Bet_Noire/iStock via Getty Images

Introduction

The past few years have been an ordeal to deal with Ardagh Metal Packaging (NYSE:AMBP). Although this was one of the more promising de-SPACs with an actual revenue-generating and profitable industrial activity, the company continued to underperform while there were also some question marks around corporate governance (like issuing high-yield preferred shares to the majority shareholder). As I remain convinced about the future of aluminum beverage cans and as peers Ball (BALL) and Crown Holdings (CCK) were also reported demand was weakening as customers were reducing inventory levels, I decided to cut Ardagh some slack. But I obviously wanted to see an improvement soon.

Q1 met the expectations

This article is meant as an update on previous articles, which you can all find here.

When the company published its Q4 and FY 2022 results, it promised to post a 10% increase in the adjusted EBITDA result. As the adjusted EBITDA in FY 2022 came in at $625M, the 2023 guidance implied an EBITDA of $690M. Ardagh emphasized the majority of the EBITDA (and EBITDA increase) would be weighted towards the second semester. That was also clear based on the Q1 guidance: Ardagh guided for a Q1 adjusted EBITDA of $130M.

It seems like that guidance was a pretty low hurdle the company had set for itself. And fortunately Ardagh met that guidance as its Q1 EBITDA came in at exactly $130M.

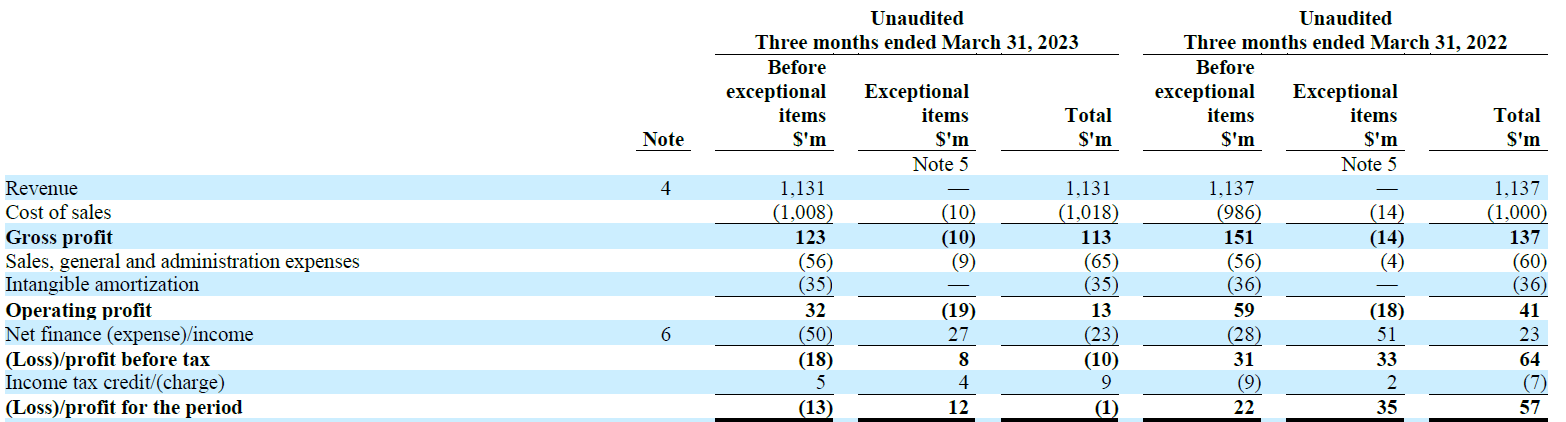

That wasn’t enough to be profitable. As you can see below, the $130M in adjusted EBITDA was generated on a total revenue of $1.13B resulting in an EBITDA margin of just under 12%.

AMBP Investor Relations

That EBITDA margin should continue to increase throughout the year but it wasn’t sufficient to post a net profit and the net loss was approximately $1M.

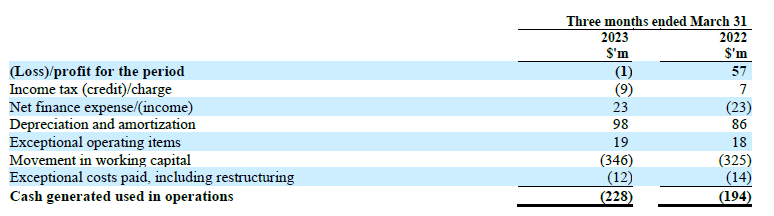

I have always looked at Ardagh from a cash flow perspective, and I see no reason why I should change that approach. Ardagh uses the ‘cash used in operations’ as starting point of its cash flow statement, but I think it’s important to have a look in the footnotes to see what exactly is included in the starting point. As you can see below, this includes about $346M in working capital investments as well as a $12M restructuring and exceptional cash expense.

AMBP Investor Relations

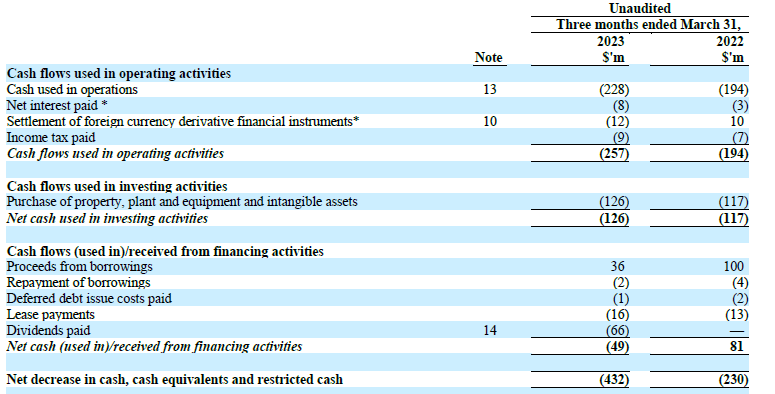

This means that on an adjusted basis, the cash generated by operations wasn’t a negative $228M but a positive $130M and the operating cash flow was $101M (note: the cash interest payments are low in Q1 and Q3 but higher in Q2 and Q4).

AMBP Investor Relations

We should also deduct the $16M in lease payments and thus end up with $85M in adjusted operating cash flow. Not sufficient to cover the $126M in capex but there are two mitigating elements here. First of all, considering Ardagh confirmed the full-year EBITDA guidance, less than 19% of the full-year EBITDA was generated in the first quarter. As the EBITDA will incrementally get better while other expenses (including capex) will either remain stable or decrease, the higher EBITDA in the next few quarters should result in a positive free cash flow.

Secondly, the majority of the capex still consists of growth capex. As showing in my previous article, the sustaining capex was just around $100M per year. That’s around $25M per quarter (the Q1 sustaining capex was $36M and will likely be lower in the next few quarters) and thus substantially lower than the total capex. This also means that in the first quarter, the sustaining free cash flow was a positive $60M. That’s great but not very helpful as the growth capex is still being incurred. In an ideal world, Ardagh would have to choose between growth and the very generous dividend which is costing the company in excess of $60M per quarter ($60M in dividends on the common shares and $6M in preferred dividend payments).

For the second quarter, Ardagh is guiding for an adjusted EBITDA of $170M. That’s positive because of two reasons: it shows an important QoQ improvement and the company gets one step closer to the full-year EBITDA guidance. At $170M EBITDA, the normalized operating cash flow should come in at around $100M per quarter (I’m also applying a normalized tax rate and normalized quarterly cash interest expense here). This also means the full-year EBITDA guidance of $690M should be sufficient to generate about $400M in adjusted operating cash flow. That will be sufficient to cover the sustaining capex ($100M) and the growth capex (estimated at around $300M). If you’d look at the sustaining free cash flow, the dividend is still fully covered. But I’d be happy to forego the generous/excessive dividend to put the company in a better position.

Fortunately, the growth capex will fall to close to zero in 2024. From the Q1 conference call:

the capital expenditure we have this year is just the wrap-up of the projects that we’ve essentially more or less completely finished. So we have some payments this year. So the cash CapEx, I think of the order of $300 million, some leasing activity on top of that. And therefore, there’s a very meaningful step-down into 2024.

And:

So in the $300 million, it will drop by a lot. I think the market has got a couple of $100 million down from that. We’re not disagreeing with that.

Investment thesis

While it is nice to receive a pretty outsized dividend of $0.10 on a quarterly basis (in absolute terms as Ardagh still is one of the largest positions in my portfolio), I’d rather see the company preparing itself for the future by A) self-funding the growth capex and B) putting money aside for debt refinancing. While the company has done an excellent job in locking in low interest rates on the vast majority of its debt, it will likely have to deal with substantially higher interest rates in the second half of this decade. While that still feels like it is far away, let’s not forget that if the gross debt doesn’t decrease from the current level of $3.63B, a 200 bp cost of debt increase will reduce the free cash flow by in excess of $50M per year (after taking the tax implications into consideration). So I think it’s definitely important to be mindful of that and I’d rather see a large portion of the current $240M in common dividend payments be used towards covering the growth capex as well as buying back some of the bonds which are currently trading at a large discount on the secondary markets. While the dividend is very nice to see and have, I’m not sure the current dividend policy is benefiting the common shareholders in the long run.

I’m already relieved the company has met its Q1 EBITDA guidance and I’m encouraged by seeing the full-year EBITDA guidance being confirmed. But I really wouldn’t mind a dividend cut – on the condition the cash will be put to good use.

I still have a long position in Ardagh and it still is one of my largest positions. But the company will have to start to deliver on its promises soon. And I am very hopeful the sharply reduced growth capex to be incurred in 2024 will help the company to be free cash flow positive, both on an adjusted basis as well as on a reported basis.

Be the first to comment