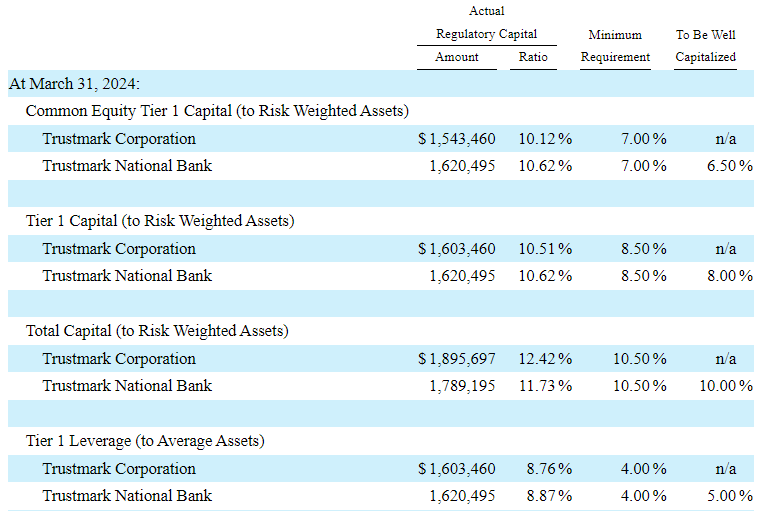

When it comes to the bank’s liquidity, it is strong considering its capital ratios that are well above the minimum requirements for Trustmark to be considered well-capitalized:

10-Q

Also, with an LDR of 85.1%, it appears that it’s conservative in its use of capital and there’s a wide enough margin for loan growth if the demand increases.

Dividend & Valuation

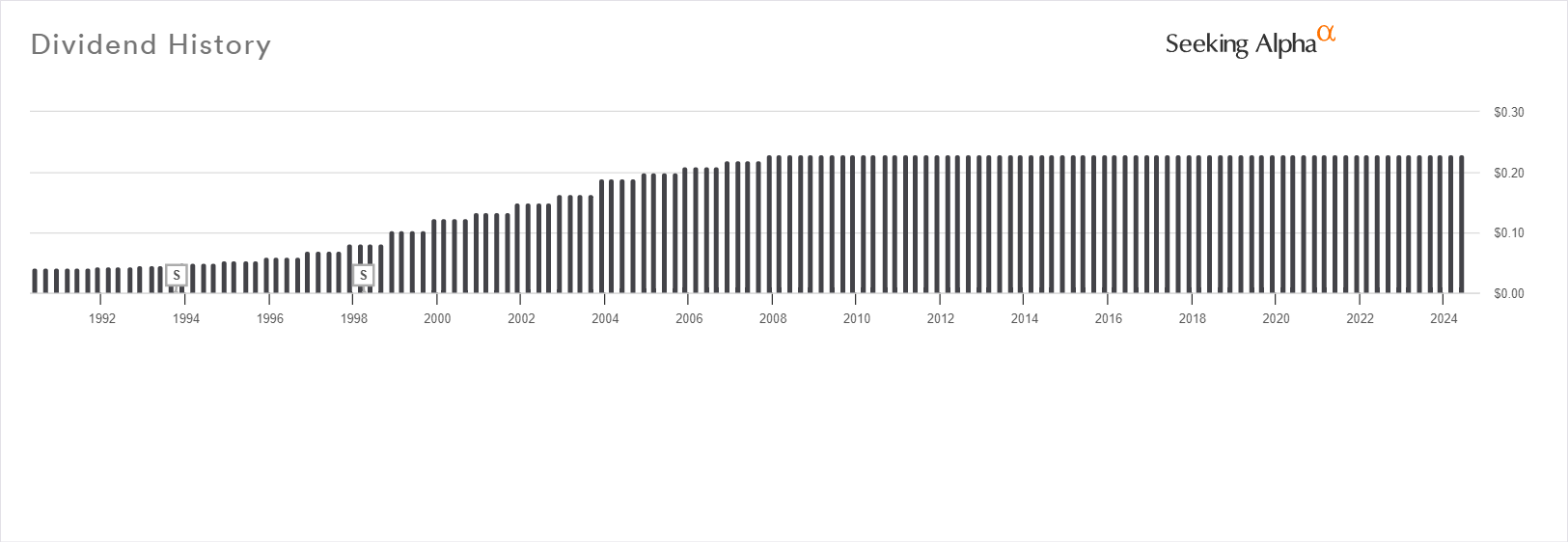

TRMK currently pays a quarterly dividend of $0.23 per share, resulting in a forward yield of 3.02%. With a payout ratio of 34.42% and no history of dividend cuts, this distribution seems to be sustainable:

Seeking Alpha

However, the yield is nothing to drool over right now and the payment record doesn’t indicate a dividend growth trend.

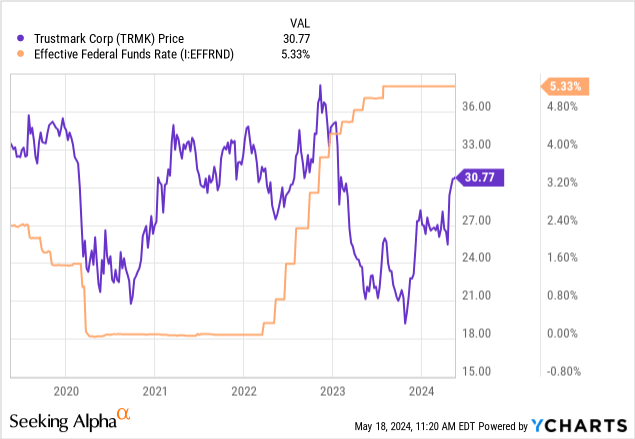

At the same time, the yield doesn’t reflect much value and it seems that the stock price is not historically too low anymore:

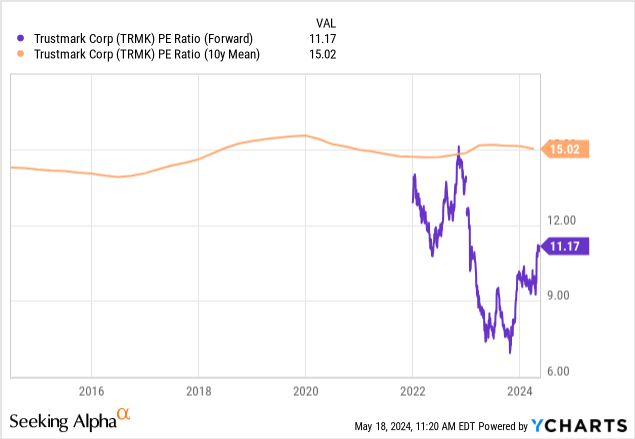

The earnings multiple is indeed attractive and lower than the 10-year mean:

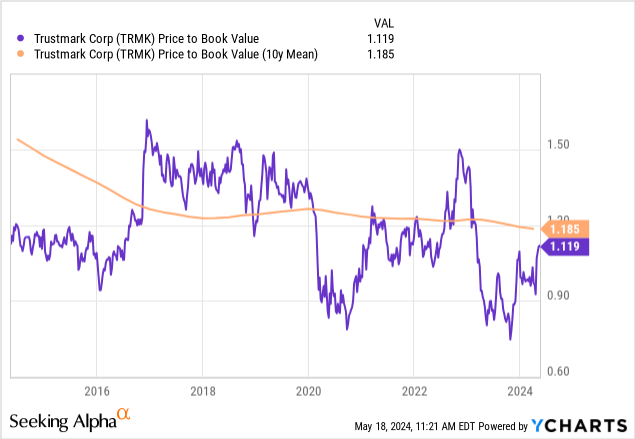

But the P/B ratio is not that attractive, being more than 100% and close to the 10-year mean:

Most importantly, there is a 34.3% premium to tangible book value per share here. While the credit quality of the loans isn’t terribly alarming, I would personally require some discount to reflect the potential losses in such a high-interest rate environment and the premium is too far from one.

Risks

There is, of course, credit and interest rate risk here, but my main issue is an opportunity risk with Trustmark. The valuation doesn’t appear attractive, and the yield is not high enough to offset a potential opportunity cost. The capital position of the bank may be enough to provide some sort of a margin of safety, but it’s difficult to establish a mean-reversion case here.

Verdict

For this reason, I think that the risk outweighs the potential benefits of investing in TRMK. If the price gets lower, I might need to reconsider but this is a hold for now.

What’s your opinion? Do you own TRMK or intend to? Let me know below and I’ll get back to you soon. Thank you for reading!

Be the first to comment