Theo Wargo

Last year, Tesla, Inc. (NASDAQ:TSLA) investors were riding the Elon Musk rocketship to the moon, as TSLA surged to the $415 level (post-split price) in November 2021.

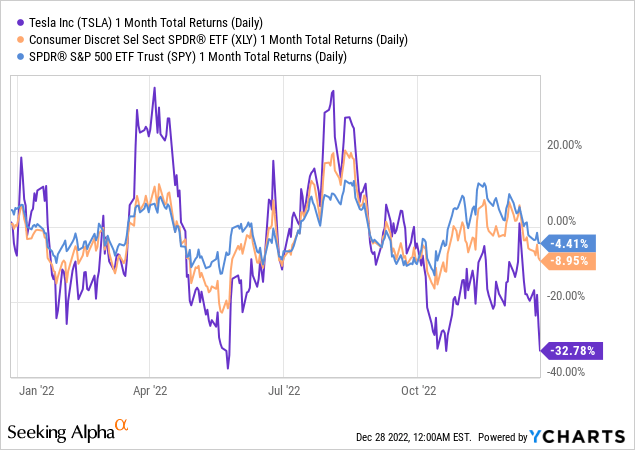

With TSLA floundering at the $110 level (down nearly 75% from November 2021 highs) at its last close, investors who chased the hype train got caught by the astute market operators who waited for TSLA investors to reach peak optimism. Of course, staunch TSLA bulls could argue that a 75% collapse from its peak levels is pretty common in this year’s bear market for high-growth stocks.

And they could also litigate that TSLA remains highly profitable relative to its leading EV peers, which even NIO (NIO) CEO William Li acclaimed in a recent commentary: “Overall profit for the industry, excluding Tesla, could be negative, given the huge spike in costs of raw materials for EV batteries.”

So what really went wrong for TSLA that it significantly underperformed the S&P 500 (SPX) (SPY) (SP500) over the past month? As seen above, TSLA notched a 1M total return of nearly -33%, compared to the SPX’s -4.4% return and the Consumer Discretionary Select Sector ETF’s (XLY) -9% gain.

Analysts/investors/media have heaped up multitudinous reasons: Twitter distraction, the slowdown in China, competition, macroeconomic headwinds, overinflated valuation, falling used car prices, and a “busted” growth story.

All these factors could potentially explain why TSLA has been hit, as no company is immune. Hence, when Elon Musk went on to urge significant caution against a severe recession, investors likely took it seriously.

However, bulls argue that TSLA’s collapse prior to Musk’s admonitions has likely priced in significant headwinds. Do they have a point? Yes, they do. We highlighted in an October article that TSLA’s PEG ratio dropped below 1x.

Obviously, with the recent battering, it’s lower now, despite the Street’s downgraded earnings estimates. Accordingly, TSLA last traded at an NTM PEG of 0.46x! Notably, TSLA’s dramatic collapse has caused its valuation to crumble, as its NTM P/E fell to 20.3x. As such, its growth premium against SPX’s NTM P/E of 16.7x had narrowed tremendously to 21.5%. Hence, we believe TSLA’s valuation is more attractive now.

We held a speculative view previously, which we closed well before the steep collapse, as it triggered our stop-loss level. However, with the price dropping into the $110 level, we assessed it had entered our high conviction zone.

Interestingly, we telegraphed to our members in June 2022 that we would not add TSLA as a core holding (meaning not speculative, and ready to hold steadfastly) until it reaches our high-conviction price level. We highlighted:

So, at what price could TSLA look interesting again? Our prognosis is that the market could easily take out the $540 level [post-split: $180] if the [market] flow remains bearish. Based on our reverse cash flow analysis, the market is unlikely to support that level, given its change of trend. Therefore, we think if the market has decided to turn its back on TSLA, given the negative flow, it’s looking to digest those massive gains from 2020-21. Hence, we urge members to be patient with TSLA [until the $110 level]. It could be an extended deep freeze. – Ultimate Growth Investing Tesla Update (23 June 2022)

And here we are, right at the $110 level. Is it reasonable to expect Tesla to turn the tables from here? Yes, it’s possible. But Why? TSLA’s behavior over the past month suggests massive capitulation forced by market operators.

So, who could have been forced to give up their shares? Remember Elon Musk warned about margin debt recently? He accentuated:

I would really advise people not to have margin debt in a volatile stock market and, you know, from a cash standpoint, keep powder dry. You can get some pretty extreme things happening in a down market. – Bloomberg

Could investors have been forced to bail out, given the rapid forced-selling maneuvers emblematic in TSLA’s price action? Why not? Also, note that the general public owns a relatively significant percentage (41%) of TSLA’s shares.

Therefore, it’s also possible that weak holders/speculative traders/overleveraged investors got caught in the massive downdraft, exacerbating the selloff. Also, short-sellers could also have been encouraged to reload their bets, as they have finally nailed their thesis in 2022.

WSJ reported in a December update that short-sellers had reaped $15B of gains in 2022. As such, we believe short-sellers who got burnt in its massive run-up toward its 2021 highs likely returned for the “revenge trade.” Known short-seller Andrew Left of Citron Research articulated:

Mr. Left, who was previously burned by his short position, says he promised himself at one point that he would never trade Tesla again. This summer, though, he says he began to get “FOMO,” or a fear of missing out, and he jumped back in. Mr. Left said he closed his position Thursday at a profit but sees room for the shares to fall further. “It’s still an expensive stock,” he said. “By no means is this over. As most stock traders will tell you, things don’t go from expensive to fairly priced. Things normally go from expensive to cheap.” – WSJ

We would have asked Mr. Left why did he close his short bets if he thought the collapse was “by no means over?” He should have reloaded more and doubled down on his conviction. Therefore, it could also point out that other bears could also be less convinced of another dramatic fall from these levels if they refrained from reloading.

Does it mean that TSLA is going to do an about-turn? Absolutely not. We have yet to glean a sustained bullish reversal or constructive price action.

However, we saw significant signs of likely capitulation that can be construed in a reverse fashion of the vertical rocketship that formed its November 2021 highs.

Hence, we assessed that the reward/risk profile has been significantly de-risked, and it’s time for investors to consider adding exposure as a core holding.

Rating: Buy (Upgraded from Speculative Buy)

Be the first to comment