Introduction

Teck Resources (TECK) has been hit hard by the current turmoil on the commodity markets due to the corona virus as well as due to its batch of weak quarterly results in Q4 2019 resulting in a net loss due to an impairment charge on the value of its Fort Hills oil sands project. Unsurprisingly, Teck also decided to withdraw its application to get the Frontier oil project permitted as the current economic circumstances don’t make much sense.

Q4 was substantially weaker than expected as Fort Hills appears to be a mistake

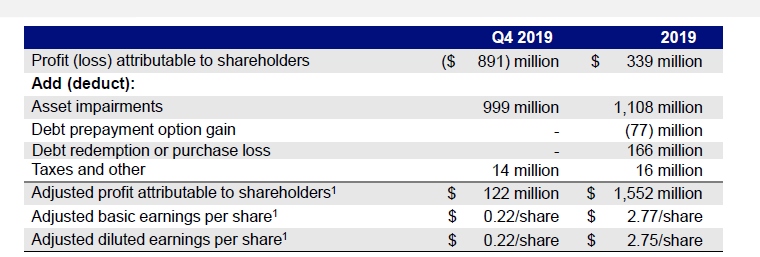

Despite an excellent performance of Teck in the first nine months of the year, the final quarter was weak. Even if we would ignore the impact of the impairment charges on the net income, the adjusted net income was just C$122M or C$0.22 per share. That’s a 75% drop compared to the same quarter in the preceding year.

Source: company presentation

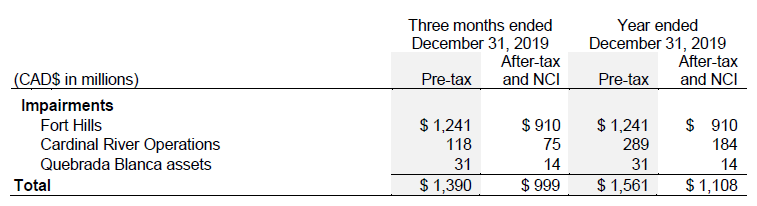

And that’s the adjusted net income. The bottom line of the income statement shows a reported net loss of C$891M predominantly due to a C$999M impairment charge on the Fort Hills oil sands project where a pre-tax impairment charge of in excess of C$1.2B was recorded. Additionally there were some additional impairment charges on the Cardinal River asset (an additional C$75M after tax on top of the C$109M that was already recorded earlier in 2019) while the Quebrada Blanca assets also saw a negligible value decrease of around C$14M after tax.

Source: press release

The impairment charge of Fort Hills comes after re-determining a reasonable oil price for the heavy oil the project is producing. Under the new valuation approach, Teck is using the current WCS price as base-case pricing for 2020 and a longer-term price of US$50/barrel (from 2024 on). This indicates that although the value of the asset already has been impaired, additional impairment charges cannot be ruled out if it’s looking like the forecasted price for 2024 cannot be met.

That being said, a reported net loss of this magnitude and a marginal adjusted net income are a bitter pill to swallow, and some investors who have read the previous articles where I focused on the sustaining free cash flow had a tough time to cope with this:

Source: The Investment Doctor Inbox on Seeking Alpha

Impairment charges have no impact on the cash flow generation

And sure, the free cash flow in the final quarter of the year was disappointing. Even after adding back the asset impairments the reported operating cash flow in the fourth quarter was just C$782M but this included a C$210M contribution from working capital changes but excludes the C$43M lease payments, the C$5M payments to non-controlling interests and the C$71M in interest expenses. On the positive side, it does include a C$71M tax payment although the impairment charges mean no taxes would be due over the Q4 result.

If we include all these elements, the adjusted operating cash flow was just C$524M. That sounds like a lot of money, but considering Teck generated a full-year adjusted operating cash flow of C$3.37B , it’s pretty clear Q4 was weak. No free cash flow was generated as Teck spent more than C$1B on capex and capitalized stripping, but keep in mind this includes the Quebrada Blanca 2 project which should be considered a growth project.

Perhaps we should have a look at the capex guidance for 2020. In 2020, Teck expects to spend C$1.73B on capex (up from C$1.57B) excluding the Quebrada Blanca investments which are expected to be C$2.42B (and will be funded by incoming payments from the partners and the specific project financing which has been put in place). Additionally, Teck is planning to spend C$625M on capitalized stripping (down from C$680M) for a total capex of C$2.35B.

This indeed means the full-year capex will exceed the annualized adjusted operating cash flow in the fourth quarter (annualized operating cash flow: C$2.1B) and the ongoing uncertainty in the commodity markets (also fueled by the Corona virus scare) means we should expect another weak and very likely weaker quarter in Q1 2020. While the copper and zinc output will remain relatively stable based on the full-year guidance, Teck has reduced its volume expectations for coking coal to 4.8-5.2 million tonnes and the Red Dog zinc mine which will see a 20% output reduction to 135-140,000 tonnes of zinc in the first quarter.

Source: company press release

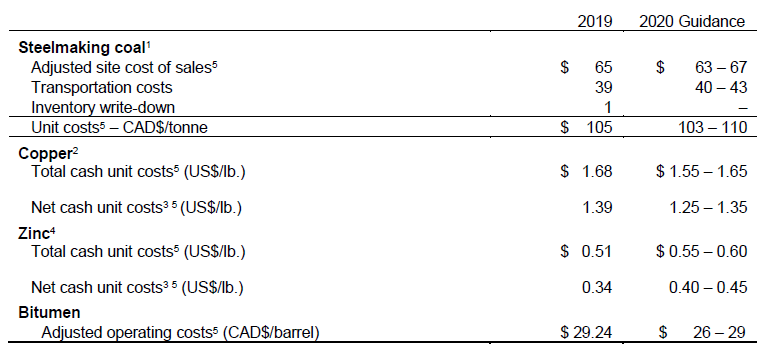

Fortunately the production cost guidance appears to be fine as most commodities will be produced at a similar production cost compared to 2019 although the cost guidance is also based on the full-year result and due to the lower volumes in Q1, the cost per tonne of coal and zinc may be higher in Q1 and subsequently trend down throughout the year.

Source: company press release

It’s great to be able to keep the production expenses under control, but as the steelmaking coal was fetching an average price of just C$173/t (compared to C$253/t in the final quarter of FY 2018), the pressure on the revenue will continue and the key to unlock higher cash flows will be in a higher coking coal price. A C$20 bump in the coal price will boost the operating cash flow by approximately C$350M after tax and provide a bigger margin of safety.

But let’s go back to the capex guidance. We already know not all capex is equal and the C$1.73B capex guidance includes C$810M earmarked for “major enhancement” purposes (including a non-recurring C$390M investment in the Neptune Bulk Terminals in the coal segment) and new mine development, and the sustaining capex is just C$920M. This, combined with the capitalized stripping which is a cost that usually cannot be postponed as mining operations need to continue uninterrupted results in a total sustaining capex of around C$1.55B for 2020. Fortunately Teck will be able to cover this with the incoming operating cash flow, even at slightly lower commodity prices.

Investment thesis

Some investors don’t appear to realize one should not invest in Teck on a quarter-to-quarter basis, but to gain longer-term exposure to steelmaking coal, copper and zinc. Do you believe in the future of those commodities (or at least one or two of them)? Then Teck Resources is an excellent way to boost your exposure to those metals. The company’s share price will move in line with the evolution of the commodity prices, and while there will be additional short-term pain, Teck should be considered by people with a longer-term view.

Given the amount of capex to be invested in enhancement and growth I don’t expect Teck to be a major cash cow this year (unless the commodity prices provide us with a positive surprise later this year). But rest assured that based on the adjusted operating cash flow in Q4, Teck will be able to fund its sustaining capex and stripping expenses. And balance sheet wise with a net debt of C$3.8B and a debt ratio of 1.5 (based on the reported EBITDA. Using the adjusted EBITDA the debt ratio would be less than 1), Teck’s balance sheet is in a shape that’s good enough to weather the current storm.

I have a long position in Teck and added on the dip. As I have a long-term investment horizon I’m not too alarmed by weaker periods. It’s inherent to the sector Teck is operating in.

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!

NEW at ESCI: A dedicated EUROPEAN REIT PORTFOLIO!

Take advantage of the TWO WEEK FREE TRIAL PERIOD and kick the tires!

Disclosure: I am/we are long TECK. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment