designer491

Written by Nick Ackerman, co-produced by Stanford Chemist.

BlackRock 2037 Municipal Target Term Trust (NYSE:BMN) launched near the end of 2022. That put it in a situation where it didn’t ride the municipal bond market slide down like its older peers, which came about due to rapidly rising Treasury Rates.

Though that did mean we still saw BMN slide like the rest of the space in October 2023, when rates once again rose higher. Meaning it is definitely not immune to declines; it just launched at a time that was more favorable for the fund and what they were looking to invest in. That’s why its NAV is now higher than at its inception.

BMN Performance Since Prior Update (Seeking Alpha)

The NAV per share is particularly noteworthy because the fund is a target term. We discussed more of the finer details of the fund in our original coverage of the fund. That said, with a target term fund, they look to return NAV back to shareholders at its liquidation. We have until 2037 for this one, so that isn’t really a worry at this time.

BMN Basics

- 1-Year Z-score: -1.20

- Discount: -8.31%

- Distribution Yield: 4.72%

- Expense Ratio: 0.72%

- Leverage: 7.22%

- Managed Assets: $172 million

- Structure: Target Term (attempts to return original $25 NAV back to investors with an anticipated liquidation date of September 30, 2037)

BMN’s investment objective is to “provide current income that is exempt from regular federal income tax.” To achieve this, the fund will invest “at least 80% of its managed assets in municipal securities. The Trust will invest primarily in investment grade quality securities.” To facilitate a better chance to return the original NAV back to shareholders, the fund will also “actively manage the maturity of its securities, which are expected to have a dollar-weighted average effective maturity approximately equal to the Trust’s maturity date.”

Despite being a BlackRock fund, it seems that they weren’t able to garner too much in terms of assets when launching this fund. This isn’t that unusual though in a time when the market was in bear market territory.

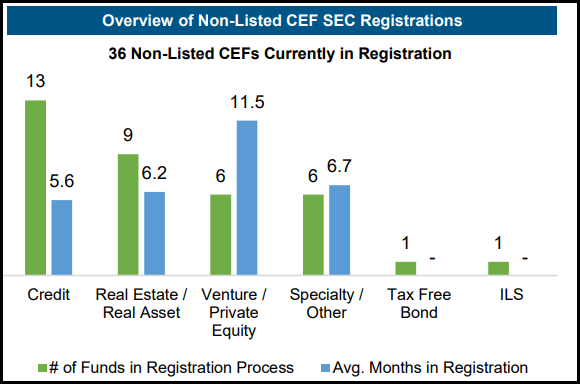

In fact, there haven’t been too many public closed-end fund launches in the last couple of years now. Besides poor market conditions in 2022, fund sponsors have seemingly been favoring non-traded interval and tender offer fund launches instead.

Non-Listed CEF Registrations (XAInvestments)

According to XAInvestment, there are 36 non-listed CEFs in the registration process right now, with only 5 public CEFs in the pipeline. 2 of those 5 potential public CEFs had an initial filing back in 2021, with another 2 originally filing in 2022. One of these funds in the pipeline is the BlackRock 2038 Municipal Target Term Trust, a sister fund to BMN.

With all that being said, BMN is quite a small fund and that can limit liquidity in terms of having relatively lower daily trading volume.

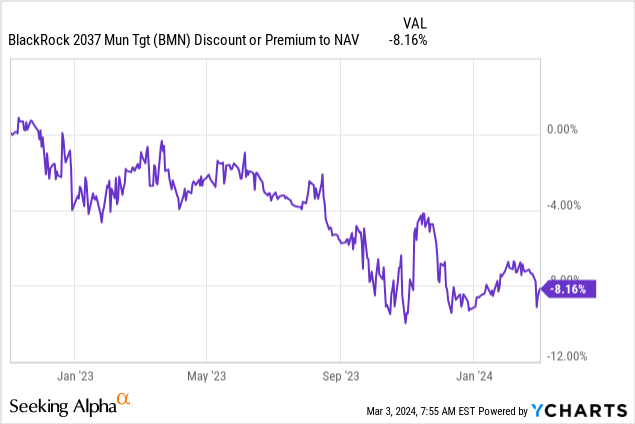

Performance – Attractive Discount Opens Up

As we noted, the fund has had the advantage of launching at an advantageous time relative to its longer-running muni peers. They didn’t see the drawdown throughout 2022 when rates were rising, and the Fed was raising rates aggressively. That said, it hasn’t escaped slipping to a discount. This often happens with new closed-end funds, whether they are perpetual, term or target term funds. Therefore, this isn’t really out of the ordinary or shocking at all.

Ycharts

This is precisely why CEFs can be interesting and possibly lucrative investment wrappers, though. It is due to this discount/premium mechanic that can be exploited.

Municipal bond CEFs, in general, are trading at the widest relative discounts compared to equity and taxable counterparts. RiverNorth’s data reflects that discounts in the muni CEF space have only been wider 3% of the time since 1996. The average discount for muni CEFs as of the end of February came to ~11%. That makes BMN less appealing on that front, on an absolute basis, but that’s not the only factor to consider either.

An additional factor with BMN is that the fund allows for utilizing leverage, but it didn’t do so right away. Instead, they’ve now been slowly adding leverage to the fund, with their last annual report now reflecting the addition of tender option bonds.

That said, the effective leverage comes to only 7.22%. This also only appeared in Q4 2023, as their Q3 commentary noted that as of September 30, 2023, the fund has “not yet deployed leverage.” Though it was also broadcasted at that time, that leverage was soon to come.

We continue to remain patient with employing leverage. Given increased funding levels and long term yields we believe patience may pay off and we may look to begin employing leverage in the later part of the year.

Taking their time to add leverage at a more advantageous time seems prudent. They noted that they will utilize leverage “in an amount up to 33.3% of managed assets.” Besides leverage through the TOB Trust, they also leave the door open for the issuance of preferred shares. Even further, they noted that they don’t have intentions of utilizing a credit facility through a financial institution; they may do so in the future. That’s mostly kept the door open for the fund to remain highly flexible in how they choose to leverage up.

Now does seem to be the ideal time to pick up some long-duration assets, such as additional exposure to munis. Most expect that we are at peak rates from the Fed for this cycle. It’s why I’ve been looking more at municipal bonds myself lately, covering a number of muni CEFs more regularly. Lower rates should bode well for municipal bonds and, therefore, muni CEFs; yields are also looking quite attractive as yields rise and, thanks to the tax-free nature providing higher taxable equivalent yields.

A main risk, though, is that inflation could trend higher and throw a curveball for all of us, but only time will tell. BlackRock also isn’t the only one looking to buy some muni exposure either, as Saba Capital Management has been targeting a number of funds.

So where we ultimately end up is all up to inflation and its impact on rates; still, muni CEFs look more attractive now than they did 1 and 2 years ago.

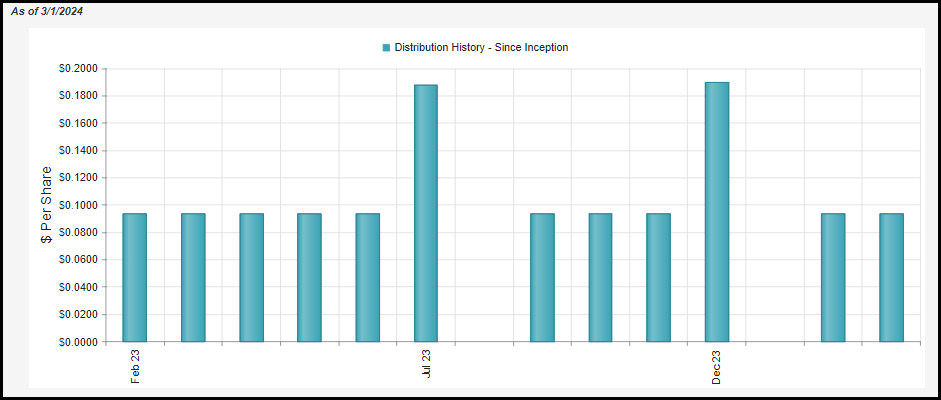

Distribution – Tax-Free Income

Another factor to consider when the fund launched and did not experience the greater volatility that came with higher rates on borrowings of the fund was the distribution. Since BMN’s launch, they’ve been able to maintain the same monthly distribution.

BMN Distribution History (CEFConnect)

Most leveraged muni funds had to slash their distribution many times over the last couple of years as their borrowing costs increased substantially, in most cases leveraged muni funds are now paying more for leverage than they earn on the underlying munis they hold.

A number of those funds that slashed their distributions have increased their payouts more recently, but it was only in an effort to reduce discounts or with an optimistic outlook that rates would be coming down before too long. Either way, the leveraged funds that have increased their distributions in a reversal from the prior cuts have only seen their distribution coverage decline.

BMN isn’t immune to future interest rate swings anymore now that they are leveraging up with the tender option bond trust. That said, the average rate for TOB trusts came to 3.37% as of their last report, with a peak rate of 4.05%.

BMN TOB Trust (BlackRock)

BMN’s lists the average coupon of their portfolio comes to 4.97%, which would mean a positive spread, but then you have to factor in the operating expenses of the fund. That puts another ~0.75% on top of their TOB costs, and the positive spread narrows meaningfully. Of course, that’s still much better than the 5 to 6% rates we are seeing funds pay through their credit facility, plus the operating expenses for those funds as well.

This last report also shows that the fund’s net investment income coverage came to around 93%. Ideally, we want to see a fixed-income fund have coverage of greater than 100%, but it isn’t necessarily the worst coverage we’ve seen. At the same time, with NAV increasing since the fund’s launch, it has been able to ‘cover’ the distribution by realized/unrealized appreciation.

BMN Annual Report (BlackRock)

The fund’s distribution rate comes to 4.72%, which may not seem too enticing for high-yield-focused investors. However, the taxable equivalent yield for someone in the 24% tax bracket starts to push that rate up to 6.21% – which starts to become more competitive. Thanks to the discount of the fund, the NAV rate comes to a lower 4.33% level.

For tax purposes, the fund has distributed mostly tax-free income to investors. Though, as is usually the case with CEFs that hold a diversified basket of holdings, there has been a small portion that’s subject to ordinary income rates.

BMN Distribution Tax Classification (BlackRock)

BMN’s Portfolio

At the end of 2023, the fund listed 97 holdings in total. The fund also listed that 18.05% of the bonds held in the portfolio are subject to the alternative minimum tax or AMT.

The effective duration of the portfolio at the end of January 31, 2024, was listed at exactly 7 years. That duration is down some from the 7.7 years that was listed previously and suggests the fund is a bit less interest rate sensitive now than it was previously.

However, at 7 years, the fund is still meaningfully impacted by rate changes nonetheless, which is actually a positive because of expecting some lower rates in the future that should bode well for the fund. It could see the fund’s NAV continue to increase as the underlying portfolio starts to appreciate further.

Again, that’s basically the crux of why muni bonds and muni bond funds, in particular, look particularly appealing at this time. Mostly tax-free income with the potential for some possible appreciation in the future with another potential catalyst of possible discount narrowing in these CEF wrappers.

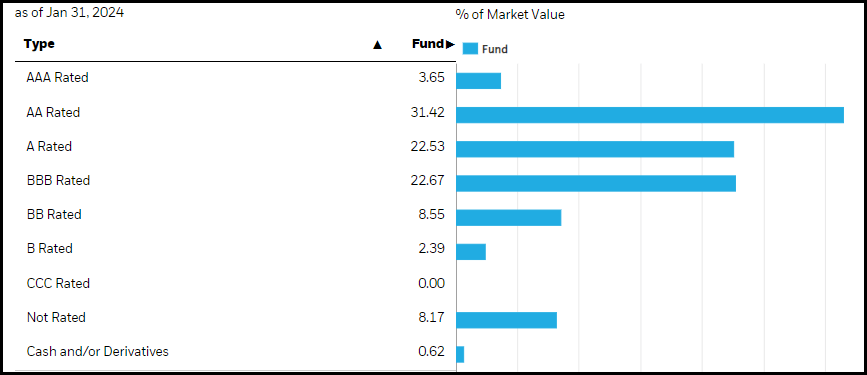

The credit quality of the fund’s muni portfolio has also remained fairly static since our last update as well. The fund is focused on higher quality muni holdings that get strong credit ratings; they’ve mostly avoided adding too much in below-investment-grade debt or debt that is not rated.

BMN Portfolio Credit Quality (BlackRock)

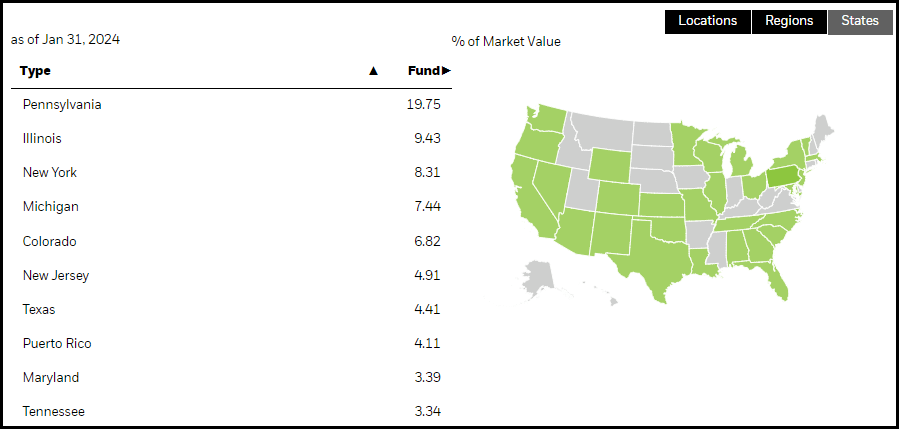

Looking at exposure to particular states, Pennsylvania is actually a large standout. This exposure increased materially since the last update, as it almost doubled while exposure slipped from almost all other states and territories.

BMN State Exposure (BlackRock)

This is quite interesting because Pennsylvania isn’t one of the five largest issuers of muni bonds that we often see; it’s generally California, New York, Texas, Illinois and Florida as the largest exposure for muni funds as they are the states that issue the most muni bonds. In this case, we don’t even see California or Florida listed in the top 10 here.

This could be a good thing for shareholders of this fund who live in Pennsylvania as well. They could benefit from having a meaningful portion of this income free from state taxes as well.

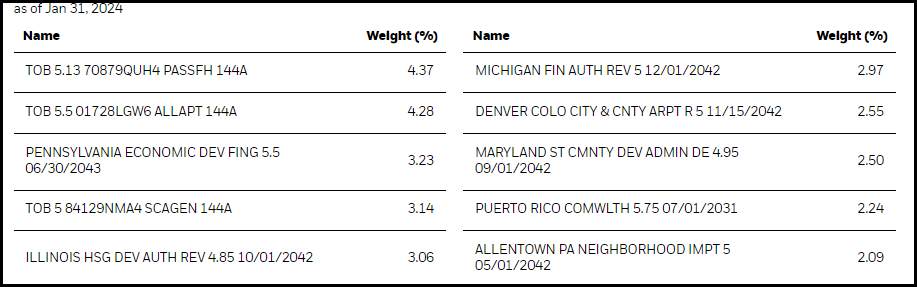

In looking at the top ten holdings more specifically, we see the bonds that were transferred to the TOB Trust as some of the largest exposures of the fund.

BMN Top Ten Holdings (BlackRock)

The percentage weight to each position doesn’t necessarily mean particularly heavy exposure to anyone holding. However, another common feature of most other muni funds is that they hold several hundreds or even thousands of different positions. With BMN at only around 100, even a bit below, that makes them a bit different at this time as well.

Conclusion

BMN launched at a particularly good time in late 2022, missing most of the drawdown that other municipal bond funds had to experience from a higher-rate environment. For that reason, the fund’s NAV is now higher than it was at inception, reflecting the fact they haven’t seen significant underlying erosion of their portfolio.

Further, they were patient when employing leverage instead of adding leverage immediately through the TOB Trust. Now that rates have mostly stabilized, they have been employing some leverage but have plenty of capacity to add further. That could put them in a situation to benefit relative to their already heavily leveraged peers who don’t have that same capacity to add further borrowings. They would benefit if rates do come down as expected as we move forward.

Additionally, the fund’s discount looks appealing at this time as it has reached near a low since the fund’s launch. On an absolute basis, the fund’s discount isn’t as wide as the average muni bond CEF, but for being in a better relative position to peers, it seems attractive regardless.

Be the first to comment