sitox

This article was co-produced with Williams Equity Research (“WER”).

We’ve covered NewtekOne, Inc. (NASDAQ:NEWT) on here and in our Investing Group many times, and this article’s purpose isn’t to explain the entire backstory. Suffice it to say, NewtekOne Inc. went from an unknown C-corp to one of the best performing business development companies aka BDCs to an underperforming bank holding company.

To be fair, the company had its doubters when it transitioned to a BDC, and it took time for the market to appreciate the company’s unique business model. It wasn’t like other BDCs. And it outperformed almost every peer (all peers over certain timelines).

A similar story applies this time, but we don’t yet know the ending. NewtekOne stock climbed in price and recognition from modest levels around $10 back in 2015 to nearly $40 a share in May 2021. It touched $10 again during the 2020 crash, so the rapid rise to double pre-pandemic highs was extraordinary.

Not long after, management announced the acquisition of a ~60-year-old traditional bank and the planned conversion from a BDC to a bank holding company.

Investors can put up with almost anything, but not sustained uncertainty. Throw in a dividend cut more in line with banking peers, and it wasn’t a fun ride.

In this article, we aren’t concerned about the past beyond its usefulness for understanding the future. Stocks make irrational moves all the time. That’s one reason the stock market is so great – there is always a wonderful opportunity somewhere. The key is recognizing long-term value and holding it long enough to come to fruition.

Today, we take a no-nonsense view at NewtekOne’s Q1 2024 earnings report released on May 6th. We’ll analyze how management and the company have performed and use a mega-bank as reference for better context.

We’ll scrutinize full-year 2024 estimates and end with the answer to what this all boils down to: Is NewtekOne stock a misunderstood gem or a doomed business model?

The Business Strategy & Q4 Earnings

We are all busy and must find ways to earn a living. That doesn’t always leave a ton of time to study our investments. As a result of this and the natural tendency to look for shortcuts (e.g., technical analysis) in life, many investors know little about the companies they own. If that’s your situation, allocating more time to research or opting for an ETF occasionally isn’t a bad idea.

What you want to avoid is what I call “ETF-level knowledge” but own a portfolio of individual stocks. Knowing a few things about the sector outlook is great, yet not enough to responsibly manage individual stock positions. Bad information leads to bad decisions, and I see it happen every day. If investors don’t know the drivers of a company’s business, they are more inclined to panic sell at just the wrong time. Or believe a factor, like interest rates, has a different financial impact than it does.

This is an appropriate introduction to NewtekOne. Based on the comments I see on Seeking Alpha and elsewhere, many retail investors don’t have a strong grasp on what the company actually does. While I can’t cover everything here, I do expect readers to be in the “reasonably educated” camp after reading this piece.

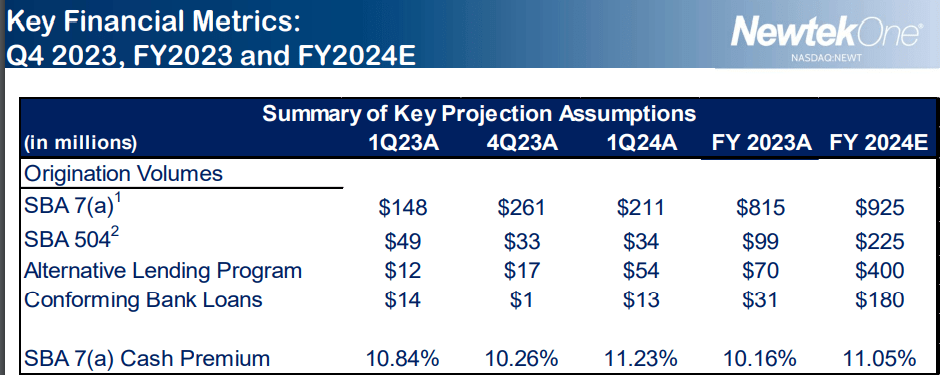

Newtek Q1 2024 Investor Presentation

NewtekOne primarily originates Small Business Administration (“SBA”) loans as shown above. Not home mortgages, not auto loans, not credit cards, and not consumer lending. That’s what most banks do, but it’s not what NewtekOne does (the bank division has some exposure to these more vanilla loan types and this is likely to continue). Additionally, NewtekOne has been reviewed by independent third parties as a stricter underwriter.

For example, Forbes stated that NewtekOne was a poor choice for a lender if your business is new, or you want an unsecured line of credit (riskier loans). Forbes reiterated that NewtekOne requires a longer operating history and loans against companies with meaningful assets and track records only (safer loans).

NewtekOne provides a range of lending solutions and business management solutions to small businesses. That’s what it did as a C-Corp all those years ago, why it was a moderately good fit as a BDC (lender to small and medium-sized private U.S. companies), and why it works today structured as a bank holding company.

Let’s continue with how NewtekOne compares and contrasts to the banking model we are all familiar with. This will help us better measure how NewtekOne is performing and understand its risks and potential strengths.

First, regular banks are a low-margin business. They generally earn a tiny spread on a large pool of capital. For that reason, they are sensitive to changes in their assets under management and interest rates. Banks must be cautious about the amount, or yield, paid to depositors. Pay a little too much on customer savings accounts or CDs and there won’t be any profit.

NewtekOne is also dependent on margins, but that’s where the similarities end.

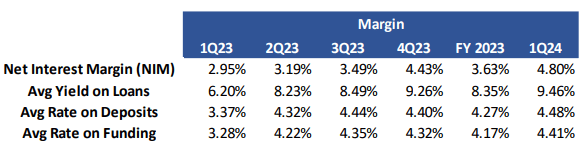

Newtek Q1 2024 Investor Presentation

Its average rate paid on deposits was 4.48% in Q1 2024 compared to an average rate on loans of 9.46%. That’s a net interest margin (“NIM”) of 4.80%. Look at the top row in the above chart. 4.80% is the strongest margin in any quarter. That’s far ahead of JPMorgan Chase’s (JPM) 3.48%. And unlike NewtekOne, JPMorgan’s peaked in Q4 2023. I’ll continue to use JPMorgan as a reference so you’ll know how the business models differ using real numbers.

NewtekOne isn’t just passing on higher rates, it’s increasing its margins to record levels. That’s because the increase in what NewtekOne has had to pay depositors is much less than the increase charged to borrowers.

If it sounds like NewtekOne has a more efficient business model than the average bank, you’d be right.

JPM Q1 2024 Earnings Presentation

JPMorgan is usually considered the best mega-bank in the U.S., if not the world. Its gigantic scale (half a trillion market cap) helped it achieve a 17% and 21% Return on Equity (“ROE”) and Return on Average Tangible Common Shareholders’ Equity (“ROTCE”), respectively, last quarter. These are two of the most used and important metrics for evaluating banks. If you include the acquisition of First Republic, the results are a disaster, but we will ignore those to make a fair comparison.

What about NewtekOne?

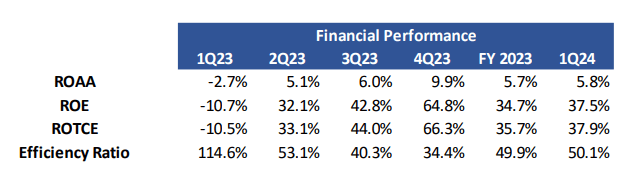

Newtek Q1 2024 Investor Presentation

NewtekOne produces almost double JPMorgan’s ROE and ROTCE. And consistently.

Sure, but NewtekOne’s business is way riskier than JPMorgan’s, right? There are a couple of ways to measure that. One is collateral. It’s true that many of JPMorgan’s loans are backed by assets, like homes, and NewtekOne’s are not backed in the same way. NewtekOne relies on personal guarantees from its borrowers (which means all their assets are collateral) and only loans to businesses with at least a few years of successful operating history. This makes it difficult to pin down exactly what collateral is behind the loans. One could argue it’s significantly greater than most other loan types, but I’ll only argue that it’s different and not necessarily better or worse.

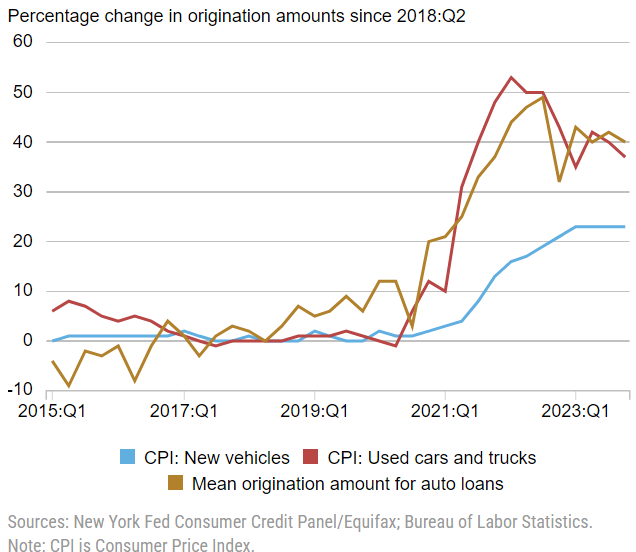

JPMorgan has $87.7 billion in auto loans and leases on its balance sheet. Based on the origination information and common sense, a large percentage were made in the past few years, when new and used car prices were in a bubble and underwriting standards were historically weak. We know exactly what the collateral is in this case, and it isn’t pretty.

New York Fed Consumer Credit Panel/Equifax

That’s not to mention $204.7 billion in credit card loans outstanding. These are large numbers, even for a bank with a market capitalization of $555 billion. I’m not claiming JPMorgan is less or riskier than NewtekOne, but rather proving that the answer to “what’s more risky?” depends on what matters to you. As someone intimately familiar with how SBA and auto loans work, I’d much rather own a pool of SBA loans today.

With NewtekOne, SBA loans require a personal guarantee from the owner. Not even a home mortgage requires that (at least not in the U.S.). SBA loans also undergo far more underwriting scrutiny than any other retail loan (e.g. auto/personal) except for a mortgage (we’ll exclude the NINJA home loans before the Great Recession).

But we don’t need to guess how risky one loan type is versus another. The data is there if you know where to look.

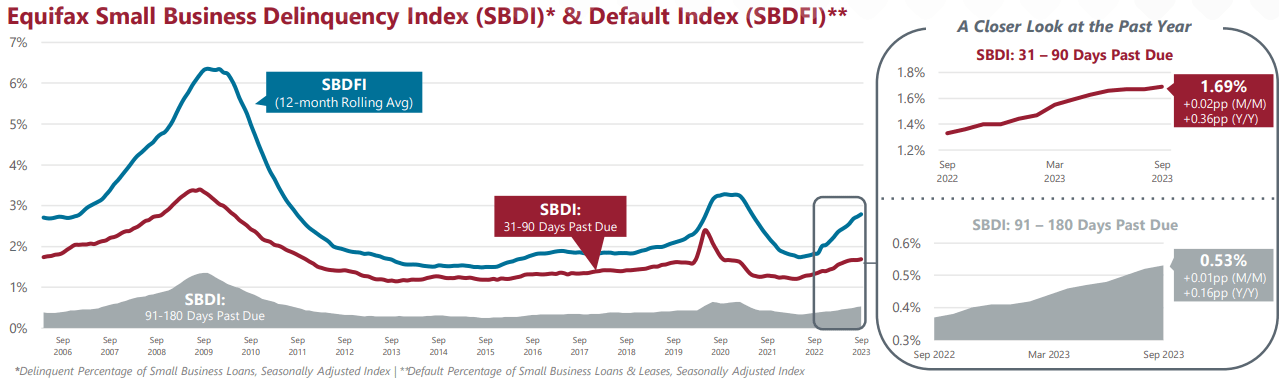

The SBA, for example, provides extremely detailed statistics about its loans. There is even a Small Business Lending Delinquency Index maintained by Equifax.

Equifax

The default rate for small business loans has been under 2.0% for years and ended last year around 1.7%. Guess what it is for auto loans?

New York Fed Consumer Credit Panel/Equifax

If default rate is your metric of choice, auto loans are currently defaulting at a rate 32% higher than small business loans. Delinquencies are higher than pre-pandemic levels for every income group, meaning that focusing on higher end clientele doesn’t guarantee insulation. Credit cards are in similarly poor shape. Those are both knocks on traditional banks. Home loans, however, are doing better and have a strong equity cushion behind them currently. That helps traditional banks.

The other common measures of portfolio risk for banks are capital ratios. JPMorgan’s Common Equity Tier 1 capital (“CET 1”) was 15.0% in Q1 2024. This is what the regulators use to gauge how much of an institution’s capital can absorb losses immediately when they occur. They consider this the highest quality of capital.

NewtekOne’s CET 1 was 17.6% during the same quarter, which is notably better than JPMorgan’s. There are many capital ratios we could discuss, but they all trend in the same direction.

One area where a mega-bank like JPMorgan has NewtekOne squarely beaten is its credit rating. JPMorgan can issue corporate debt at among the lowest expenses of any company thanks to its top tier Aa3/A+ Moody’s/S&P credit ratings. NewtekOne’s smaller size means an investment grade credit rating from a major issuer isn’t feasible. It has earned favorable ratings from lower tier issuers like Egan Jones in the past. It’s better than nothing, but it’s not a substitute.

Fortunately, since it’s now a bank, NewtekOne can issue CDs and savings deposits for collateral. It couldn’t do that before, and it’s a major reason that NewtekOne purchased a bank.

The company was paying a much higher cost of capital before the conversion. Interestingly, ~95% of NewtekOne’s CD’s come with a 6-month term. This is important to consider because it gives the company a lot of flexibility. If NewtekOne had to resort to issuing highly attractive CDs with two- or three-year terms, it could be in trouble if rates were to decline rapidly. That doesn’t appear to be a risk right now, but it’s better to hedge against it anyway. This helps NewtekOne achieve one of the lowest liability durations that I’ve come across. On the other hand, NewtekOne will have to keep attracting new deposits to maintain its momentum. Scott Price, NewtekOne CFO, stated in the May 7th conference call that their retention on maturing CDs has been “above industry standards at 90%.”

NewtekOne’s sequential (this means quarter-over-quarter instead of year-over-year) deposit growth was approximately 9% in Q1 for the bank division. Across the firm, it was 11%. Those are solid annualized numbers, and NewtekOne achieved it sequentially. For comparison, U.S. bank average deposit growth was approximately 2% over the same period.

To finish this section off, let’s talk about loan losses. NewtekOne’s provision for credit losses (“PCLs”) were $4.0 million in Q4, which is up moderately compared to Q3 2023’s $3.5 million but down relative to Q4 2023’s $4.4 million. These are sizeable relative to earnings before taxes of $9.3 million for the quarter (note that PCLs are subtracted to reach this figure).

In general, problematic loans have increased slightly as a percentage of the portfolio in recent quarters, in line with what’s happening in the broader economy. The $37 million in problematic loans still at the non-bank lender within NewtekOne is a real number. It’s unclear how many of these loans will end up re-performing, but the unrealized losses were already booked in previous quarters.

At the bank level, there are approximately $12 million in loans past due between 31 and 89 days. It’s important to remember that NewtekOne sells the government guaranteed tranche. While the $12 million is ~3% of the current pool, it’s roughly between 1% and 2% of the original amount. This is right in line with the SBA figures we analyzed previously.

Cash Flow & Dividends

NewtekOne increased its dividend by 5.6% to $0.19 quarterly per share after releasing Q4 2023’s earnings. The forward annual yield was 7.5% at that time. While a nice bump, it’s in a different ballpark than the peak of $0.70 quarterly per share achieved while still a BDC.

Those numbers require explanation to see the real picture. As a BDC, NewtekOne often paid out around 100% of its cash earnings as dividends. That’s normal for a BDC.

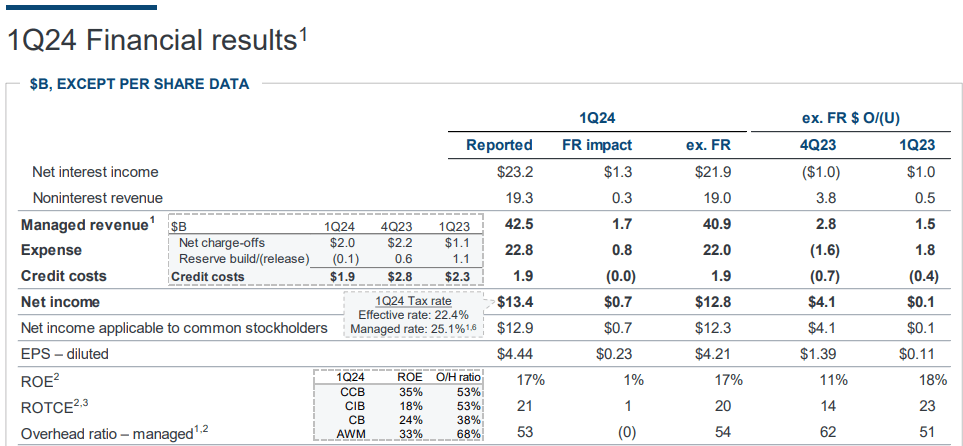

As a bank, however, that $0.19 is a 50% payout ratio against core earnings per share of $0.38 in Q1. Management is targeting $1.85-$2.05 in core earnings for the year, so that would keep the payout ratio right at 50%. As a side note, that was previously $1.80-$2.00, but management increased it in the May 7th conference call. While the dividend is down massively, cash flow per share is similar to pre-bank conversion, depending on how it’s calculated and exactly what period is used.

I do not anticipate rapid dividend growth for NewtekOne given reinvestment into the business is critical and a major driver of the conversion in the first place. I do, however, expect at least mid-single digit increases annually.

Valuation & Conclusion

NewtekOne was trading around $11 per share before May 6th’s earnings release. It rose $1.25 on the news and is now around $12.33 per share. Using midpoint core earnings of $1.95 (and management has hit its key earnings numbers consistently over time), that’s a 6.3x earnings multiple.

Western Alliance Bancorporation (WAL) is a regional bank that almost failed during last year’s crisis. Every regional bank worse than it was bailed out or taken over. It trades at 8.15x. The SPDR S&P Regional Banking ETF (KRE) traded with a P/E ratio of 10.9x as of March 31st. KRE is up slightly over that period, so it’s above 11x now.

The Invesco S&P SmallCap Financials ETF (PSCF) had a P/E ratio of 13.4x as of the same date. Frankly, it doesn’t matter what you compare NewtekOne to. Low quality regional banks, small-cap financial stocks, or just companies with a similar financial profile and trajectory. It’s undervalued. If management delivers on 2024’s targets, I think a 10x P/E should be the floor. That’s $19-$20 per share using today’s figures and assumes no growth outlook for 2025.

If NewtekOne can reach most of its stated AUM and strategy goals over the next 2–3 years, a 12-13x multiple makes sense to me. Add in 5-10% earnings growth each year, and that’s $28.17 at the end of three years, using the midpoint of all the ranges discussed. That’s 129% capital gains plus $2.28 in dividends, or a 147% total return over the 3-year period. That may seem like a long shot, but it’s still well under what NEWT was trading at in 2021.

Be the first to comment