JasonDoiy

Roblox’s (NYSE:RBLX) performance has stabilized in recent quarters, with the company returning to robust growth and its cash flows improving. Despite this, the stock has struggled in recent months, and absent a change in app store policies, it is difficult to see Roblox’s prospects changing materially.

Roblox’s stock has performed in line with the broader market since I last wrote about the company in October 2023. At the time, I suggested that modest growth and large losses were a near-term problem, but there was potential in the long run if Roblox could improve its cost structure. AI should reduce the burden of safety and trust costs, as should a maturing user base, but this will take time. Changes in app store policies could have the most impact, although this situation remains fluid.

The stock probably performs ok in the short run, provided growth remains solid, as this will support cash flows. Roblox’s cash flows are largely a function of the timing of payments though and do not reflect the profitability of the platform.

Market Conditions

Roblox’s current business model probably means that it is fairly isolated from macro conditions. On average, users spend modest amounts on the platform and advertising isn’t a material part of the business yet. Roblox’s recent soft growth is more likely to be the result of COVID pulling forward demand than sensitivity to economic conditions.

While there have been difficulties in other parts of the gaming market, this could provide Roblox with a small tailwind. A large number of developers have been laid off in recent years, which could contribute to growth of Roblox’s developer community. The company’s future is more tied to its ability to pull paying users into the ecosystem though.

I expect fairly robust growth from Roblox going forward and consider the company’s cost structure far more important than the demand environment. In this regard, mounting regulatory pressure on big tech companies could be a positive development, but this will likely take time to eventuate. In particular, the Digital Markets Act in the EU has the potential to make app side loading a viable alternative, lowering the burden of platform fees. So far, it appears that there will be little meaningful change though, and Roblox’s guidance assumes that the status quo is maintained. While companies like Apple are complying, this has been characterized as superficial and has been done in a way to ensure there is no real change. I think it is likely that the burden of app store policies will decline over time, but based on recent events I think this still could be years away.

Roblox Business Updates

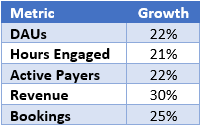

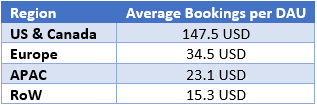

Roblox has seen strong performance across metrics in recent quarters, which is positive for the long-term health of the platform. Roblox’s 13-an-over cohort increased 28% YoY in Q4 and now constitutes 58% of the total user base. This is particularly relevant for Roblox’s advertising business. User growth has been fairly solid across geographies, with Japan and India both areas of particular strength in Q4. While this is a long-term positive, it is currently weighing on overall average bookings per DAU.

Roblox was recently made available on PlayStation and Meta Quest, which should support near-term user growth. Voice DAUs were up 161% YoY in Q4, with Roblox stating that this feature improves engagement and retention. It is also an important part of Roblox’s desire to become more of a social platform.

Table 1: Roblox Q4 Business Metrics (source: Created by author using data from Roblox) Table 2: Roblox Average Bookings per DAU by Region (source: Created by author using data from Roblox)

Roblox continues to introduce functionality to increase the appeal of its platform to both users and developers. This includes more advanced avatars, with features like facial animation. The company has also suggested that AI will eventually be available to generate avatars. Roblox recently announced its own AI model for real time AI chat translation, which allows users from around the world to communicate with each other. A beta version of Roblox Assistant is also now available. This allows creators to use natural language to generate new ideas and code. Roblox also continues to work on voice and chat moderation. While this has the potential to improve the quality of the user experience, perhaps more importantly, it should lead to lower trust and safety expenses for Roblox.

Roblox’s advertising business is progressing, but the company has suggested that it is not yet material. Roblox had 69 brands on its platform in the fourth quarter and expects to continue scaling its advertising initiative in 2024 (1). The company will introduce more measurement capabilities for advertisers in 2024, which will be an important component of attracting demand to the platform. Roblox is also experimenting with physical shopping, which could help to create a closer loop for advertisers on the platform.

Financial Analysis

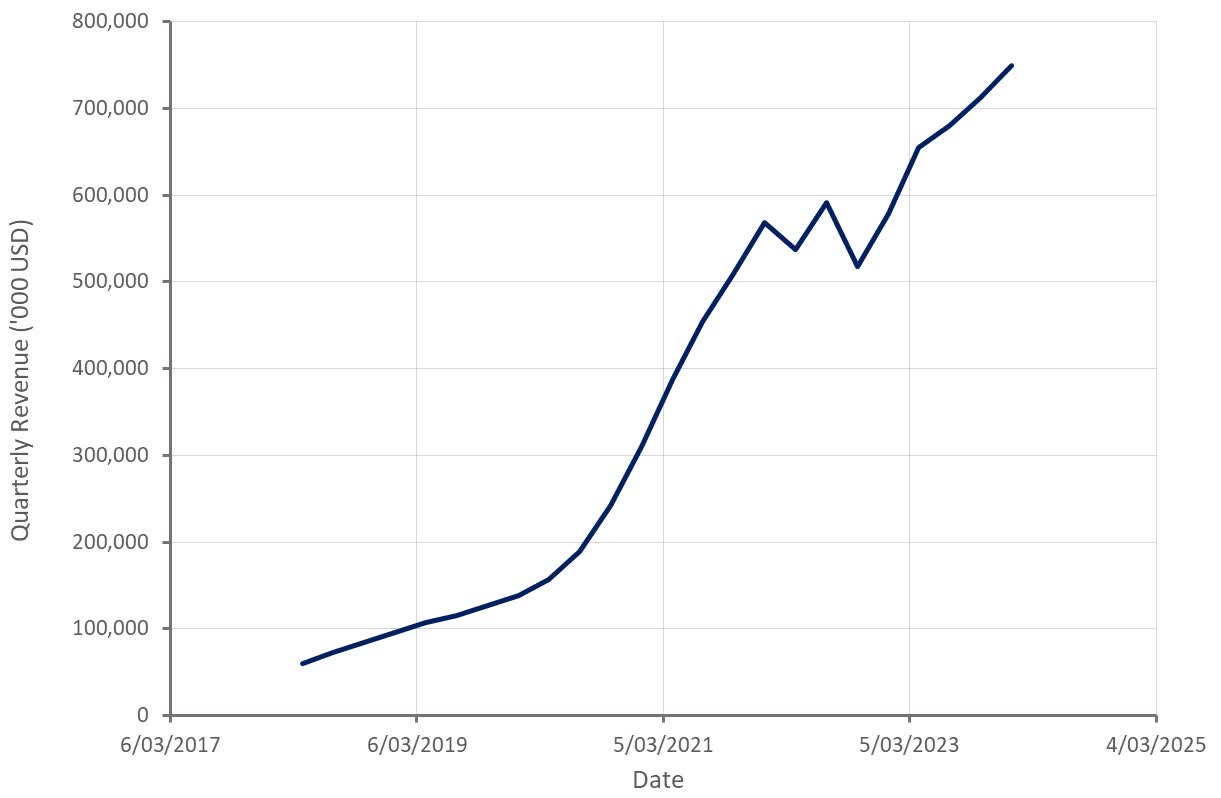

Roblox’s revenue increased approximately 30% YoY in Q4 to 750 million USD. Revenue growth was robust across regions, with APAC and RoW recording particularly strong growth. Bookings were up 25% YoY to 1,127 million USD. Roblox prefers bookings as a measure of business performance, as revenue is impacted by whether goods purchased are durable or consumable and the life of paying users.

Roblox continues to see growth in its payer community, although this is only broadly in line with growth of the user base. Average bookings per monthly unique payer have also been fairly flat in recent years, limiting Roblox’s growth. This figure was up 6% YoY in Q4 though.

Roblox is guiding to 755-780 million USD revenue in the first quarter, representing approximately a 17% YoY growth rate at the midpoint. Bookings are expected to be 910-940 million USD, up 20% YoY. Roblox expects 3,300-3,400 million USD revenue in 2024, an increase of roughly 20% over 2023. Bookings are expected to be 4,140-4,280 million USD, up 20% over 2023.

Figure 1: Roblox Revenue (source: Created by author using data from Roblox)

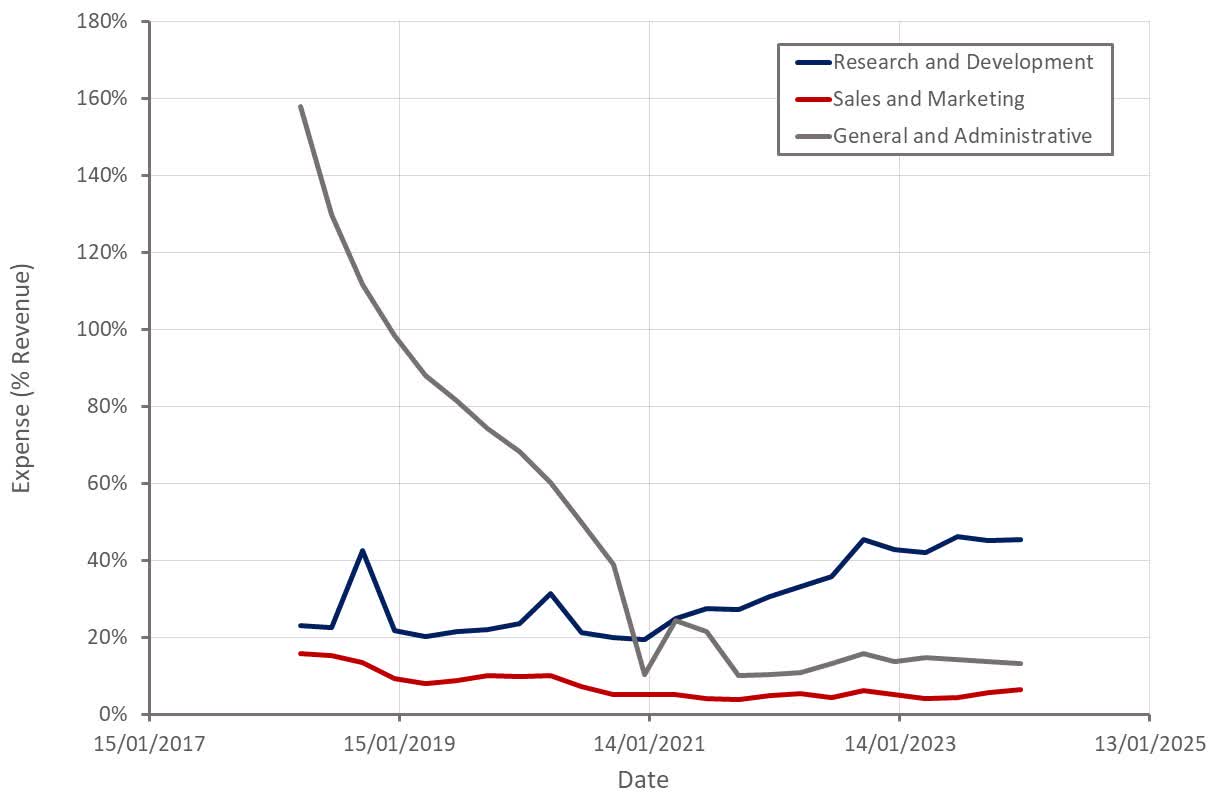

While Roblox’s growth has improved in recent quarters, the company’s cost structure is still concerning. Roblox spends large amounts on infrastructure, platforms fees, developer fees and trust and safety, which could all be considered part of cost of sales.

Roblox continues to invest a large amount in R&D but outside of this, its operating expenses are fairly modest. I typically think R&D is a good thing, but it is not really clear what outcomes Roblox is creating given how much it is spending.

Figure 2: Roblox Operating Expenses (source: Created by author using data from Roblox)

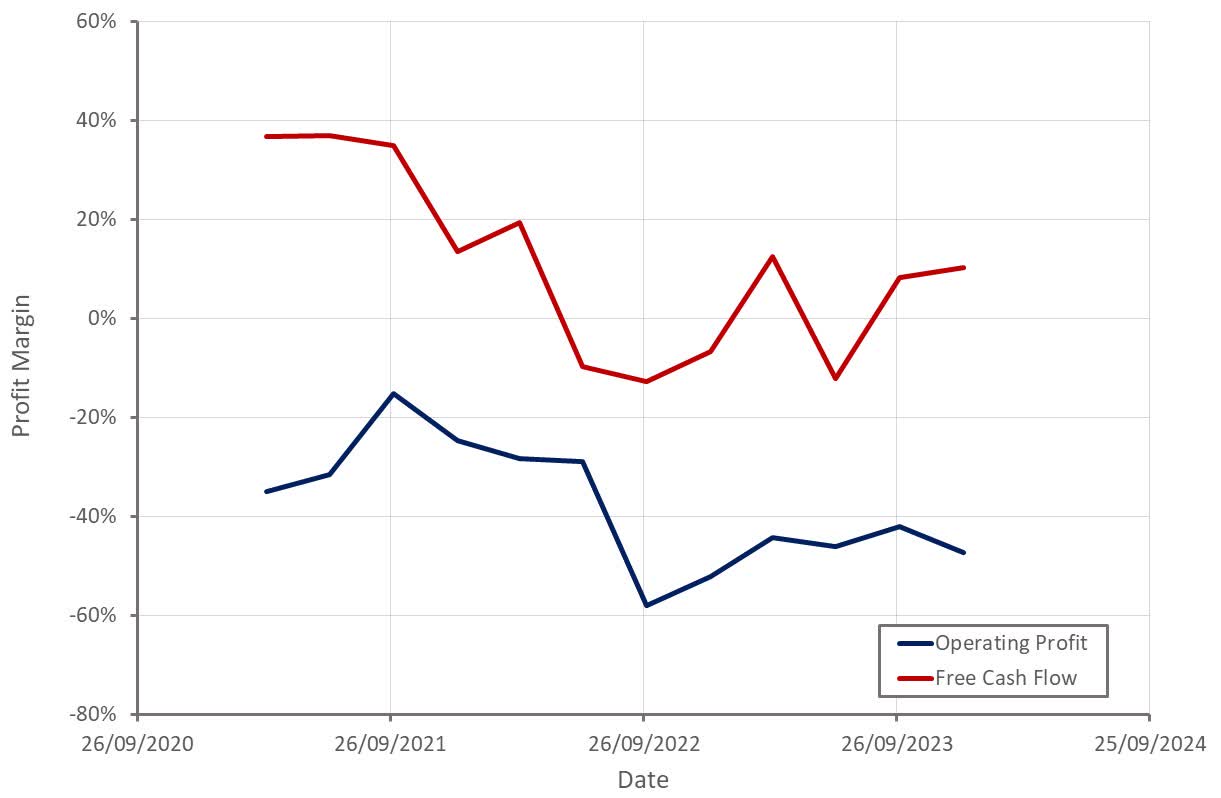

Roblox’s operating profitability and free cash flows have diverged in recent quarters as growth has picked up. This is largely a function of Roblox collecting payments from users far in advance of paying developers. While this is a genuine source of cash, it is only meaningful while the company is growing.

Figure 3: Roblox Free Cash Flow (source: Created by author using data from Roblox)

Conclusion

While Roblox’s share price is still down significantly from 2021 levels, its valuation is actually still fairly high, unless there is a fairly dramatic shift in the company’s cost structure. Roblox’s long-term profitability is questionable without a substantial reduction in infrastructure and trust and safety expenses. A change in app store policies would provide the most benefit, and while the regulatory landscape is supportive, it is still not clear what will end up happening. Advertising has the potential to support growth and improve margins, but this part of the business is not meaningful yet.

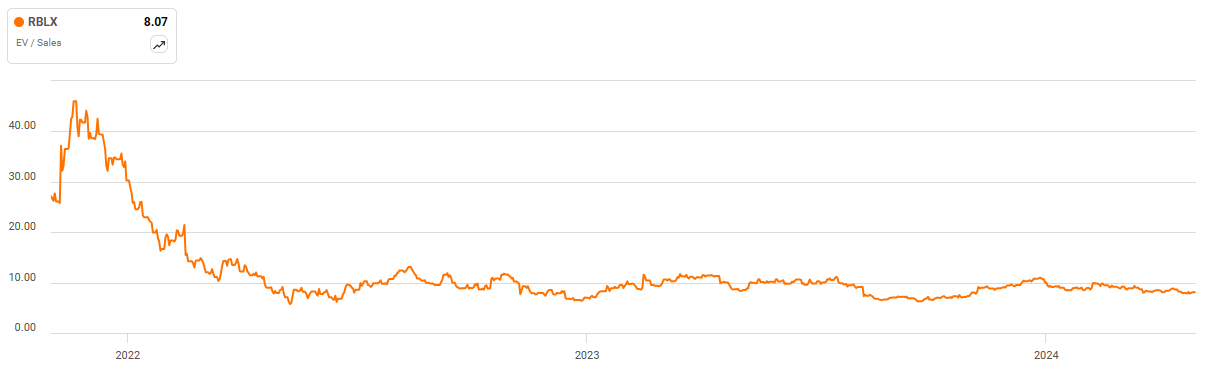

Figure 4: Roblox EV/S Multiple (source: Seeking Alpha)

Be the first to comment