sanfel

Back in June 2020, I wrote an article on Tanger Factory Outlets (NYSE:SKT) that it was time to chase the yield. Back then, the dividend was listed at more than $1.40 on the website. There was a lot of speculation about a dividend cut, but the dividend was raised on April 10 to an official annual rate of $1.10. The stock price has soared from $7.71 at the time of the published article to the current price above $26. The current yield on that original investment is still above average. This is now a recognized stock with a decent future. It may not be the bargain it once was. But good management is nearly always worth a consideration by an investor.

The time to think about dividends and income is when a stock is left for “dead” because the challenges appear to be insurmountable. Back then I was getting comments about no growth ever again because the situation looked dire. Yet here we are about 3 1/2 years later (give or take) and not only is the situation not dire, but things have returned to normal.

The key is that many income stocks that interest investors have high yields that only go one way (and that is generally not up that much in the long run). But an undervalued situation like Tanger gave income and other investors a chance to get in at a time when anyone would tell you that the successful future the company needed was impossible.

Financial Strength

However, financially strong companies nearly always recover and go on to still higher highs whenever they hit a bump. Most good management teams are much better equipped to deal with “bumps” than the average management team. In the process, they often make up for “lost time” as well.

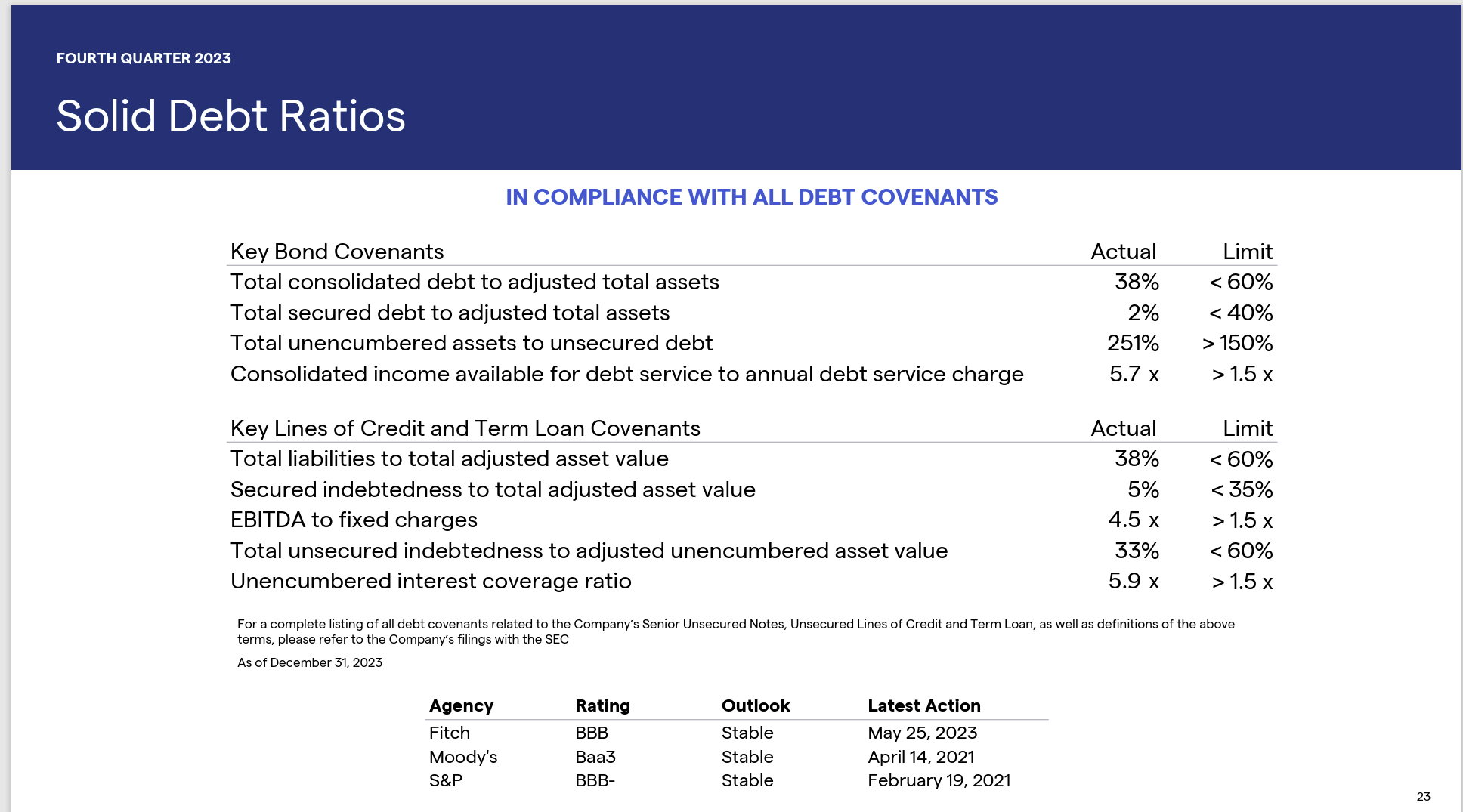

Tanger Factory Outlets Debt Ratio Summary Fourth Quarter 2023 (Tanger Factory Outlets Corporate Presentation Fourth Quarter 2023)

Clearly, this remains a financially strong company. There is a lot of unsecured debt and very little secured debt. Any company with the debt ratings shown above has adequate access to the debt market whenever that access is needed.

It is very unlikely that the current interest rate levels pose a long-term threat to profitability. With many of these companies, it would take years of high rates to have a significant impact. Many of these companies buy a few assets and possibly sell a noncore asset or two along the way. There are tenants that move out or go broke while new tenants move in. It does not take a lot of activity to keep the company ahead of any interest rate threat.

Right now, the market is focused on interest rate decline potentials. That is even better for a company like Tanger that will generally carry a fair amount of debt.

Business Difference

Tanger is a company that owns outlets. The old anchor store strategy is not even an issue here. That alone makes a big difference when it comes to worries about being saddled with any type of fixed contracts or low profitability contracts.

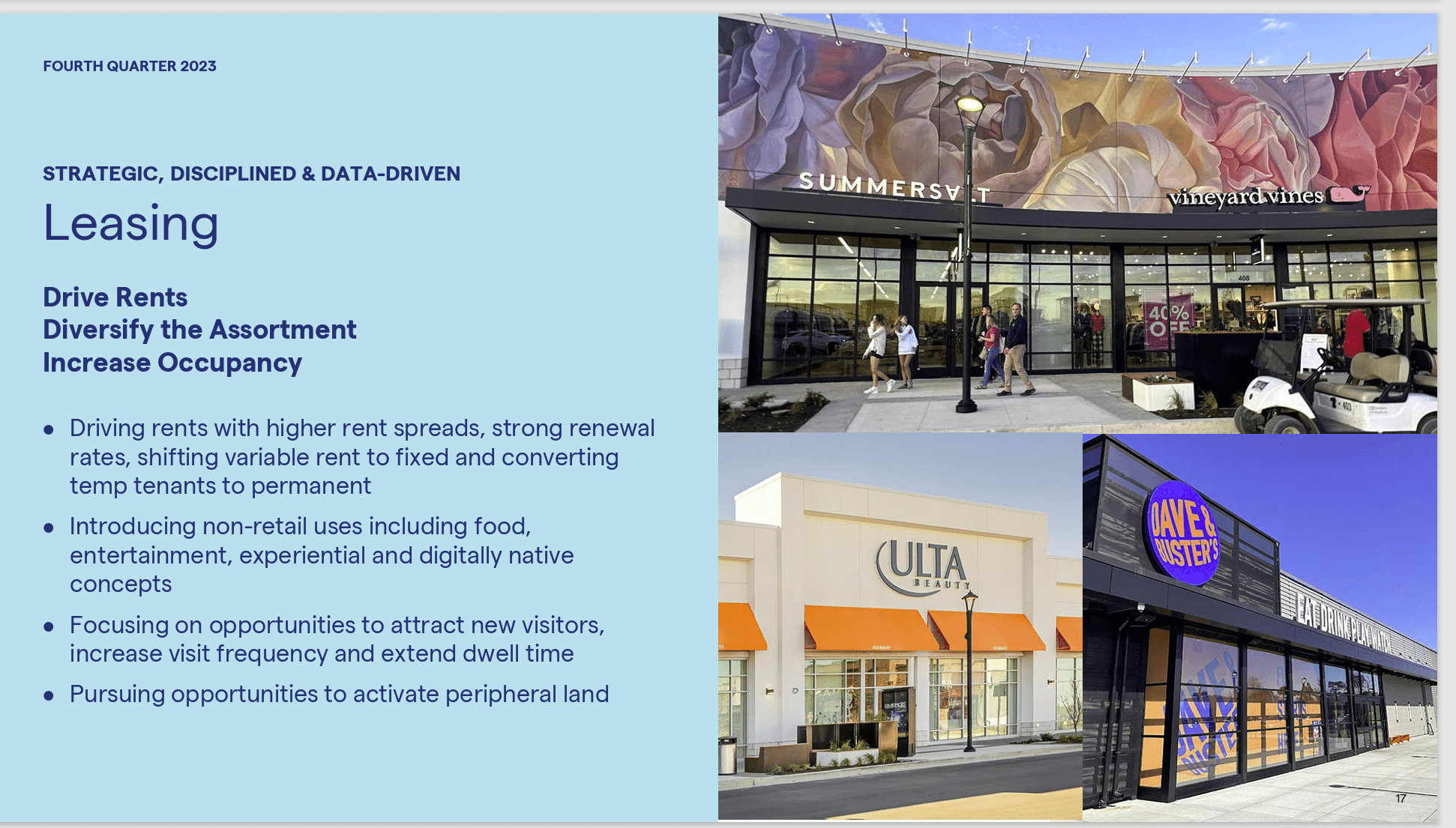

Tanger Factory Outlet Centers Leasing Strategy (Tanger Factory Outlets Corporate Presentation Fourth Quarter 2023)

As a result, the company has far more flexibility than a lot of other REIT’s when it comes to adequate profitability. There are not nearly as many of these REIT’s as there are ones that own malls (of any kind) or even single store structures.

That implies a little less competition in this business that can lead to slightly higher profits.

Furthermore, while the location of the company outlet malls is usually favorable, it is not what traditional retail would normally look for in a location. That agrees with management’s claim about lower entry costs. The situation may well attract more business as time goes on. But that just leads to higher traffic for the mall outlet, while often maintaining a cost advantage over more traditional malls.

Growth

Now, with the fiscal year 2020 challenges behind the company, the growth that looked like such an impossible task has now returned to business as usual. Whether it was worth the wait or the risk to wait and see if it happened is, of course, up to each individual investor.

But your chances improve considerably, when investment grade companies are the considered recovery idea. Even if that company temporarily loses the investment grade rating, the odds of a recovery and then on to more growth are considerably greater than the more speculative ideas (generally).

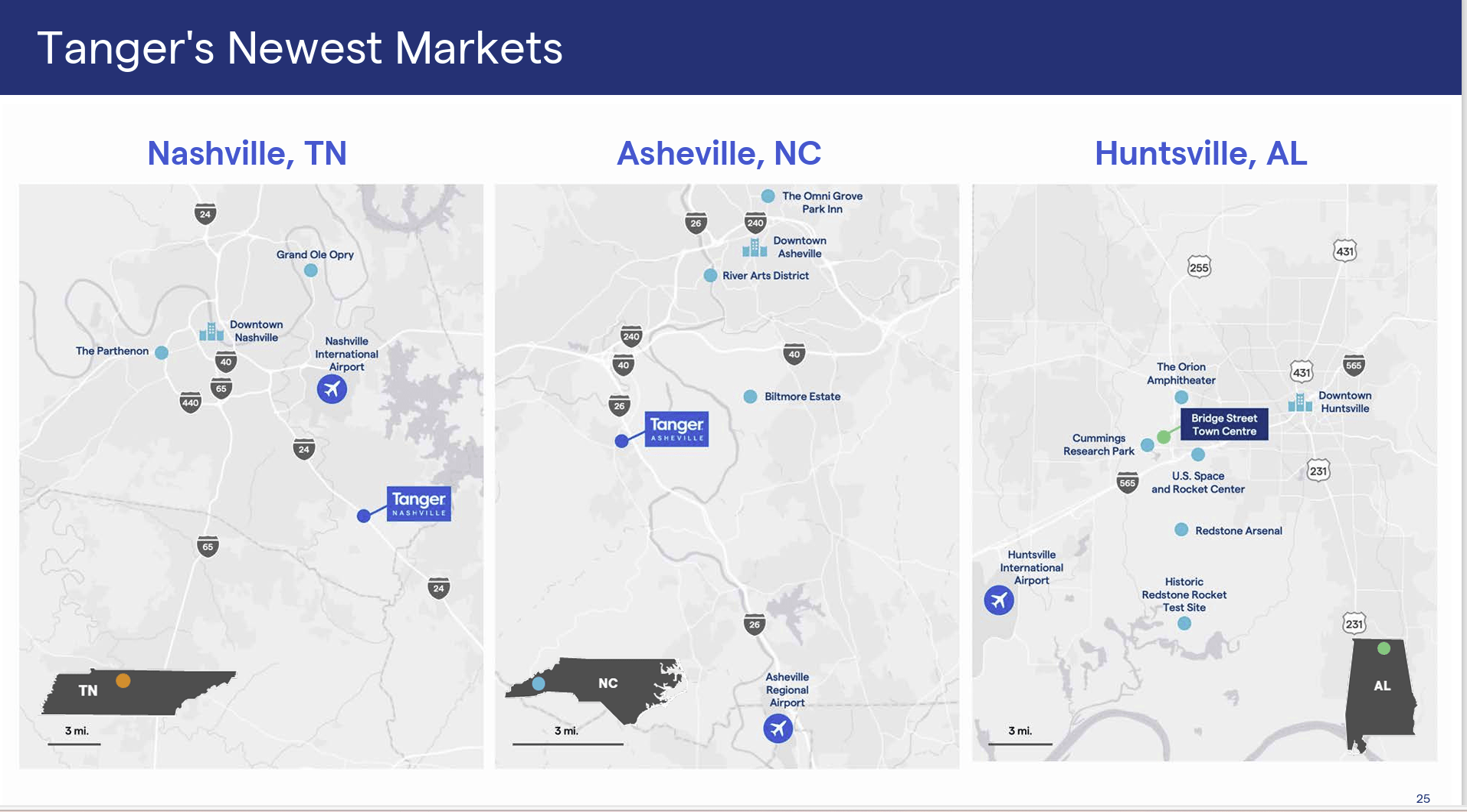

Tanger Factory Outlet Centers’ Growth Projects (Tanger Factory Outlets Corporate Presentation Fourth Quarter 2023)

Back in fiscal year 2020, the immediate growth from the point of that first article was to refill the vacancies created by the coronavirus demand destruction. But holding back the stock (among other things) was the idea that the company could not grow.

Very few had any idea that things would return to normal, and the above slide would happen. This company has long grown through a combination of opportunistic purchases that can happen at any time, as well as organic growth. Both of those are in the above slide.

It took a few years, but clearly the stock price at the time had no future priced in. Now, there are still many that do not include a future of more organic growth and opportunistic purchases unless the company announces those projects. Yet, as the 2020 article demonstrates, clearly future growth compared to back then happened. It will likely happen in the future, even if the investor does not know where.

Diversification

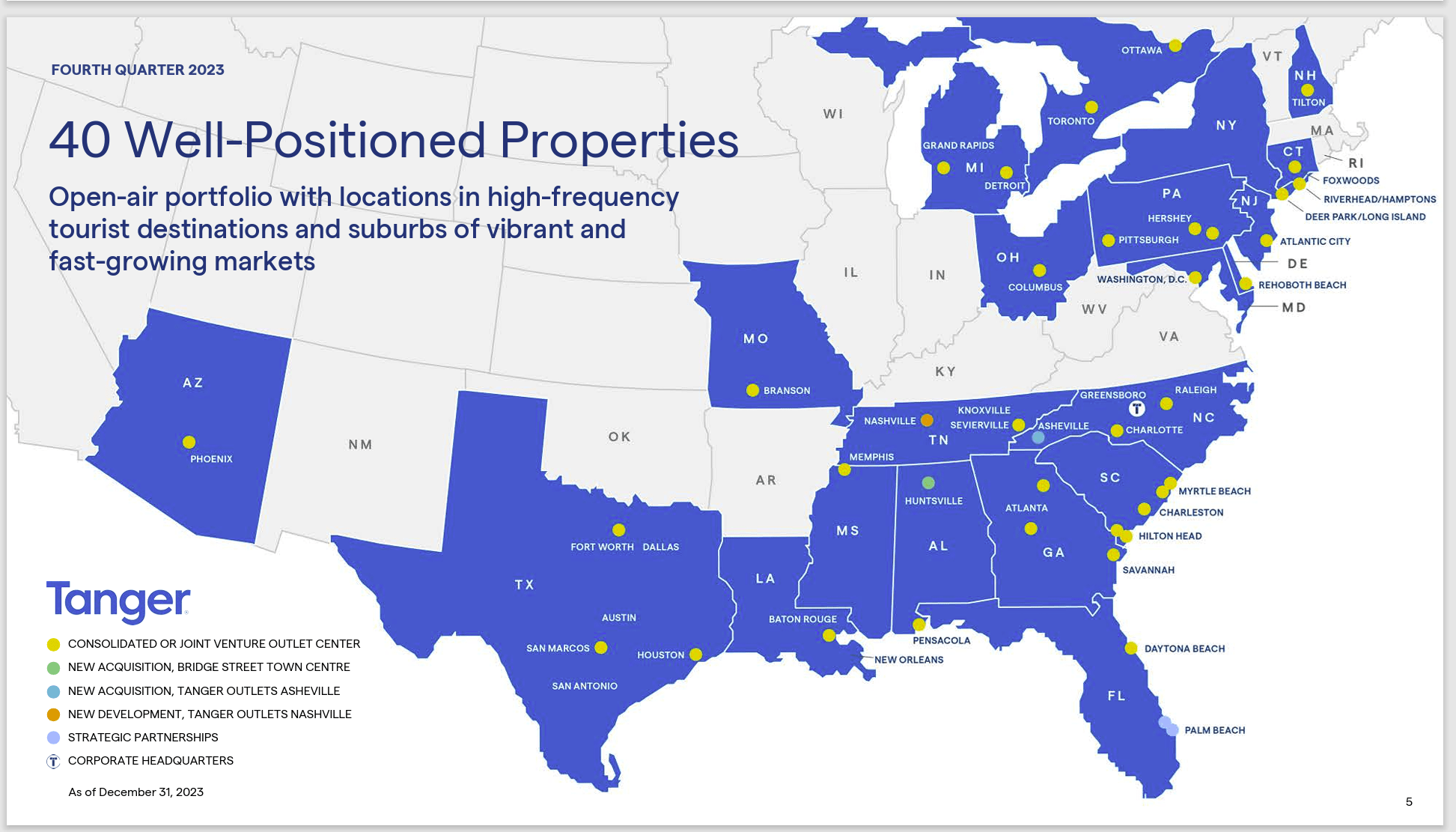

This company is well diversified in some of the fastest growing areas of the country.

Tanger Factory Outlet Centers Map Of Operations (Tanger Factory Outlets Corporate Presentation Fourth Quarter 2023)

This places the company in a position to produce above average growth simply by executing reasonably with the properties already in the portfolio. After all, more population can be translated into more business at the same location if management knows what it is doing.

Management has also mentioned that some of these properties have unused acreage that can be a basis for some organic growth as well.

Conclusion

Tanger Factory Outlet Centers is not the bargain that it once was when I wrote my first article. However, I am a firm believer in investing in good management. This stock still does not really reflect the superior abilities that this management team has demonstrated.

This is the kind of company that will likely find ways to grow that stock price in the teens, with the record to support that long term growth until the story changes or a key person retires. Not every company has the value laid out in front of you when that value is in superior management. That makes this one a continuing strong buy consideration.

However, as fiscal year 2020 demonstrated, the stock could have some downside potential in any economic downturn as it is considered part of the retail investment category.

Nonetheless, I suspect the future upside potential with this management team guiding the company is well above average. Investors can expect new outlet malls combined with an occasional purchase and joint venture. To me that makes this a buy for investors not already in for a starter position and then investors can decide later whether to buy more. Dollar cost averaging may prove to be the way to go here.

For me, I will not sell this unless the growth story changes, or management adversely changes. I tend to buy good management and hang on as long as that management is there. Rarely does a stock become so overpriced that it is an obvious sell. If that happens, we all would likely know it and know what to do.

Be the first to comment