JacobH/iStock via Getty Images

Since hitting multi-year lows last Fall, the shares of Rio Tinto Group (NYSE:RIO) have been on a relentless march upwards, appreciating well over 40% in recent months. Much of that has been due to rising iron ore prices which have gone from about $82/t in early-November to just below $130/t today. And as most readers are probably well aware, a lot of that had to do with the anticipation of Covid restrictions being lifted in China, the world’s largest importer of iron ore.

However, now that Rio’s stock has repriced substantially higher to take account of the reopening, a more cautious approach may be warranted. It’s worth remembering that China’s economy was slowing down even before the pandemic started, and several factors may prevent it from reaching growth rates similar to those of the past. Rio’s management appears to be well aware of that fact and has taken steps to grow the company’s portfolio through the purchase of lithium-producing assets. In this article, we’ll review those investments as well as the factors that may impact iron ore prices in the near future.

Company Background

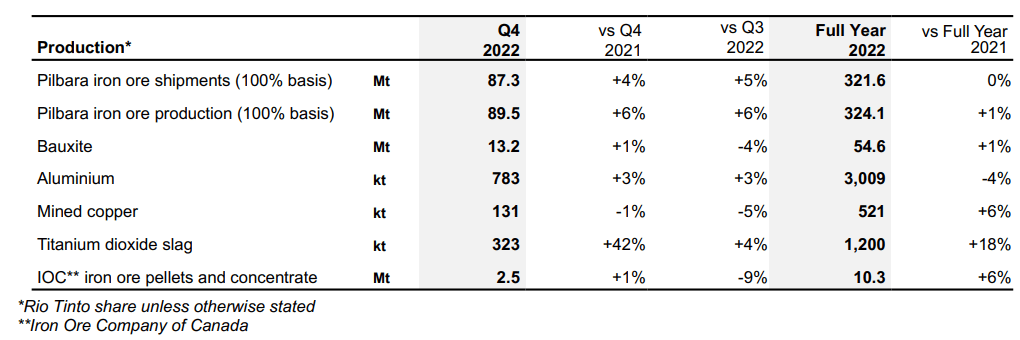

Rio Tinto is the world’s second largest mining company when measured by market cap, and similar to the other top global producers it makes most of its money through the extraction and sale of iron ore. As can be seen in the exhibit below, sales of iron ore made up almost 60% of the company’s revenue in 2021. And although 2022 revenue figures won’t be released until late-February, full-year production figures have been made public, and the results were largely similar to those of 2021, with the exception of titanium dioxide.

Rio Tinto 2021 Revenue Distribution (Author Using Financial Statement Information) Rio Tinto Q4 Production Report

Running such a large and geographically diversified company, Rio has operations in 35 countries, has its advantages. Incidents that are serious enough to halt production at a mine site such as accidents, breakdowns, or problems with local governments will often only have a minor impact on the company’s aggregate results. This leads to greater predictability of overall production and allows management to focus on growing or replacing existing production as well as considering options to expand into the production of other commodities.

It also allows Rio to pay a healthy dividend; although this may change when full-year results are announced, the stock paid an H1 dividend of $2.67 per share and currently yields 9%. The company paid out half of its H1 2022 underlying earnings of $8.6 billion, and this payout level probably won’t change as Peter Cunningham, Rio’s CFO, said during the Q2 earnings call that, “we’re just being very consistent on the dividend. Fifty percent is our sort of normal level.” However, while the payout may remain consistent, the dollar amount will probably be lower given that iron ore, copper, and aluminum prices were substantially lower during most of the second half of last year.

During the call, management also discussed the decision to reduce 2022’s capex budget by $500 million, bringing it down to $7.5 billion from the previous $8 billion allocation. This was due to currency fluctuations and changes to some projects. However, what was more interesting about Rio’s capex projections was not the 2022 number, but rather the amounts budgeted for 2023 and 2024. Management expects those line items to sum to between $9 billion and $10 billion per annum, of which $3 billion will be allocated to growth projects each year.

Investor Presentation

Lithium

Rio’s management intends to use part of that growth capex allocation to grow the company’s commodity portfolio, and they intend to do this by developing the Rincon lithium property that Rio purchased for $825 million in 2021. The lithium brine project is located in Argentina and had a resource estimate of 11Mt LCE at 373 mg/L when it was purchased. It is still in the very early stages of development, but in July of last year Rio announced funding of $190 million for the construction of a start-up plant as well as some early works infrastructure to support a full-scale operation.

Since then, the company has gone on to sign an MOU with the Ford Motor Company (F) that will cover lithium, aluminum and carbon. Rio’s management has said on multiple occasions that they view the energy transition as an opportunity for the company, and this point was reiterated during the Q2 call when Jakob Stausholm, Rio’s CEO, discussed the company’s intentions and said that he’s committed to investing in materials essential to the energy transition.

However, it should be noted that it is still early days for this initiative; as mentioned, Rincon is in early-stage development and Stausholm also seemed to rule out growing the project through acquisitions when he said, “I’m not too excited about doing too many things on the M&A front.”

So, given all of this, it seems that Rio’s fortunes will rise and fall with the price of iron ore for the foreseeable future. And that brings us to the disadvantages of running a large and geographically diversified mining company.

China

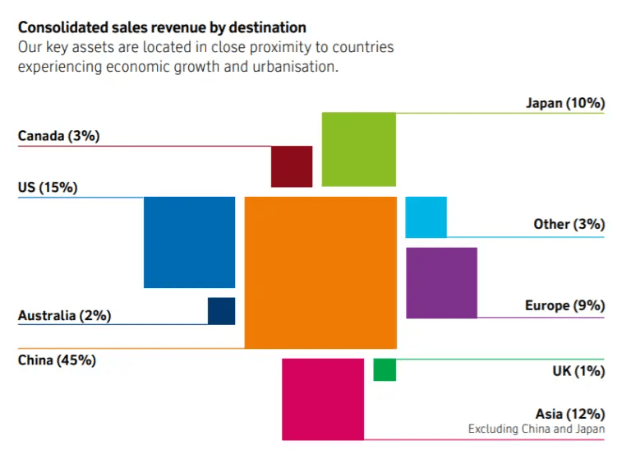

As most readers are probably well aware, the stocks of most explorers, developers, and even many small producers are often less correlated to the price of the underlying commodity than are the stocks of the senior producers. This makes having a good understanding of the macro forces driving the demand for that underlying commodity that much more important. And in the case of iron ore, the demand driver is the Chinese economy. And China is also Rio’s most important market.

Rio Tinto Annual Report

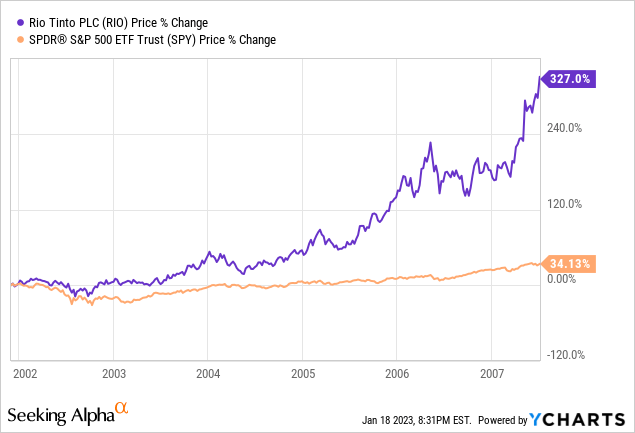

China’s golden years, in terms of its imports of primary materials, occurred during the five to six years following its entry into the World Trade Organization in 2001. During this period, China had a voracious appetite for all types of raw materials, and this resulted in the prices of resource stocks far outpacing the broader market.

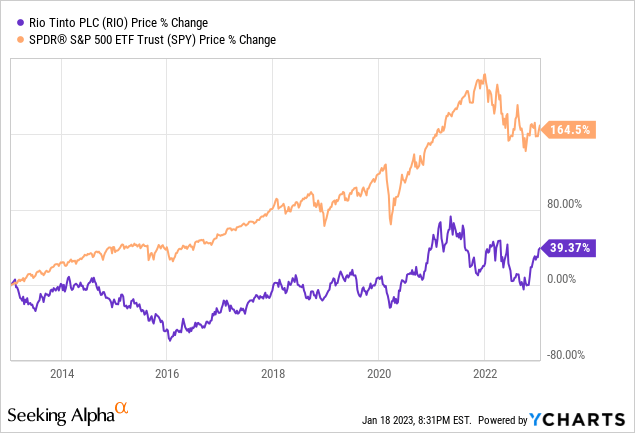

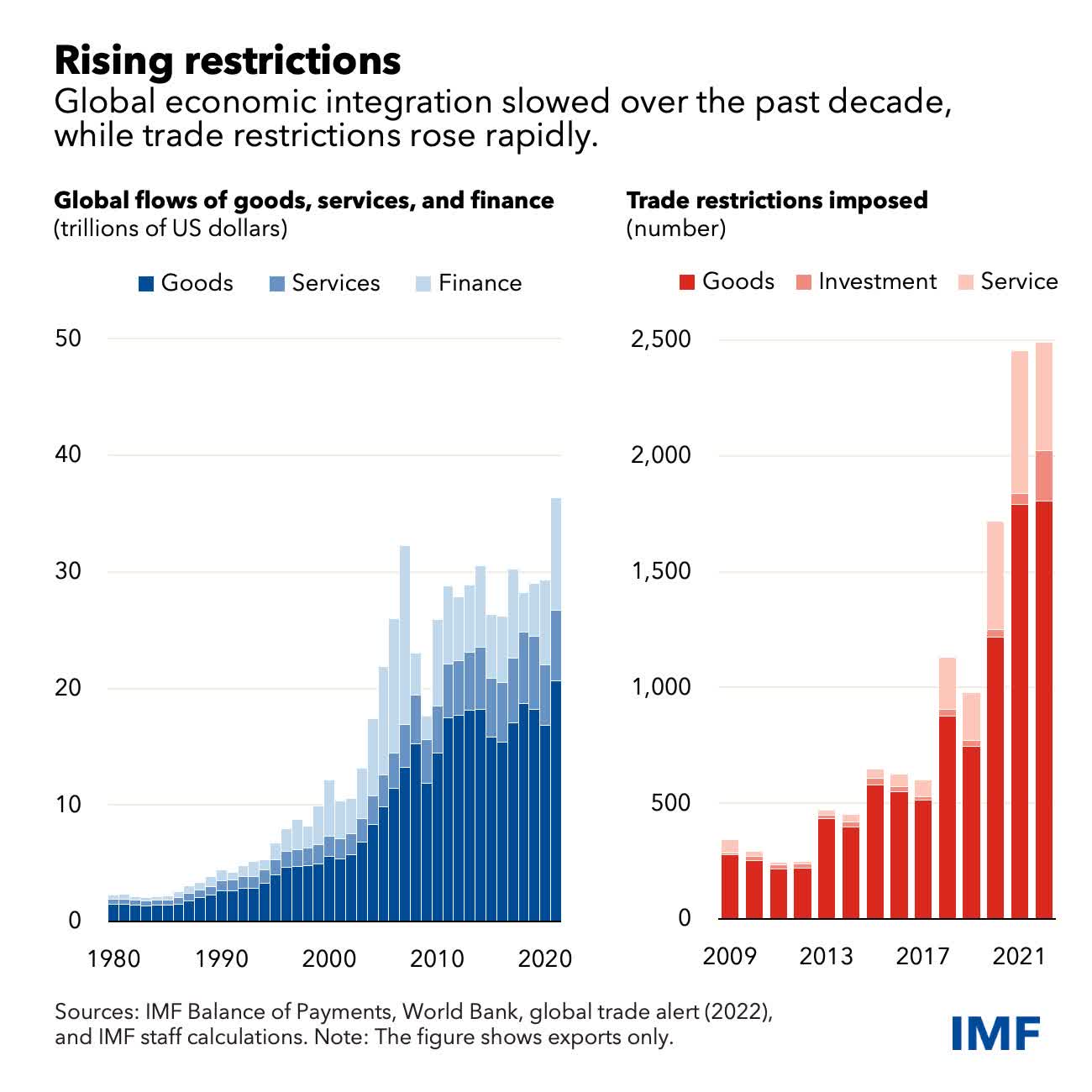

But over the last decade, the Chinese economy has cooled substantially, and this has resulted in a significant moderation to demand growth for base metals. The impact of this trend can be seen in the failure of Rio’s share price to keep pace with the broader market over that time period. And although China’s reopening from COVID lockdowns will provide some temporary relief, the exhibit below shows how the longer-term trend of increased trade restrictions driven by rising geopolitical tensions has resulted in the leveling-off of international trade flows. That is a trend that looks set to continue.

IMF.org

Takeaway

So, given these longer-term trends, as well as the fact that Rio’s stock has already risen substantially in anticipation of China’s reopening leads me to believe that the shares are fully valued at these levels. Granted, the company is solid, it pays a good dividend, produces commodities for which there will always be a need, and is implementing plans to grow its product portfolio; however, the fact that the macro environment holds a lot less promise than it did in years past leads me to be much more cautious. I currently rate the stock a hold and would only consider buying shares after a substantial pullback.

Be the first to comment