Dilok Klaisataporn

New Pacific Metals (NYSE:NEWP) reported Bolivia’s largest silver discovery in the last 30 years. Besides, the company recently compared one of its exploration projects with another project valued at more than $1.28 billion. Currently trading with a valuation of around $400 million, a new feasibility study to be reported in 2022, and information about the drilling in the Carangas project could send the stock price higher. With that, let’s note that the stock is not for everybody because inflation risks and failed assessment of reserves could bring stock price volatility.

New Pacific Metals

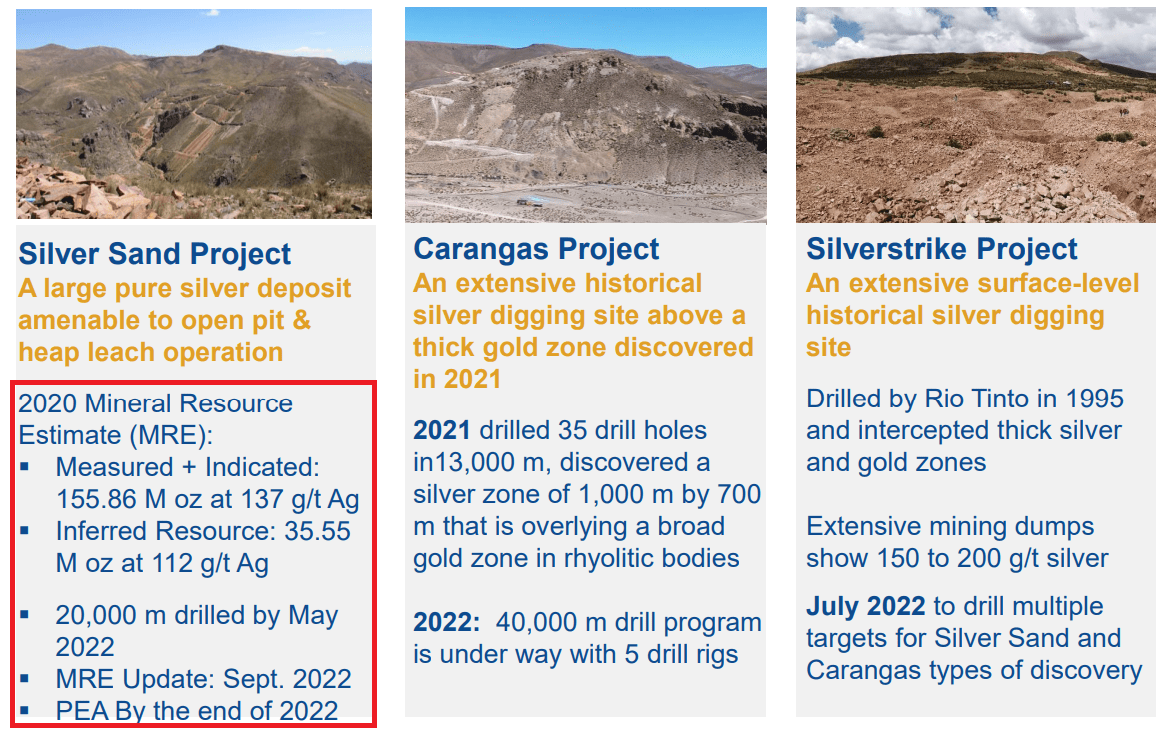

Incorporated in Canada, New Pacific Metals runs the Silver Sand Project, which is said to be Bolivia’s largest silver discovery in the last 30 years. The company also has two exploratory projects, Carangas and Silverstrike.

I believe that investors are expecting quite optimistic outcomes from the feasibility studies to be reported about the Silver Sand Project. However, in my view, they may also bet on the optimistic results from the drilling projects of Carangas and Silverstrike. Let’s keep in mind that management compared the Carangas project with the Filo Del Sol project, which reports an after tax net present value of $1.28 billion. These figures may explain why the current market capitalization stands at much more than the valuation of Silver Sand Project.

Company’s Website

With that about the projects run by New Pacific Metals, I believe that 2022 and 2023 could be quite exciting in terms of stock price catalysts. Management is about to release the Silver Sand Preliminary Economic Assessment along with reports about new environmental permits activities and new updates in September. I believe that new information about the production plans could push the stock price up.

Company’s Website

Finally, let’s note that the company is present on social media, where many new posts about the PEA and the Bolivia government’s 2021 to 2025 economic development plans were released.

Right now we are in the process of doing a PEA and it’s going to be finished by the end of this year, also in parallel we’re trying to do a PFS to take advantage of the Bolivia government’s 2021 to 2025 economic development plan. Source: New Pacific Metals – Twitter

Under Normal Circumstances, The Valuation Of The Silver Sand Project Does Not Exceed $100 Million

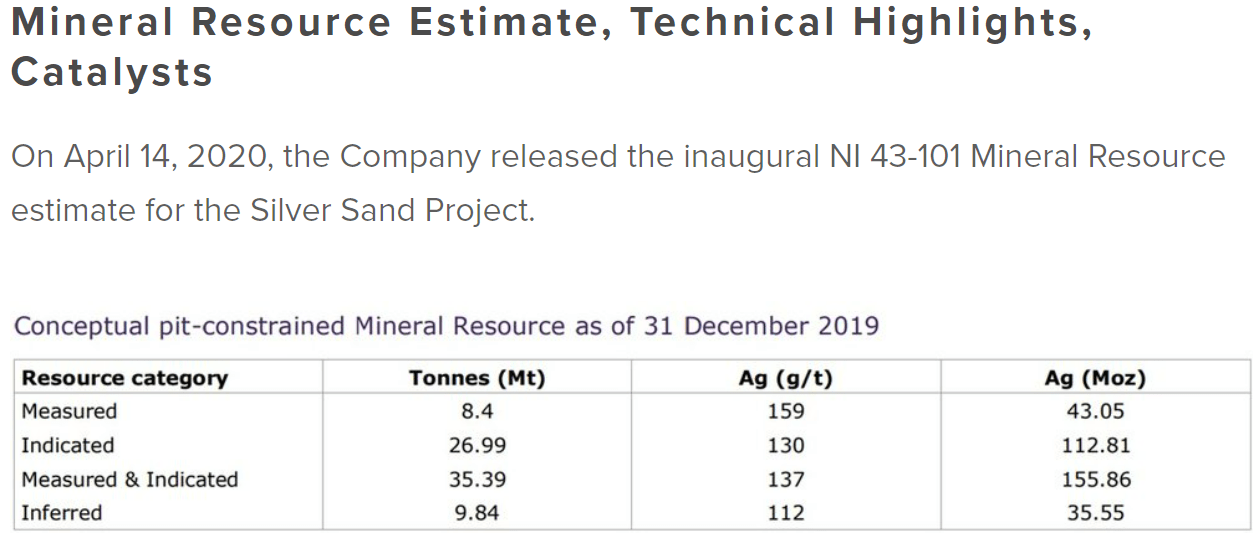

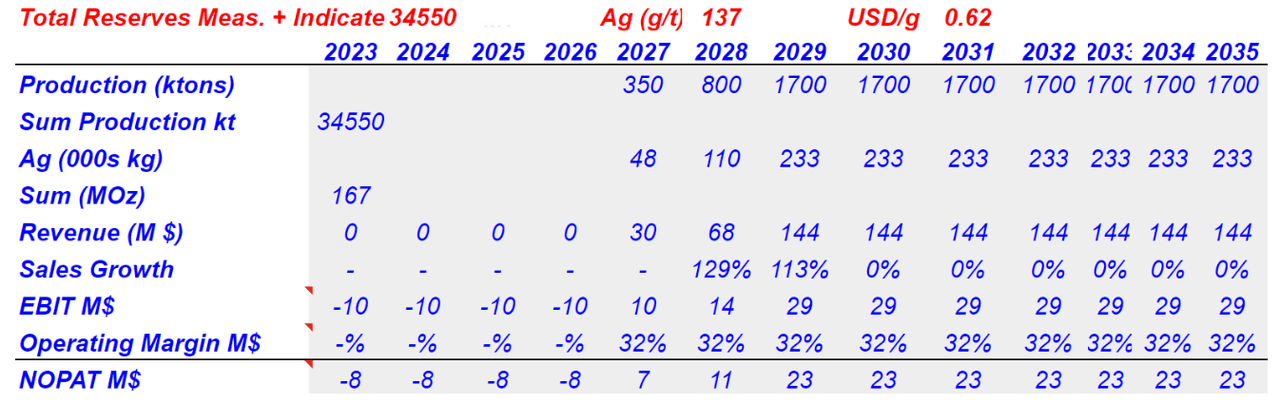

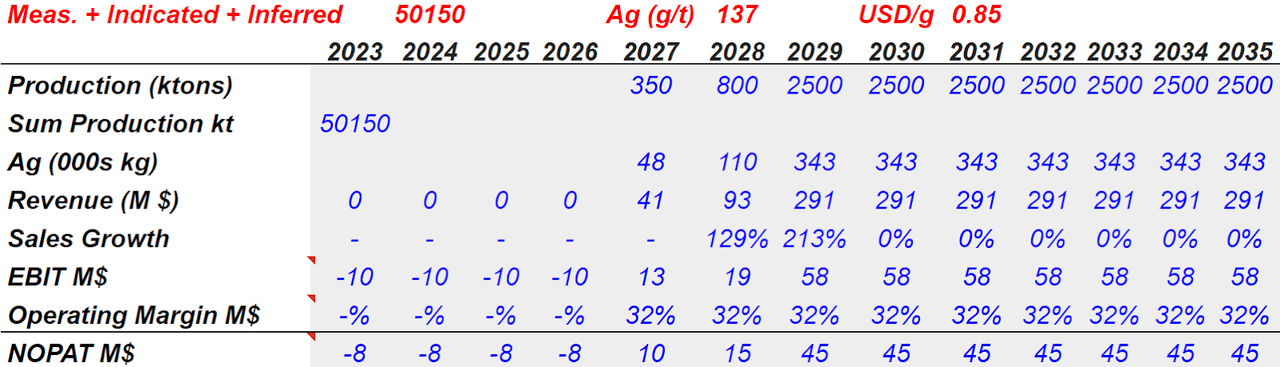

For the assessment of the Silver Sand Project, I assumed close to 35 million tons of mineral resources including 8.4 million measured tons and 26.99 million indicated tons of mineral resources. I also used 137 grams of silver per ton. These figures were reported by New Pacific Metals in a technical report:

Company’s Website

Company’s Website

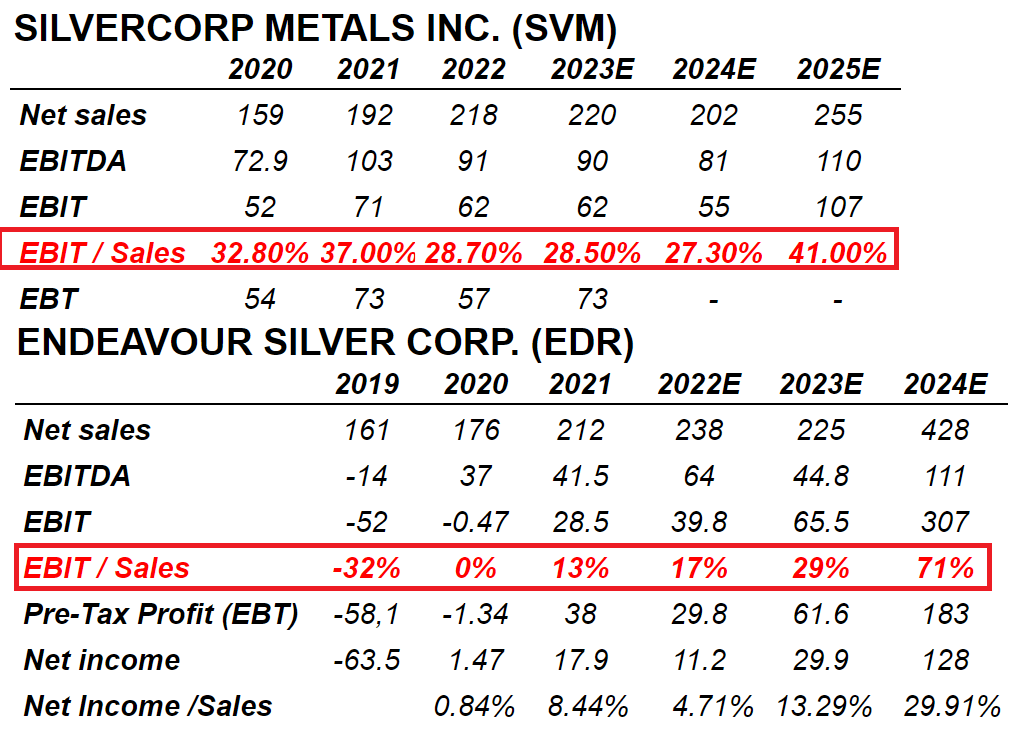

I also used EBIT/Sales figures from other miners of silver. Silvercorp (SVM) and Endeavor (EDR) report EBIT/Sales between 37% and 17%. My assumption includes an operating margin close to 32%:

MarketScreener

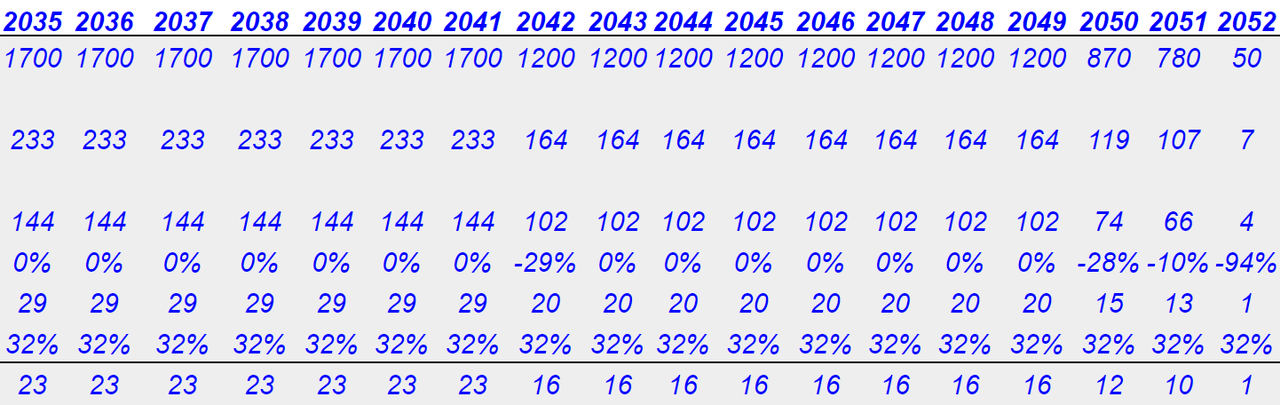

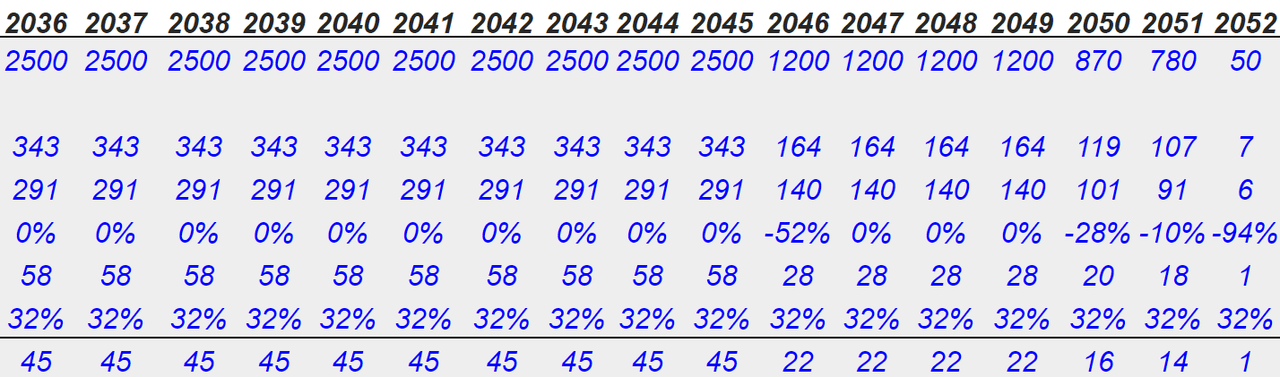

I assumed total production of close to 35 million tons, 137 grams per ton of silver, and $62 per gram. I believe that the company could produce 1700 kt per year from 2029 and 1200 kt from 2042 to 2049. With an operating margin around 32%, the non-operating profit after tax would stand at close to $23 million per year from 2029 to 2041 and $16 million from 2042 to 2049.

Author’s Work

Author’s Work

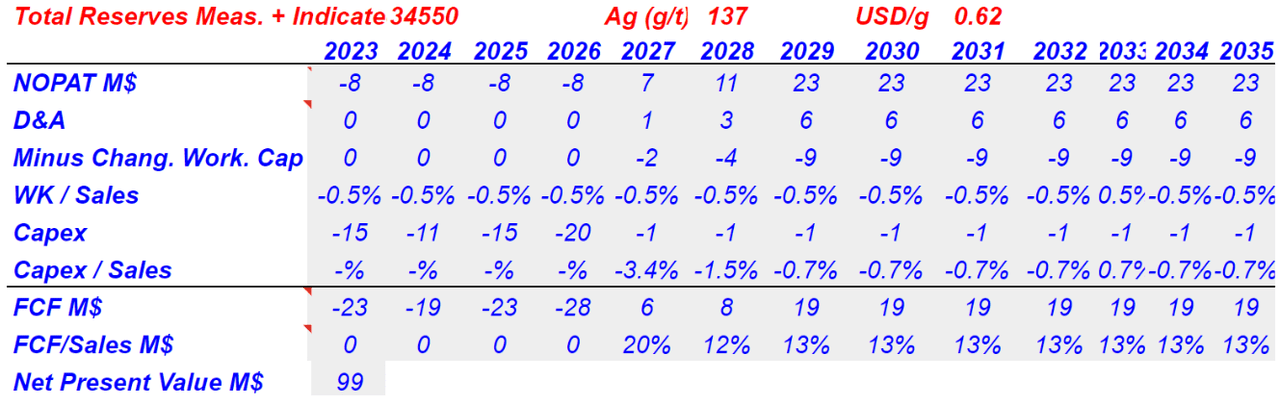

Now, with growing D&A, changes in working capital/sales around 0.5%, and optimistic capex/sales, I obtained a maximum free cash flow of $19 million per year. The NPV would stand at close to $100 million.

Author’s Work

Author’s Work

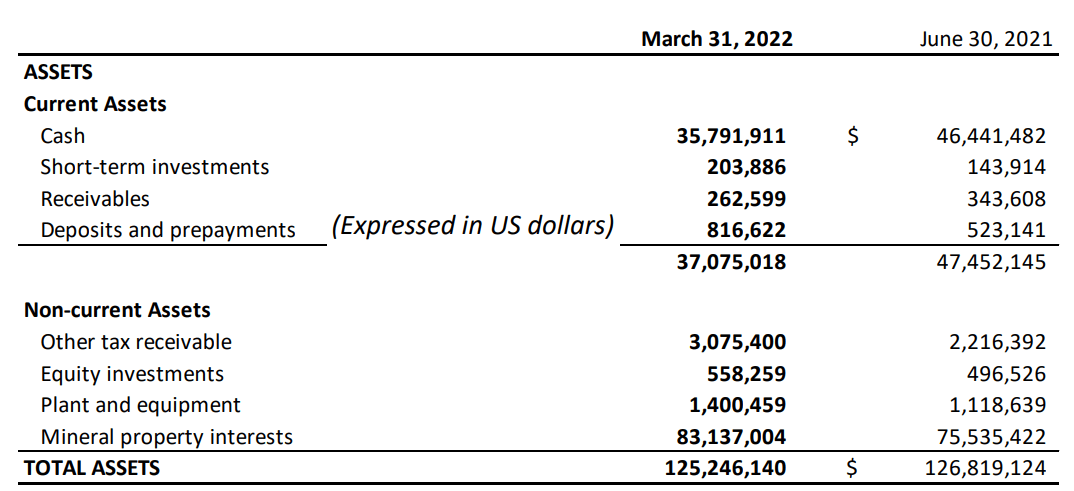

I believe that the valuation of the mine done by management is clearly aligned with the assumptions made in this case scenario. As of March 31, 2022, mineral property interests were worth $83 million. With that, I believe that there is room for optimism because the mineral properties increased from $75 million in June 2021 to $83 in March 2022. In my view, as management continues to explore and drill new areas, proven reserves will likely trend higher. As a result, future production and future free cash flow may trend higher too.

Quarterly Financial Statements

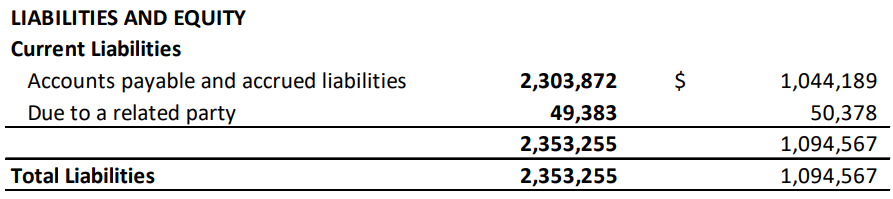

It is also beneficial that the company does not have financial debt, and has $35 million in cash. It means that New Pacific Metals can receive debt financing if management believes it is necessary. Keep in mind that the asset/liability ratio stands at more than 50x.

Quarterly Financial Statements

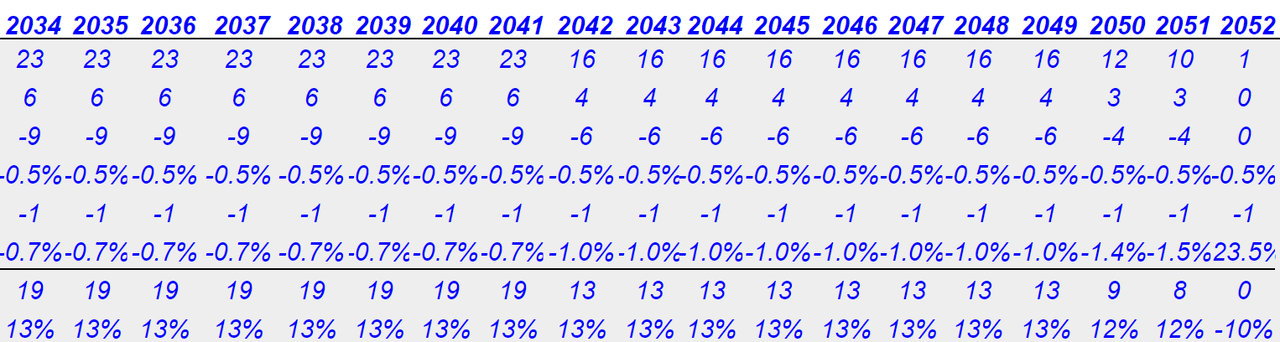

A More Optimistic Scenario Results In A Valuation Of Silver Sand Project Of $332.5 million, And Traders May Be Betting On The Carangas Project

If you are an optimistic investor, you will most likely appreciate this case scenario more than the previous one. Considering the increase in mineral properties reported in the last balance sheet, I assumed that more exploration will lead to more proven reserves. Let’s not forget that I am assuming that New Pacific Metals will produce until 2052. Clearly, management has a lot of time to conduct further exploration and development.

I assumed reserves of 50 million tons, production close to 2.5 million tons, and revenue close to $300 million. The results include 2030 NOPAT of $45 million and operating margin around 32%.

Author’s Work

Author’s Work

Under my best case scenario, future free cash flow would even reach almost $45 million from 2030 to 2045, and the FCF/Sales ratio would stand at 15%. The net present value with a discount of 5% would stand at $332.5 million.

Author’s Work

New Pacific Metals currently trades with a valuation of more than $400 million. It means that many market participants believe that both the Carangas project and Silverstrike project are promising. I couldn’t find a lot of information about expected proven reserves. Management will most likely have to invest much more money to measure the reserves in these new areas. With that, the information that we have so far is promising.

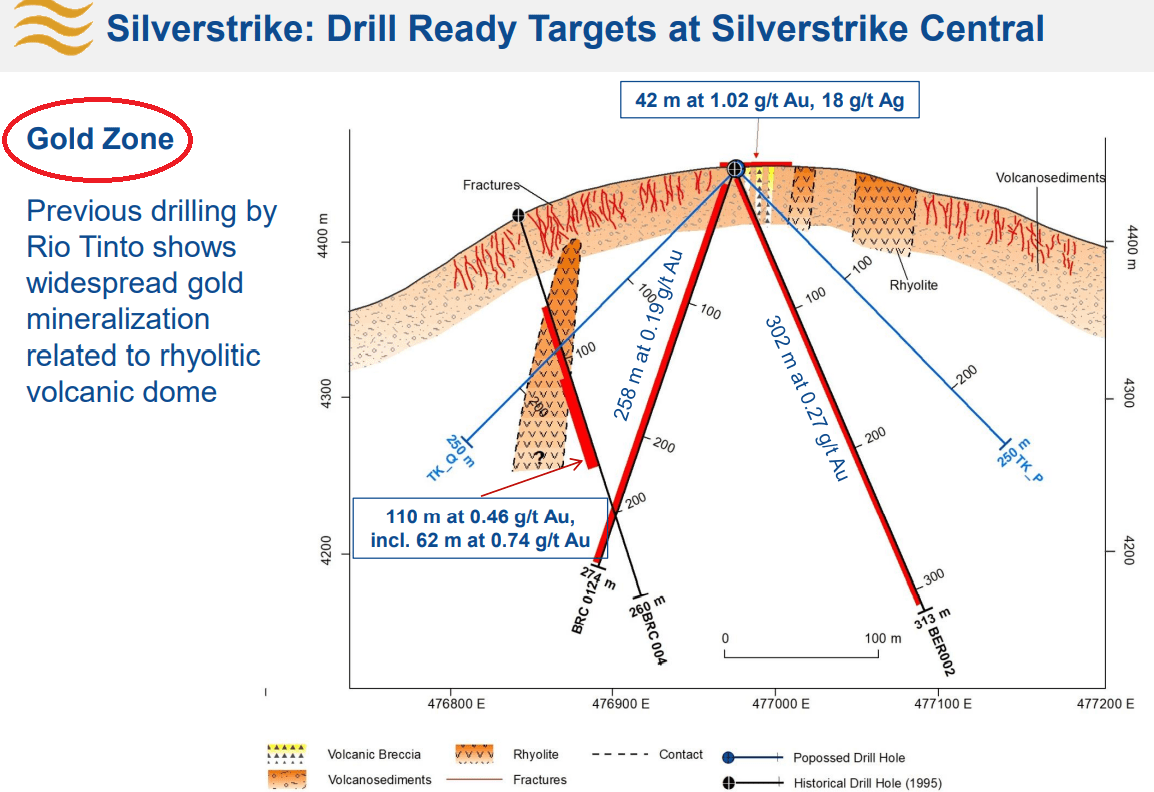

The Silverstrike project includes a gold zone. Previous drilling conducted by Rio Tinto (OTCPK:RTPPF) includes gold mineralization with concentration close to 1.02 grams per ton of gold and 18 grams per ton of silver. Management only needs to assess the total valuation of these gold and silver mineralizations.

July Presentation

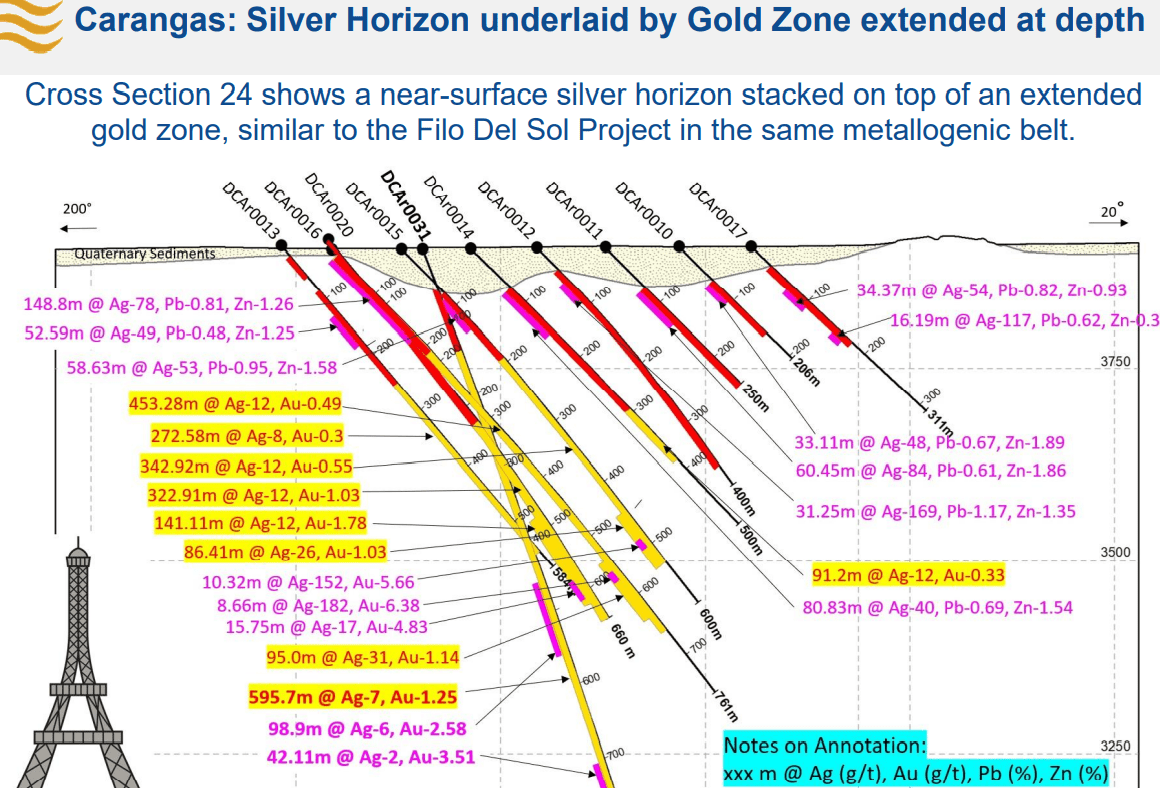

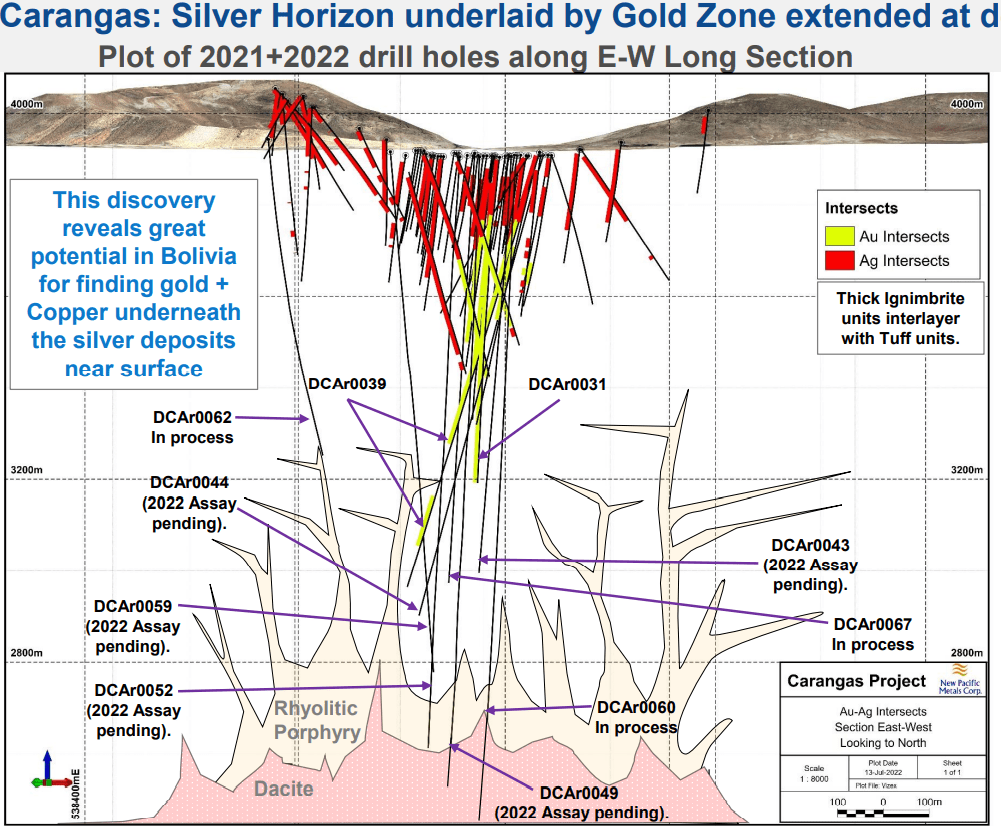

With respect to the Carangas project, the company disclosed mineralization with 78 g/t of silver and 1.26% of Zinc. The project was compared by management with Filo Del Sol project, which was reported to have an after-tax net present value of $1.28 billion. Filo Del Sol project is located in the same metallogenic belt.

July Presentation

July Presentation

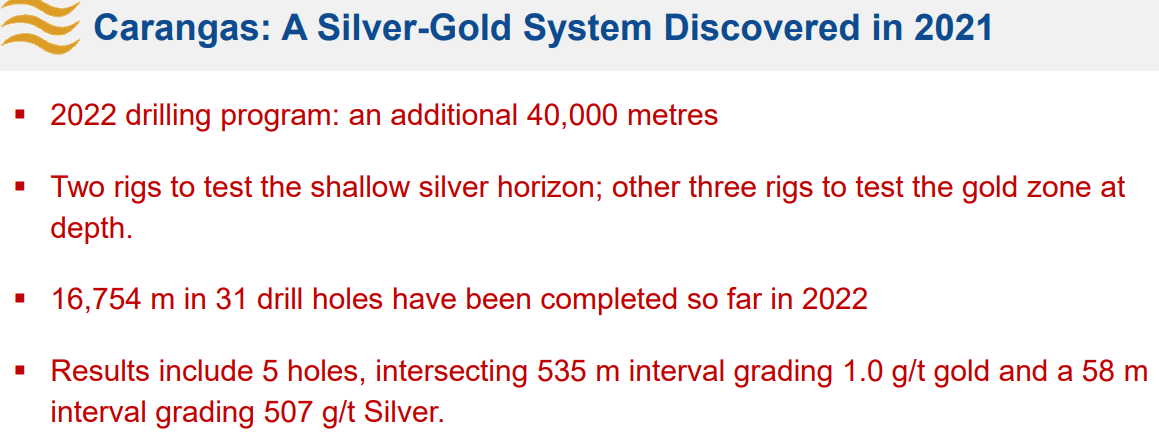

In my view, we will soon have much more information about the mineral reserves in the Carangas project. Keep in mind that the company announced a drilling program with more than 40k meters to be conducted in 2022.

July Presentation

New Pacific Metals currently trades at less than $500 million. I don’t believe that the Silver Sand Project could justify such a valuation with the information we have. In my view, the upside potential is quite significant because of the Carangas project. In sum, the stock is not for very conservative investors, but could be very profitable for some others.

If the Silver Sand Project is finally worth $332.5 million, with $35 million in cash, we would obtain a valuation of $367.5 million. If we assume that the Carangas project is worth 25% of NPV of the Filo Del Sol project, we could give an estimate of around $725 million. The sum of these projects could stand at more than 1 billion dollars. If we assume 150 million shares outstanding, the implied price would be $6.6 per share.

Risks From Failed Estimation Of Reserves, Inflation, Or Supply Chain Could Push The Stock Price Down

New Pacific Metals and I made a significant number of assumptions with regards to the total life of the company’s flagship project. The company will reveal a lot of new information about the economic feasibility of the projects and perhaps new mineralization figures. If the numbers are lower than expected by the market, the stock price would likely decline. Finally, the company may also produce less mineral than expected because geological models may be too optimistic. As a result, the company’s fair valuation would be lower than expected.

An increase in inflation could also be very detrimental for New Pacific Metals. Salaries could increase, capital expenditures may be higher than expected, or opex could exceed expectations. As a result, future free cash flow could be lower than what I expected. In the worst case scenario, we would expect a decline in the company’s valuation.

Under certain circumstances, New Pacific Metals may face supply chain complications. Management needs certain machinery and tools for drilling, exploring, and mining. If the company cannot have these tools, or has to pay too much for future free cash flow, margins would decline, which would lead to a decrease in the company’s stock valuation.

Conclusion

The valuation of New Pacific Metals reached more than $400 million, which is significantly more money than the net present value of Silver Sand Project. I believe that the mineralization found in the Carangas project and the association with the Filo Del Sol project generated significant optimism in the market. In the same metallogenic belt where the Carangas project is located, Filo Del Sol project is said to have a net present value of more than $1.28 billion. With this in mind, I believe that the Carangas project could be worth enough to justify the current market valuation of New Pacific Metals, and perhaps much more.

Be the first to comment