Surendra Sharma

This article was coproduced with Cappuccino Finance.

In the past couple of years, the real estate market has been in a roller coaster mode. At the beginning of the pandemic, the real estate price dropped like everything else.

Then, the Federal Reserve lowered the interest rate to near zero, and the government started pumping money in with stimulus and other benefits.

The combination of the two resulted in skyrocketing real estate prices around the U.S. Some regions experienced a buying frenzy with multiple offers on the first day of listing.

But as inflation started to climb and the Federal Reserve started tightening up the monetary policy, this caused higher mortgage rates. The high mortgage rate dampened demand substantially, and the volume of existing home sales dropped for almost a year straight.

In this frenzy, mortgage REIT (real estate investment trusts) have experienced a large roller coaster ride as well. After performing very well in 2020 and 2021, mortgage volume dropped substantially in 2022, and the negative sentiment in the real estate business caused the stock prices of mortgage REITs to drop substantially.

I believe they dropped too much.

Now inflation has started easing up and the Federal Reserve has slowed its pace of interest rate hikes. The sentiment in the real estate market is improving as the mortgage rate decreases.

I expect these four commercial mortgage REITs in this article are worth an investor’s attention, especially if you’re in the market for higher yielding alternatives.

BrightSpire Capital, Inc. (BRSP)

BrightSpire Capital is a commercial real estate credit REIT that originates, acquires, finances, and manages a diversified portfolio consisting primarily of commercial real estate debt investments and net lease properties in the U.S.

Additionally, they originate mezzanine loans and preferred equity investments. BrightSpire has a large, diversified portfolio and executes a disciplined investment strategy to maximize shareholders’ returns.

Investor Relations

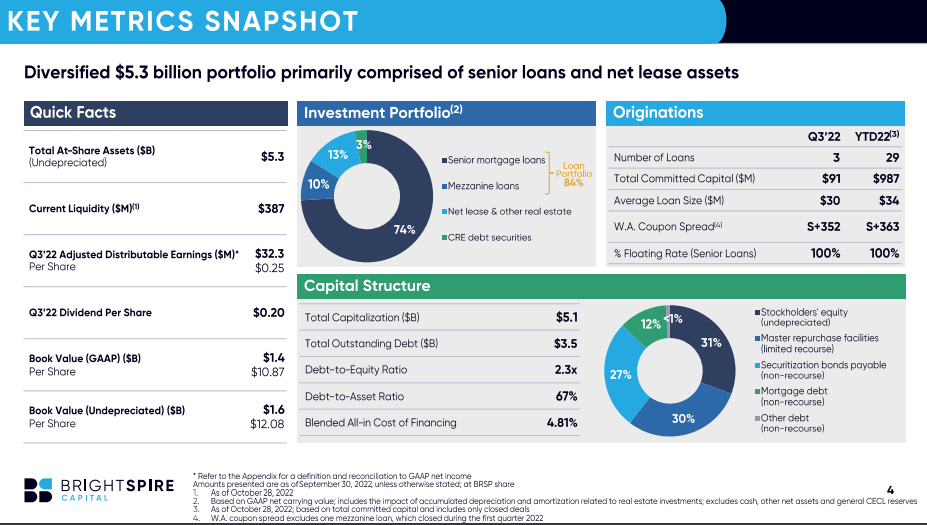

BrightSpire is doing a great job at managing risk and maintaining favorable capital structure. They have a very diversified portfolio that spread over multifamily, office, hotel, mixed-use, and industrials. Their debt-to-equity ratio is at 2.3x, and debt-to-asset ratio is at 67%. The blended cost of financing is at 4.81%. BrightSpire has $387 M of total liquidity available to them ($222 M of cash).

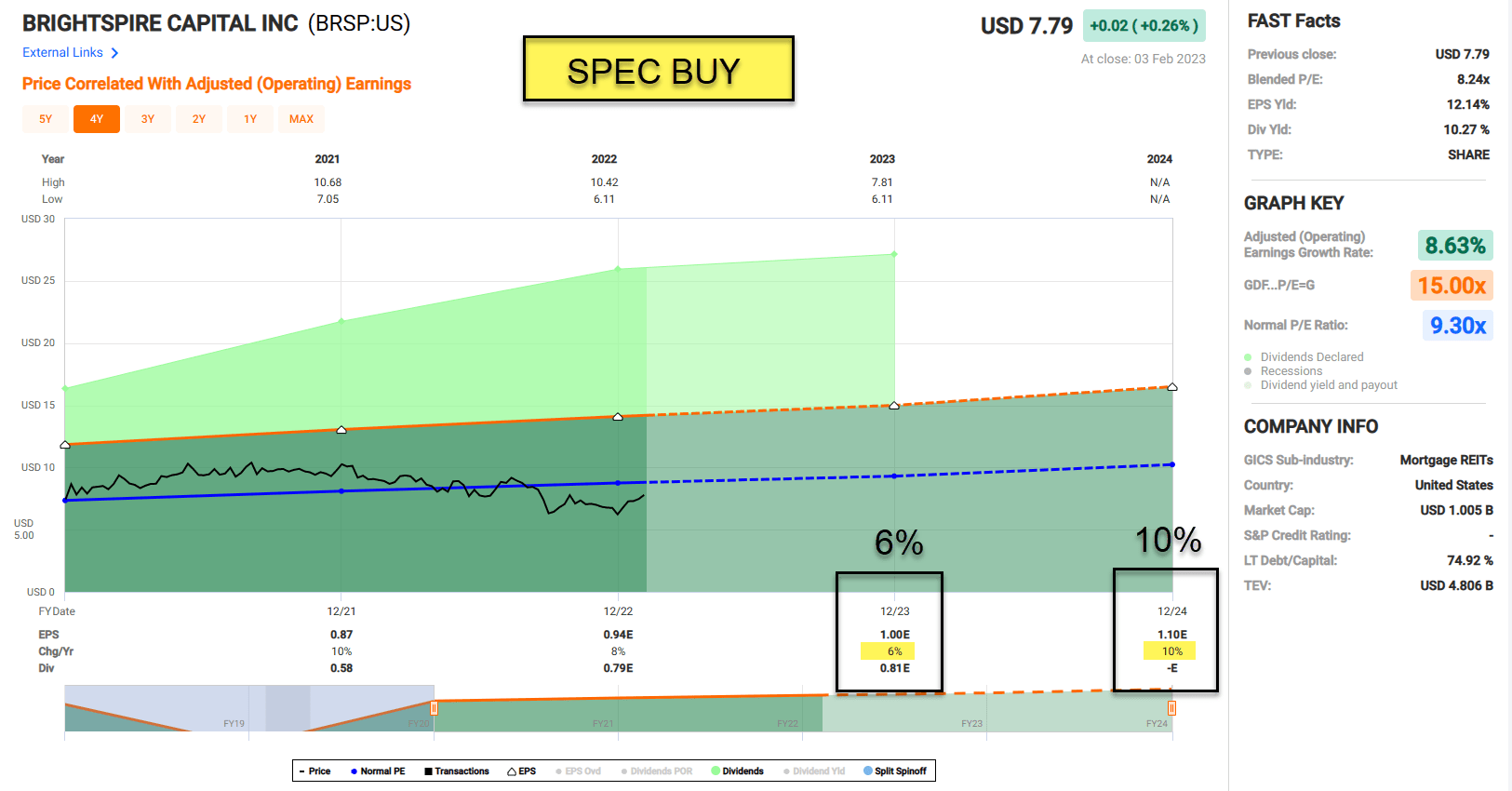

BrightSpire offers a very juicy dividend at this point with 10.27% dividend yield. Unfortunately, they stopped the dividend payment in the middle of the pandemic, but they resumed in 2021.

Given the cash dividend payout ratio of 68.03% and their solid capital structure, I expect BrightSpire to continue their dividend payment. Also, their strong operation will support their dividend as well.

FAST Graphs

TPG RE Finance Trust, Inc. (TRTX)

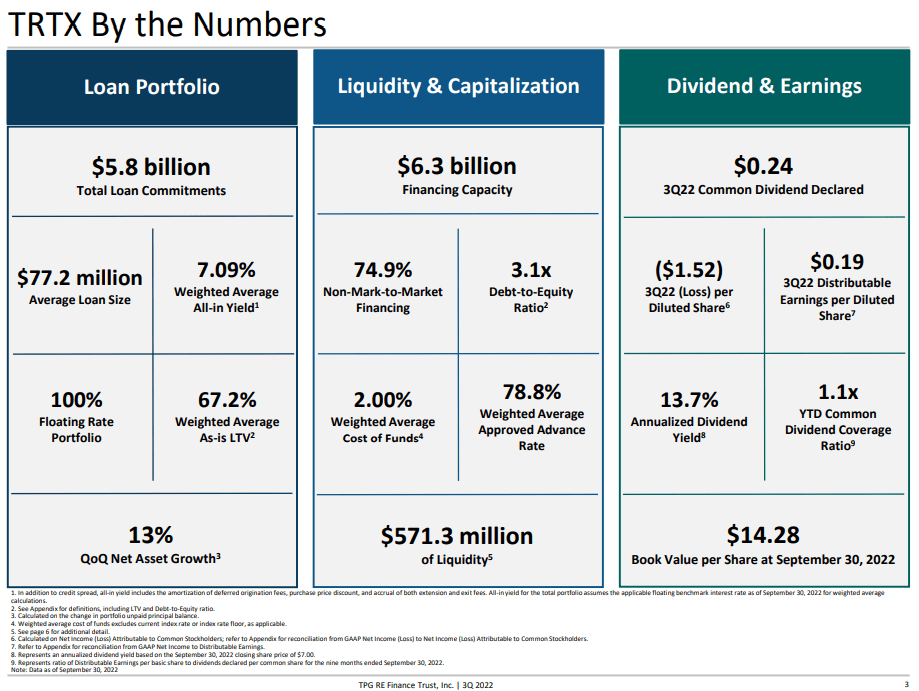

TPG RE Finance Trust is a commercial real estate finance company. Their principal activity is to directly originate and acquire a diversified portfolio of commercial real estate assets, consisting of first mortgage loans and senior participation interests. Their loan portfolio is worth $5.8 B with the weighted average all-in yield of 7.09%.

Investor Relations

TPG RE Finance has a strong liquidity position and solid balance sheet. They have over $6 B of financing capacity and $571 M of available liquidity to them. Their total leverage ratio is at 3.13x, and the debt-to-equity ratio is also at 3.13x. TPG satisfied their covenant terms at this point (minimum cash liquidity, debt-to-equity, tangible net worth, and interest coverage).

TPG RE Finance is currently paying a juicy dividend with 10.67% yield. Given their strong operation, solid balance sheet, and ample liquidity, I expect TPG RE Finance to continue paying their dividend. Their cash dividend payout ratio is at 71.2%.

FAST Graphs

Sachem Capital Corp. (SACH)

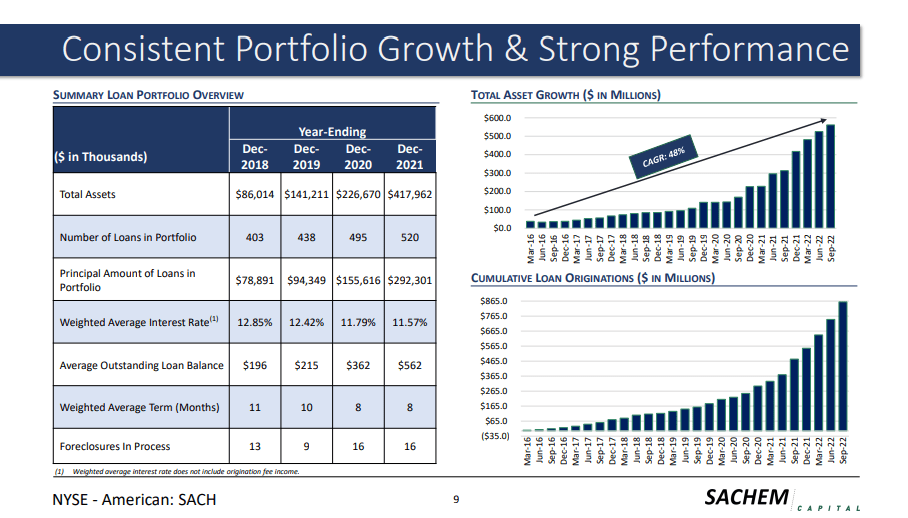

Sachem is a REIT that specializes in originating, underwriting, funding, servicing, and managing a portfolio of short-term loans secured by first mortgages liens on real estate properties. Their primary markets are the Northeast states and Florida. Their portfolio has been growing at a steady pace in the past several years. Sachem’s total assets grew at 48% CAGR since 2016.

Investor Relations

Sachem has a strong capital structure to support their growth strategy. They have ample liquidity available to them consisting of $35.5 M of cash, $200 M of master repurchase financing, and $150 M of available capacity remaining.

In an exclusive iREIT podcast near the end of the year, CIO and COO Bill Haydon discussed Sachem’s dividend decisions over the latter half of 2022. Sachem had consistently paid 12 cents per share quarterly, until a one-time summer payment of 14 cents.

Responding to shareholder’s frustration after Sachem dropped the dividend back to 13 cents, Haydon stated that Sachem had “picked up the inference that people wanted [the dividend] to be stable and increasing.”

At current prices, this makes for a quarterly payout with a very attractive 13.83% yield.

FAST Graphs

Starwood Property Trust, Inc. (STWD)

Starwood Property Trust is a REIT that originates, acquires, finances, and manage mortgage loans and other real estate investments in the U.S. Starwood has been growing steadily over the past couple of decades, and they acquired over $235 B of assets in the U.S. over the past 30 years. The portfolio of Starwood Property consists of multifamily (200,000 units), hotel keys (370,000), industrial (56 M sq ft), retail (56 M sq ft), and office (99 M sq ft).

Investor Relations

Starwood maintains a strong conservative balance sheet. Their debt-to-equity ratio is at 3.8x (including both off-balance and on-balance items), and their debt maturity schedule is very well spread over the next several years. Additionally, Starwood has strong financial capacity with $8.8 B liquidity.

Currently, Starwood’s dividend yield is at 8.93%. Given their conservative balance sheet and strong portfolio, I expect them to maintain the dividend level for the foreseeable future.

FAST Graphs

Risk…

Even though it is easing, recession fears are still strong on Wall Street and Main Street, and we may enter a recession later this year.

If a recession hits, the demand for mortgages in both the commercial and residential markets will decrease. Therefore, the performance of these mortgage REITs may suffer in the short term.

Even though the interest rate and mortgage rate are dropping, they are still at a higher level.

Also, listening to Jerome Powell’s speech, it seems like the Federal Reserve’s hawkish stance is still a factor. With a high borrowing cost environment, the real estate market will likely to stay bearish for the foreseeable future.

Conclusion

Inflation is finally showing a sustained downtrend, and it is good news for most people. I don’t get shocked by the high price tag on beef at the grocery store anymore. Mortgage rates have showed some slight downtrend, and the real estate sentiment is improving.

In the past several months, the mortgage REITs stock price suffered due to the lower demand and negative market sentiment. I expect a turnaround may get started soon, making this a point to consider some mortgage REITs. While you are waiting, you can collect a nice, juicy dividend.

Personally, I maintain around 10% of my overall REIT exposure in commercial mREITs and this has been a terrific blueprint for me because I can enhance my overall portfolio yield. Most Equity REITs generate yields of between 2% to 7%, with the average Equity REIT yielding 3.6%.

By combining vetted commercial mREITs and high-quality preferreds, with core equity REITs, my REIT portfolio generates high income and strong total returns. It’s a formula that I’ve back tested and is especially appealing for those living on a fixed income.

Remember that when dividend yields reach double-digit, the business models are much riskier, so it’s important to always maintain responsible diversification.

Always adopt an asset-allocation strategy that dovetails with your unique personal risk tolerances, and by doing so, you will vastly increase the odds of investment success.

Be the first to comment