It’s time to discuss AutoZone (NYSE:AZO) again. This Memphis, TN-based auto parts retailer just released its earnings. While sales came in short of expectations, the company once again beat on earnings. Margins were stable as gross margins continued their long-term increase. Management is also confident in its investments in both Mexico and Brazil. If coronavirus fears are able to linger, I believe this stock will have a ton of potential as the current decline has caused a very interesting valuation and risk/reward. Source: AutoZone

Here’s What Happened In Q4

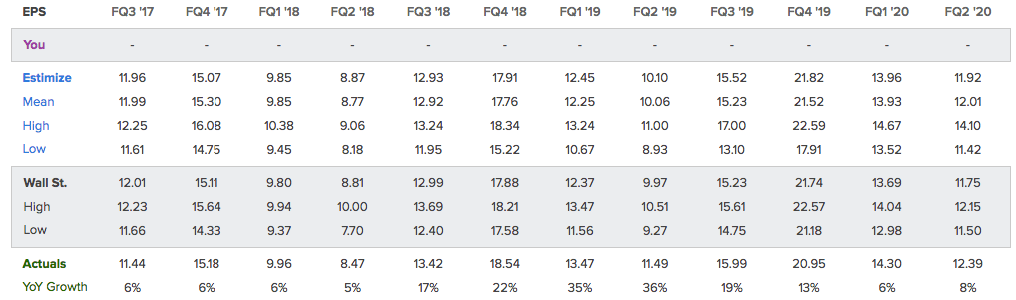

As usual, I start by looking at the adjusted bottom line. In the most recent second quarter of the 2020 fiscal year, the company improved its bottom line to $12.39 per share. This is above expectations of $11.75 and 8% higher compared to the prior-year quarter. The company’s growth streak is doing great as the troubles of lower margins and higher (online) competition are currently failing to hit companies in the auto parts segment.

Source: Estimize

Source: Estimize

In the case of AutoZone, strength started all the way at the top. Second-quarter sales totaled $1.87 billion. This is an increase of 2.6% and includes domestic, Mexico and Brazil stores. Total domestic same-store sales were down 0.8% Commercial sales improved by 8.2%. This segment represents 23% of total sales and was up $42 million. Weekly sales per program were up 5% on average. Commercial sales are also the reason the company is positive going forward. In the third quarter, AutoZone will offer commercial sales in 85% of its stores and expects this to lead to further market share gains and sustainable (same-store) sales.

Another factor expected to deliver substantial long-term growth potential is the addition of new stores in both Mexico and Brazil. In the second quarter, the company opened two new stores in Mexico. This brought the total up to 608 stores. While the addition of two new stores does not sound ‘that much’, management is dedicated to keeping the long-term expansion intact. With regard to Brazil, AutoZone is currently operating 38 stores. While sales exposure is still neglectable, and operating costs are high, management expects the potential size of the Brazilian market, in general, to boost sales in the long term.

Total inventories were up 7% compared to the prior-year quarter. This was mainly caused by new stores and increased product placement. The average inventory value per store went up from $690,000 in the prior-year quarter to currently $713,000.

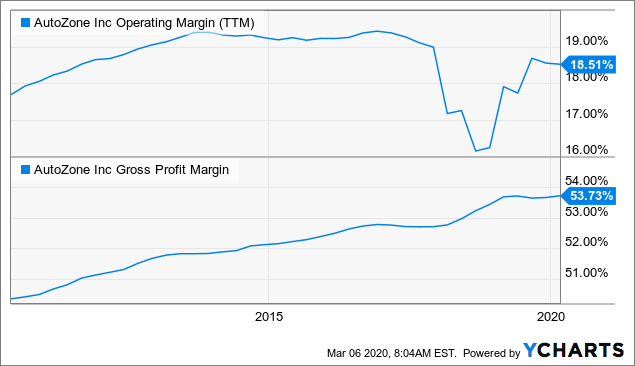

With that said, let’s take a look at company margins. The second-quarter gross margin came in at 54.3%. This is an improvement of 28 basis points compared to the prior-year quarter. The main driver behind this move was supply chain leverage (higher efficiencies). And speaking of supply chains and purchasing, management is lowering operating costs through smart sourcing to offset some of the lower margins caused by accelerating commercial sales.

Unfortunately, SG&A expenses were up 37 basis points to 38.1% of sales as higher salaries and outperforming costs pressured operating margin. The bigger margin picture as seen below is not bad at all (based on GAAP data). Gross profit margin is in a long-term uptrend, and even the operating income margin has recovered nicely again. While I expect the operating margin to stay below 19% for a while, I believe that further strengthening sales will further support the bottom line.

Data by YCharts

Data by YCharts

What’s Next?

Here’s what management had to say with regard to the outlook of the second half of the 2020 fiscal year.

In summary, while we were not pleased with our top-line performance, we were pleased with our operating performance and remain encouraged with our industry strength in both DIY and DIFM, and our prospects for the remainder of the fiscal year. We believe macro factors such as relatively low gas prices and increasing miles driven remain largely in our favor. We remain committed to growing our market share in both, DIY and commercial.

I tend to agree with everything as the top line was only supported by the addition of new stores – comparable store sales were down. Adding to that, the macro factors were good. Gas prices are low, and economic momentum was recovering. I am using words like ‘were’ and ‘was’ as it does not matter anymore. The market is completely shaken by the coronavirus. Absolutely nobody knows what to expect. So far, it seems that the mortality rate is somewhere between 2% and 3% with a ton of undetected cases as people with a strong immune system are often only showing mild symptoms. That’s all I am going to say with regard to symptoms, as all info I have has been gathered in the past few months from various websites.

Nonetheless, while the market is panicking, I like to focus on companies that are good buys at lower prices. AutoZone is one of these stocks. I believe the company’s long-term potential is strong while short-term struggles persist. These struggles are the coronavirus and higher operating costs related to the company’s (strategic) expansion and supply chain improvements. At this point, the stock is trading at 14.2x forward earnings. While I do not know how bad the coronavirus is going to get, I strongly believe there is support above $900 per share.

{kind=link}

Source: FINVIZ

Regardless of what you are doing, keep your cyclical positions small. Focus on long-term investments that can be bought at a good price. With that said, I look forward to the next earnings release as we will get a lot of insights and some data that shows how bad the virus is really impacting retail.

Stay tuned!

Thank you very much for reading my article. Feel free to click on the “Like” button, and don’t forget to share your opinion in the comment section down below! My long-term investments are stated in my Seeking Alpha biography.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This article serves the sole purpose of adding value to the research process. Always take care of your own risk management and asset allocation.

Be the first to comment