DISCLAIMER: This article is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this article is not an offer to sell or buy any securities. Nothing in it is intended to be investment advice and it should not be relied upon to make investment decisions. Cestrian Capital Research Inc or its employees or the author of this article or related persons may have a position in any investments mentioned in this article. Any opinions or probabilities expressed in this report are those of the author as of the article date of publication and are subject to change without notice.

Background

We initiated coverage of Iridium Communications (IRDM) here on SeekingAlpha in June last year – you can find that note here. Since that time we’ve covered the company continuously with a similar message which is to say – this is a rock-solid business that we expect to continue to grow. It’s our absolute favorite telco for its purity, and it’s also one of very few pureplay space-sector stocks (the others include Maxar Technologies (MAXR) and Virgin Galactic (SPCE) which we also cover).

Our goal in our research work and in our own personal investing activity is to find stocks that can beat the S&P500 over the long term, and hopefully find a few short-term winning trades in that same stable of stocks. IRDM has been a great pick for us so far on both fronts, and its recurring revenue, government-contract dominated business model makes it a stock where one can easily sleep at night.

Looking For Resilient Stocks

During the current correction, we’re reviewing stocks in our coverage universe to learn their behavior in bad times – their speed of correction, where they bottom out, the degree to which the actual business is hit versus just the stock, and so forth. As we’ve said many times, here at Cestrian Capital Research we are staffed by old folks who have worked through several such episodes, including the dot com crash and slow rebuild of 2000-3, SARS in 2002-3, the great financial crisis of 2008-9, the Euro crisis of 2010-12 and plenty of other smaller hits. So we’re fairly sanguine about this one whilst still thinking the market is likely to continue to decline from here (we write as trading was just halted – not a normal Monday!). We posted on the topic here on Feb 28 saying we felt there was plenty of room to fall from there. So far that’s been the case.

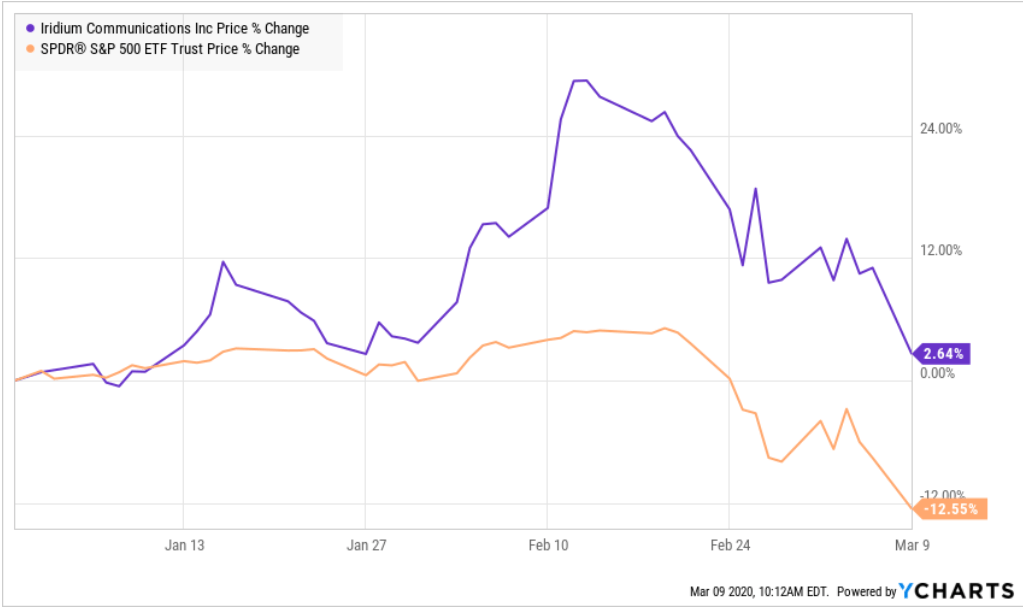

IRDM has held up well year to date. Here’s the YTD chart vs. the S&P500 ETF proxy, SPY.

{kind=link}

The stock has had a number of positive catalysts, including refinancing of its debt load, improvements in its joint-venture Aerion air traffic business, and others. In addition, market perception of the stock is improving, from “Iridium? Wasn’t that a bankrupt Motorola plaything?” to “Iridium? It’s going to be paying a dividend soon, right?”.

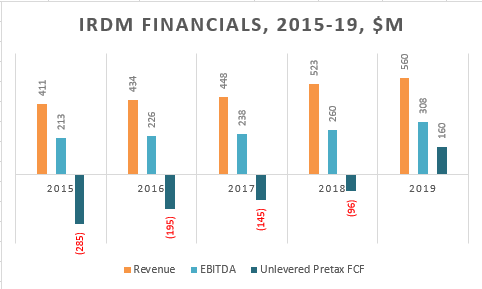

Perception in this case is lagging reality. IRDM is a machine these days. Here’s the last five years’ summary numbers. In the chart below, “unlevered pretax free cashflow” is the normal definition we use – it’s EBITDA minus change in working capital minus capex – in other words it’s the money the business actually produces before it pays the IRS or its lenders.

You see steady revenue growth, steady EBITDA growth, and unlevered pretax FCF steadily becoming less negative before moving positive in 2019. That reflects the capex cycle coming to an end. It will be a few years before IRDM has to spend major capex again – its satellite fleet has a c.15+ year life and we estimate at least 3 years before any major capex commitment (the company will tell you longer but let’s be cautious here).

Here’s the detail.

So that’s a resilient business.

The company isn’t immune from Coronavirus – lower economic activity in the market will affect everyone in the end – but given its core activity of providing communications of last resort to remote workers, first responders, warfighters and other highly demanding user segments, we think the revenue line will hold up well, and better than most. Costs and capex are predictable. So we think cashflow will continue to grow and with it we get nearer to a dividend, which will open up the stock to a whole new world of possible investors.

Current Valuation

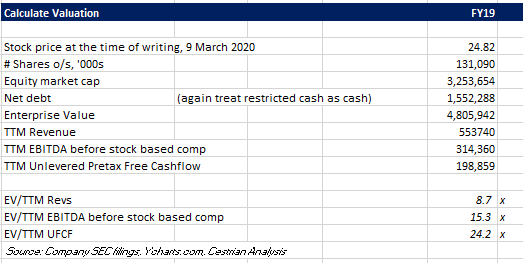

At the time of writing the market is asking you to pay 15.3x TTM EBITDA for 18% TTM EBITDA growth and accelerating cashflow growth.

If the market were stable right now we would call that an easy Buy. As it is, we’re on shifting sand so we remain at Neutral, with an eye to moving to Buy when things settle.

Cestrian Capital Research, Inc – 9 March 2020.

Thanks for reading our note. If you enjoyed it, try our SA subscription service, The Fundamentals.

We operate the ONLY space-sector service on SeekingAlpha.

Here’s what you get:

- Deep sector expertise & broad coverage in the space sector.

- Pro-grade analysis, easy-to-understand presentation.

- 100% independent, clear and direct opinion of stocks’ prospects.

- Long-term investment picks and short-term trading ideas.

- Absolute alignment with our own investing. We run a real-money service and we give you the heads up on every move we make. Any trade we make, you get to trade first.

We speak directly to our covered companies, often at CEO level.

Disclosure: I am/we are long IRDM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: We are long IRDM on a personal account basis.

Be the first to comment