Marcio Silva/iStock via Getty Images

It’s been a tough year for the semiconductor space, to say the least. We’ve expanded our coverage this quarter, publishing multiple times on 23 of the world’s most crucial semiconductors. We end every quarter reviewing our ratings and studying how our predictions have panned out over the past couple of months. We work in a forward-looking market, but believe reviewing our investment theses is essential to do what we do and do it well.

Our high-risk, high-reward stocks:

While we got a lot of backlash for non-consensus ratings on Nvidia (NVDA), Advanced Micro Devices (AMD), and memory giant Micron (MU), we’ve seen our predictions for the three pan out this quarter. We’ve upgraded NVDA, AMD, and MU since, although the stock prices for all remain volatile in the near term. We’ve also upgraded Intel (INTC) after the last quarterly report.

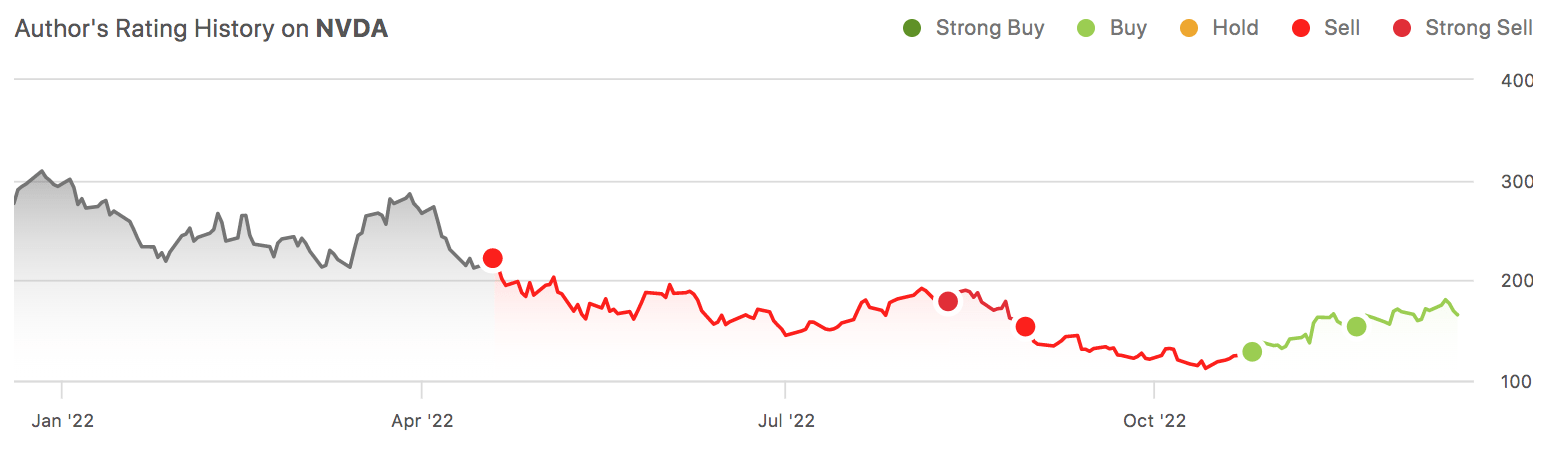

1. NVDA

NVDA’s been one of our greatest calls this year. We got a lot of backlash for our sell-rating for NVDA, but we believe our thesis regarding NVDA’s exposure to crypto-mining-related GPU sales has panned out and been followed by a sharp correction in 2H22. We upgraded NVDA at the end of October as we believe the gaming weakness has been priced into the stock.

We were a bit concerned about the impact of U.S. DoC export restrictions on Chinese customers. Still, we expected new product cycles and inventory hoarding by Chinese customers to offset the U.S. regulations. We saw NVDA perform consistently with our predictions when the company surprised everyone with the new A800 that substituted the A100 getting around U.S. regulations. We believe the worst is behind for NVDA and maintain our buy rating. The stock’s been creeping back up since our upgrade, and we expect the stock to rally in 2023.

The following graph outlines NVDA’s stock performance and our ratings.

SeekingAlpha

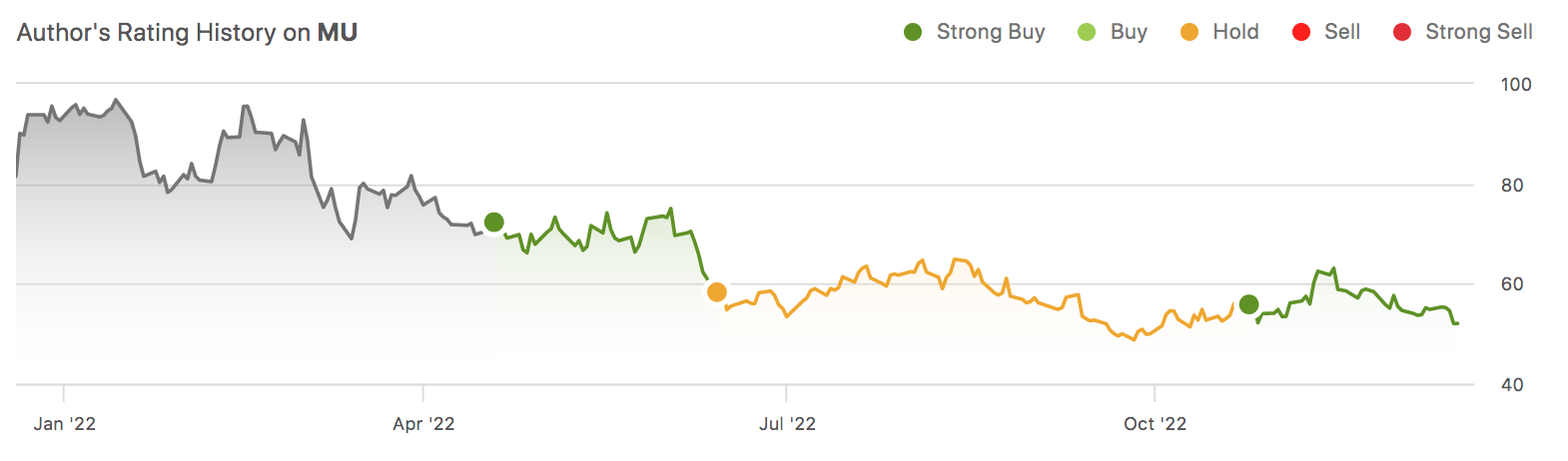

2. MU

2022 was specifically rough for the memory industry; we believe weakening consumer spending took a slice of MU’s revenue streams earlier this year. While we’ve been bearish on MU for most of the year, we upgraded the stock in late October based on our belief that the worst of memory weakness has been priced in.

The stock rallied for a bit after our upgrade, followed by a sell-off. The stock price is volatile, but we maintain our bullish sentiment as we believe MU has de-risked its guidance, pricing in the macroeconomic weakness.

The following graph outlines MU’s stock performance and our ratings this year.

SeekingAlpha

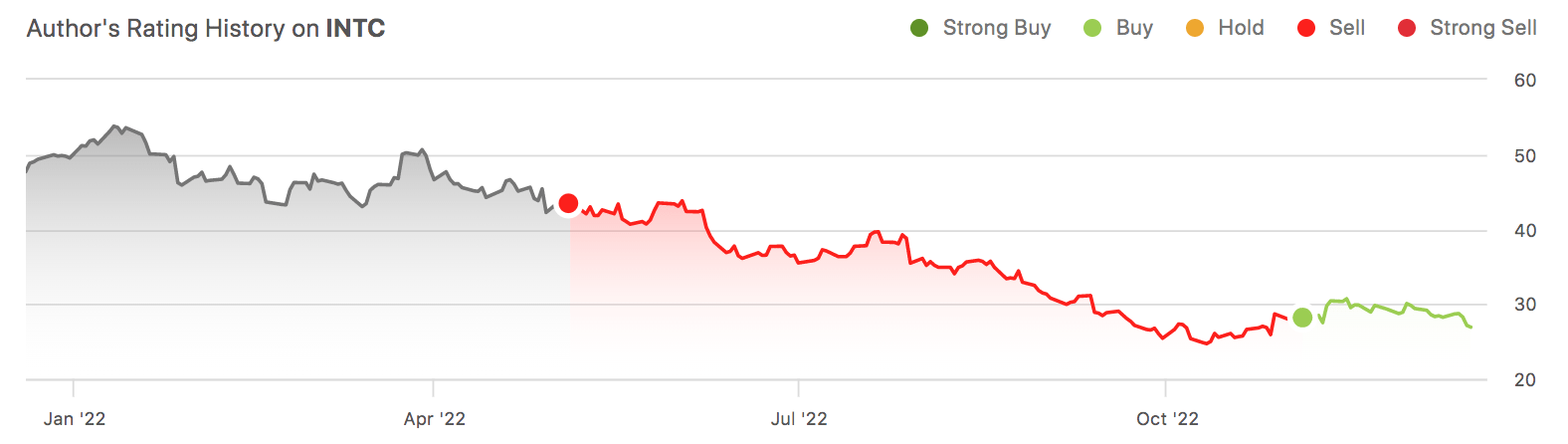

3. INTC

INTC was another interesting stock this year- we upgraded INTC this quarter as we believe the company’s financial performance will improve in 2023. We believe the company’s plans to become a U.S.-based fab will take capital and time. We don’t see INTC becoming a meaningful fab player before 2024. INTC’s stock performance isn’t the prettiest, but we expect the company will slowly recover toward 2H23.

The following graph outlines our ratings on INTC YTD.

SeekingAlpha

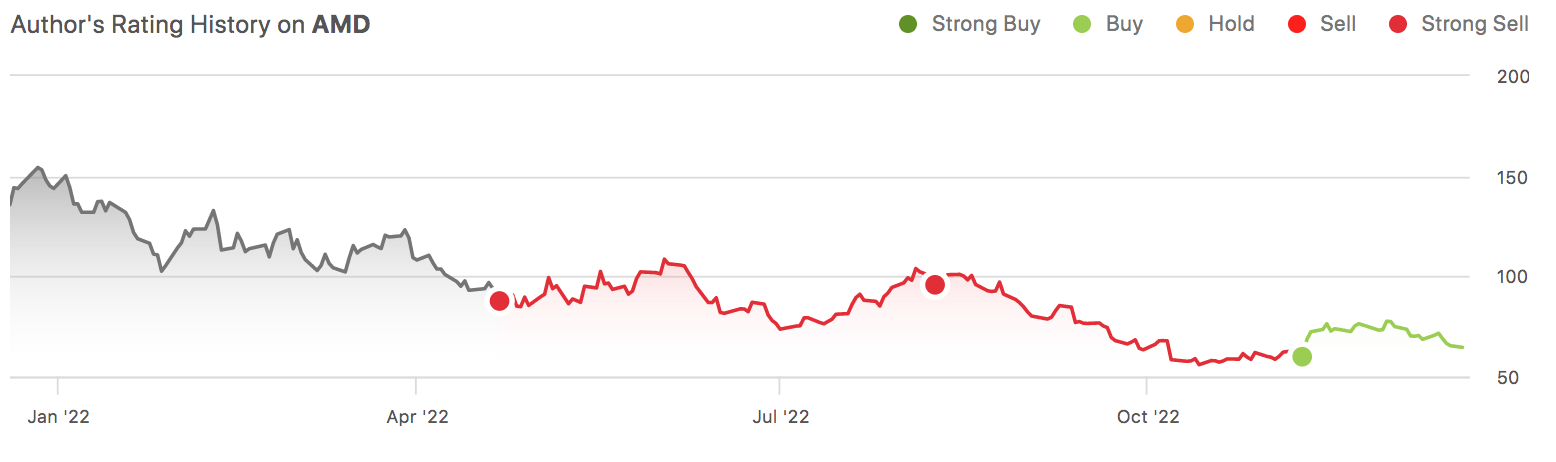

4. AMD

We upgraded AMD in mid-November and have seen the stock slowly pick back up. We believe most, if not all, the downside from weaker PC and gaming GPU demand have been priced into the company’s outlook. We expect AMD to outperform in 2023 and recommend buying the stock while it’s near the bottom.

The following graph outlines our rating history on AMD.

SeekingAlpha

Our still-bearish picks:

While we’re more optimistic about the semi space than we were a quarter ago, we remain bearish on specific stocks. Our biggest concerns this quarter have been in the storage space, namely Western Digital (WDC) and Seagate (STX).

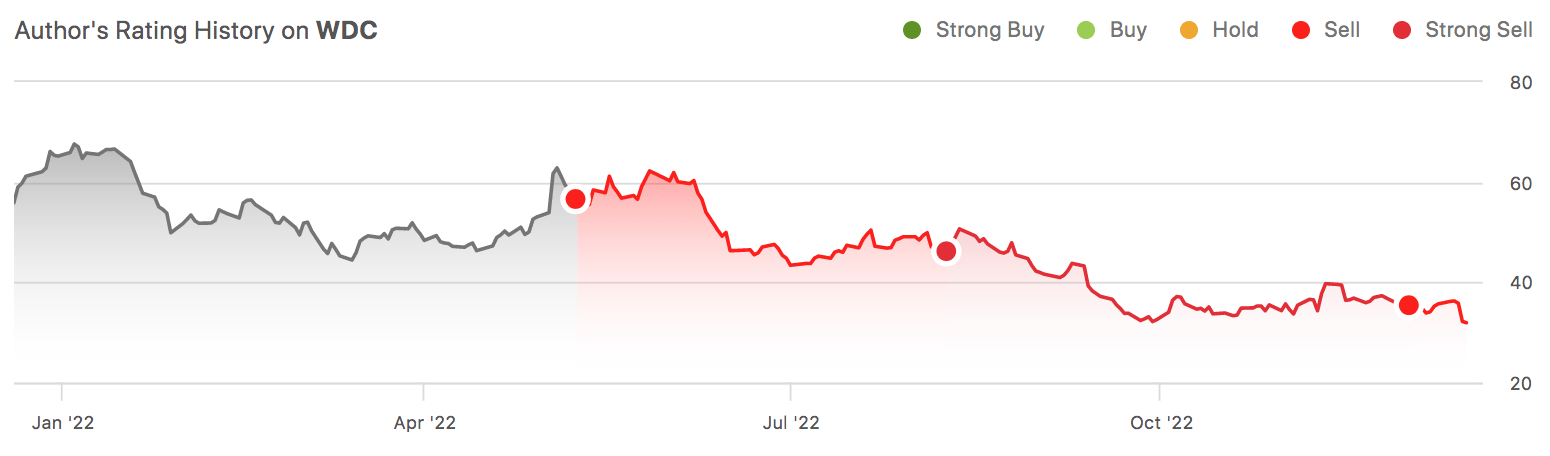

1. WDC

WDC has dropped nearly 44% since we first published our sell-rating on the stock. We expect WDC to continue to underperform based on our belief that consumer weakness is spreading into commercial markets. We believe the company will face demand headwinds in its flash and Hard Disk Drives (HDDs).

The following graph outlines our rating history on WDC.

SeekingAlpha

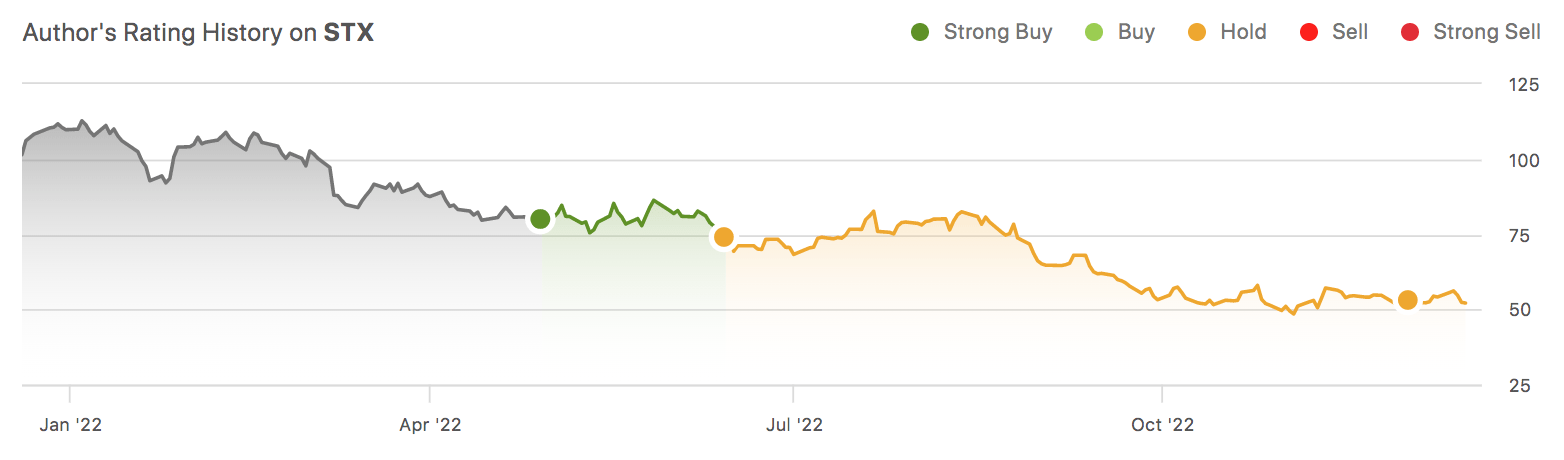

2. STX

STX is also on our list of bearish stocks this quarter. We’ve been hold-rated on the stock since July. Consistent with our beliefs, STX reported a 26% sequential decline and a 38% Y/Y drop in sales in 1Q23. We believe consumer weakness has slipped into storage demand and recommend investors wait on the sidelines for a better entry point on the stock.

The following graph outlines our rating history for STX.

SeekingAlpha

3. Global Foundries (GFS)

GFS has been a new addition to our coverage. We’re sell-rated on GFS despite the chip-maker reporting an outstanding 3Q22. We believe ASP increases drove revenue growth in the past year. In 2Q22, GFS reported a 16% increase in ASP per wafer while only reporting a 6% increase in unit shipments. Unit shipment remained low in 3Q22, increasing only 5% Y/Y. We believe the company won’t be able to maintain revenue growth through increased ASP and hence recommend investors exit the stock at current levels.

We believe the company had room to increase ASP this year due to the inflationary environment and supply shortages. We don’t believe they’ll have the same opportunity again with unit shipments normalizing due to the macroeconomic environment. We don’t see GFS growing meaningfully toward 1H23.

Timing is everything; where we could’ve gone better:

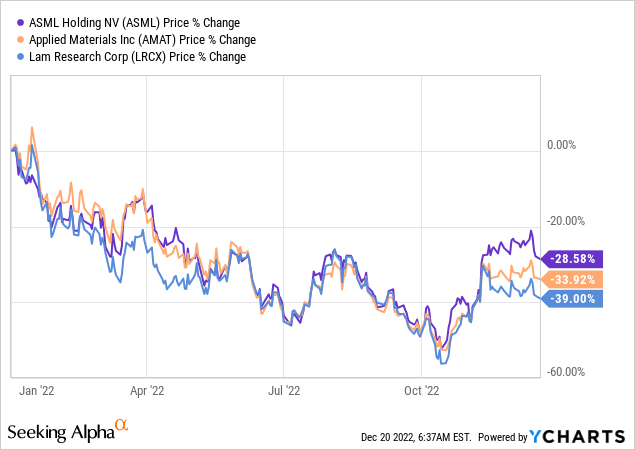

We like to look back at the quarter and see what calls could have gone better. AMAT and LRCX had a bumpy year. While we’re bullish on both stocks now, we should have downgraded them to a sell before the dip in October. The semiconductor industry is cyclical and reacts to the market. In turn, we expect to see the semi space begin to recover, headed by the semi cap stocks ASML, Applied Materials (AMAT), and Lam Research (LRCX). While we believe our expectations will pan out towards 2023, we should have downgraded before the dip and then upgraded again near the bottom to maintain our slogan of buy low, sell high.

We’re constructive on the semi-cap, as we expect the semiconductor expansion into U.S.-based fabs will boost demand for semi manufacturing equipment. We’re seeing the semi-cap slowly pick up after a deep dip in October.

The following graph outlines our top picks in the semi-cap space over YTD.

TechStockPros

What we recommend you do with the stocks:

Throughout our coverage of the semiconductor space, we’ve maintained a non-consensus outlook of the industry. We’ve been more bullish this quarter, as we believe the semi space provides favorable entry points that we haven’t seen since the market dip at the beginning of the pandemic. This quarter’s biggest takeaway from the semiconductor industry has been: to buy into the world’s most crucial semis once the weakness has been priced in. As supply improves and inventory corrections are underway, we expect the semi space to slowly but surely recover. We will continue to be forward-looking and monitor how our ratings materialize or fail to. The semi space should remain volatile over the coming quarters, but we believe we’re riding the upward trend higher in 2023.

Be the first to comment