Hope Connolly

ResMed Inc. (NYSE:RMD) is a leading company that specializes in the development of digital health and cloud-connected medical devices. The company is well known for their continuous positive airway pressure (CPAP) devices and other solutions for the treatment of sleep-disordered breathing and other respiratory conditions. In addition to its CPAP products, ResMed offers a range of cloud-based software solutions for the management of sleep-disordered breathing and other respiratory conditions. Its AirView platform, for example, enables patients to remotely monitor therapy progress and adherence, thereby improving patient outcomes and reducing healthcare costs.

ResMed Inc. has established a strong brand reputation and continues to expand its product portfolio, positioning the company to take advantage of the growing sleep-disordered breathing market. However, RMD stock remains relatively expensive as of this writing, and its negative year-over-year growth outlook makes it a risky investment at current levels. As such, it is recommended to wait for a price pullback before considering investing in ResMed.

Company Overview

One of the interesting catalysts of ResMed Inc. is its continued effort to expand its operations and product offerings. In fact, as quoted below, RMD continues to experience positive demand growth as home sleep apnea testing becomes increasingly popular.

We’re seeing ongoing high demand for our sleep and respiratory care devices worldwide and we’re making steady progress, working with our suppliers to continue to increase our production to ultimately meet the needs of all customers and especially patients. Source: Q2’23 Earnings Call Transcript.

RMD is taking a proactive approach to shaping the future of out-of-hospital healthcare. As quoted below, they aim to be at the forefront of digital health technology and have already achieved significant milestones in this regard.

We are transforming out-of-hospital health care at scale, leading the market in digital health technology across our business. We now have over 13.5 billion nights of medical data in the cloud and over 19 million 100% cloud connectable medical devices on bedside tables in 140 countries worldwide. Source: Q2’23 Earnings Call Transcript

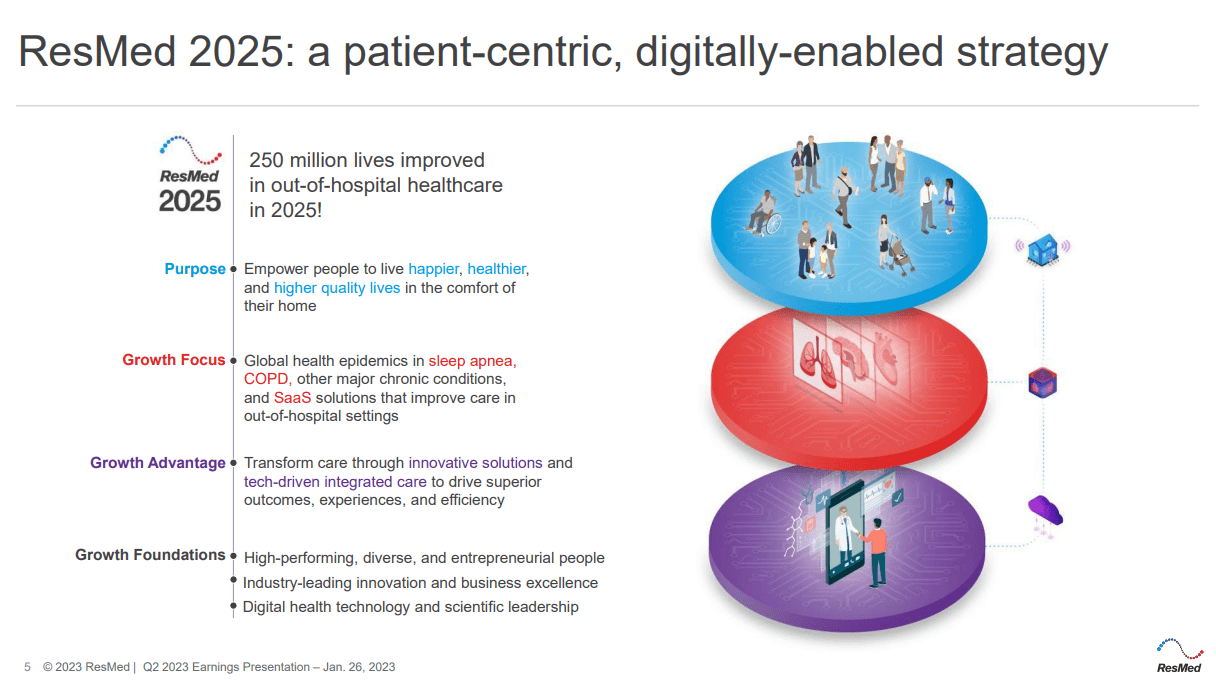

RMD: 2025 Targets (Q2’23 Earnings Call Presentation)

RMD is confident in their ability to improve the sleep and overall health care of 250 million people in 2025. In fact, they are gaining brand recognition in Japan with their latest AirSense 11 platform.

To that point, we introduced our newest product, AirSense 11 platform into the Japanese market during December and we looked forward to continuing to support doctors and patients in Japan with our world leading 100% cloud connectable medical devices and our cloud-based software technology. Source: Q2’23 Earnings Call Transcript

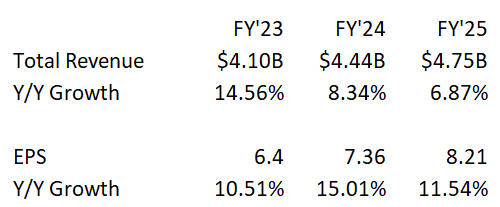

On top of this, unlike its peer Koninklijke Philips N.V. (PHG), which announced a potential huge layoff catalyst, ResMed Inc. surprisingly now has over 10,000 employees globally, up from 8,160 recorded in FY’22. With RMD’s record-high inventory level of $1,138.8 million, I believe they have sufficient capacity to continue revenue growth, as shown in the image below.

RMD: Slowing Y/Y Growth (Data From Seeking Alpha. Prepared by the Author)

However, the slowing projected Y/Y growth calls its high valuation multiples into question.

Slowing Cash Flow

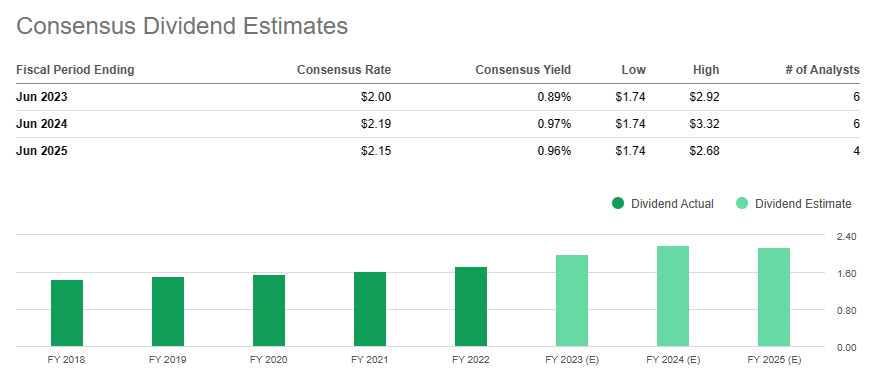

The significant decrease in cash from operations, currently trailing at $370.2 million compared to its 5-year average of $570.84 million, is largely due to the buildup of inventory. The management sees that it’s crucial to maintain current demand. However, I believe this to be a bold decision, given the current uncertain macroeconomic conditions, which could negatively impact the company’s gross margin in the future. Additionally, RMD has accumulated a record-high total debt of $1,939.5 million, which may result in additional yearly fixed expenses for the company in the form of interest payments. Given its slowing cash flow and rising interest obligations, it is reasonable to anticipate some disruption in dividend growth estimates, as illustrated in the image below.

RMD: Consensus Dividend Estimates (Seeking Alpha)

Relatively Expensive Than Peers

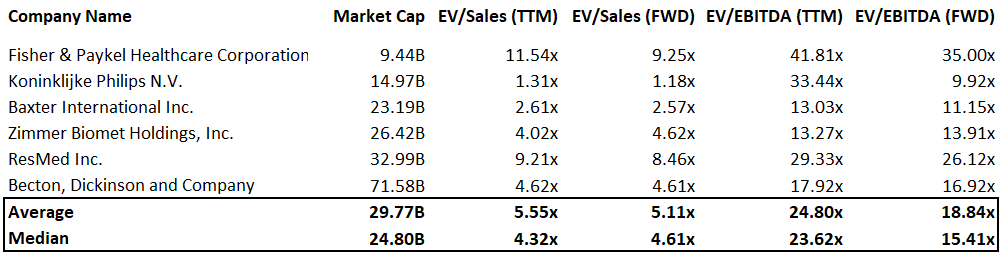

RMD: Relative Valuation (Data from Seeking Alpha. Prepared by the Author)

Peers: Fisher & Paykel Healthcare Corporation Limited (OTCPK:FSPKF), Baxter International Inc. (BAX), Zimmer Biomet Holdings, Inc. (ZBH), Becton, Dickinson and Company (BDX).

When comparing ResMed to its peers, the latter appears to be significantly more expensive. ResMed trades at a trailing EV/Sales ratio of 9.21x, which is relatively higher than the average EV/Sales ratio of its peers at 5.55x. Furthermore, when compared to its 5-year average EV/Sales ratio of 8.75x, it still remains unappealing. In fact, RMD has accumulated a record-high total debt level, amounting to $1,939.5 million, which will continue to impact its profitability through significant interest obligations. The same sentiment will apply, looking at its higher trailing EV/EBITDA than its peers’ average, as shown in the image above. Additionally, when considering ResMed’s forward EV/EBITDA ratio of 26.12x compared to the average EV/EBITDA ratio of its peers at 18.84x, it becomes clear that the company is trading at an unattractive premium. As previously mentioned, RMD appears to have a declining YoY growth outlook for both its total revenue and earnings per share, which raises questions about its high valuation.

RMD: Relative Valuation (Prepared by the Author)

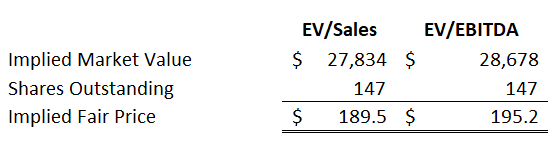

Despite the aforementioned concerns, using generous assumptions, we can arrive at an average fair price of $192.3 for ResMed. This estimate is based on an implied EV/Sales ratio of 7.50x, EV/EBITDA ratio of 23.82x, estimated total revenue of $4.10 billion, and EBITDA amounting to $1,327.5 million in FY’22, and a discount rate of 9%. As a result, as of this writing, there is no margin of safety, making the stock less appealing to potential investors.

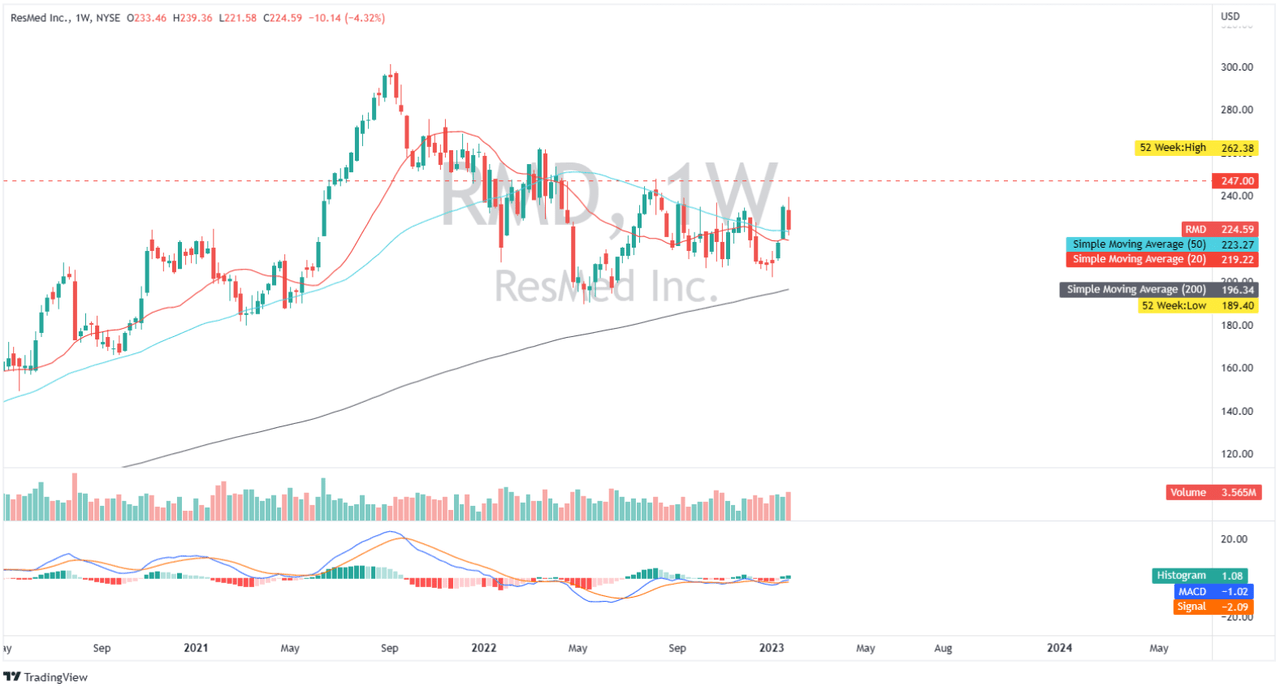

Trading Near Its Psychological Resistance: $247

RMD: Weekly Chart (Author’s TradingView Account)

ResMed is trading near its strong psychological resistance level around $247, as shown on the weekly chart. The market rejects RMD when it attempts to fully break through its 50-day simple moving average. If bearish pressure remains, RMD is likely to revisit its logical support at $190. If this happens, the current dividend yield of 0.78% will rise, as well as its current risk-to-reward ratio. Furthermore, its MACD indicator stays below zero, indicating that bearish sentiment should be monitored.

Final Key Takeaway

Putting the negative catalysts mentioned aside, ResMed Inc. should benefit from the increasing prevalence of sleep-disordered breathing and other respiratory conditions, coupled with the aging population in the US. In fact, as quoted below, ResMed’s management reassured its investors that it is also looking for a merger and acquisition transaction.

We will continue to identify and capitalize on synergy opportunities as we move forward. Source: Q2’23 Earnings Call Transcript

But the question is, how will ResMed Inc. finance it? As previously stated, ResMed Inc. has accumulated a record level of total debt, and it is experiencing declining cash flow to support dividend growth, which may jeopardize its M&A strategy. This makes ResMed Inc. risky in the short term; hence, potential investors should wait for a meaningful pullback.

Thank you for reading and good luck!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment