Morsa Images/DigitalVision via Getty Images

There is great irony in the stock price of Zoom (NASDAQ:ZM). After the pandemic led to a hyperbolic acceleration in growth, the stock now finds itself trading lower than it did pre-pandemic. In other words, ZM is trading cheaper even though it is a much larger business, one generating robust margins even on a GAAP basis. Net cash makes up 25% of the market cap and the stock trades for 18x forward earnings. Overall growth has slowed down considerably, but much of that has to do with the online business struggling post-pandemic, with that being offset by a still-fast-growing enterprise business segment. This once-tech-bubble is now trading at highly buyable levels, offering a “growth at a reasonable price” kind of valuation.

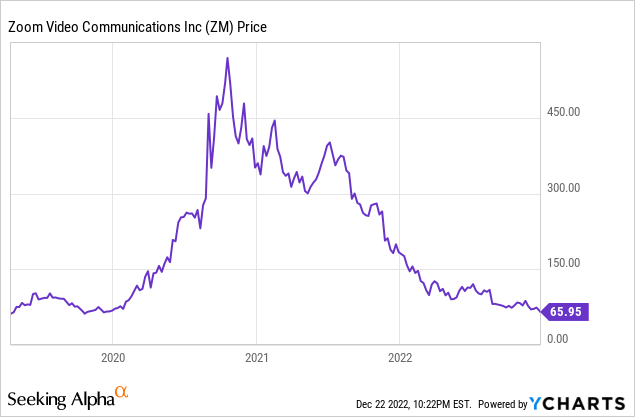

ZM Stock Price

It has been many quarters since ZM traded at the bubbly valuations it did during the pandemic. ZM has fallen so much that it is trading lower than it did when it came public.

Some may point out that ZM was a high-flying stock at the time of its IPO, but revenues are 12x higher than they were in 2019. I last covered ZM in September, where I rated the stock a buy as a profitable tech name amidst the crashing tech sector. The stock has fallen another 10% since then, in spite of arguably resilient fundamentals and an ongoing share repurchase program.

ZM Stock Key Metrics

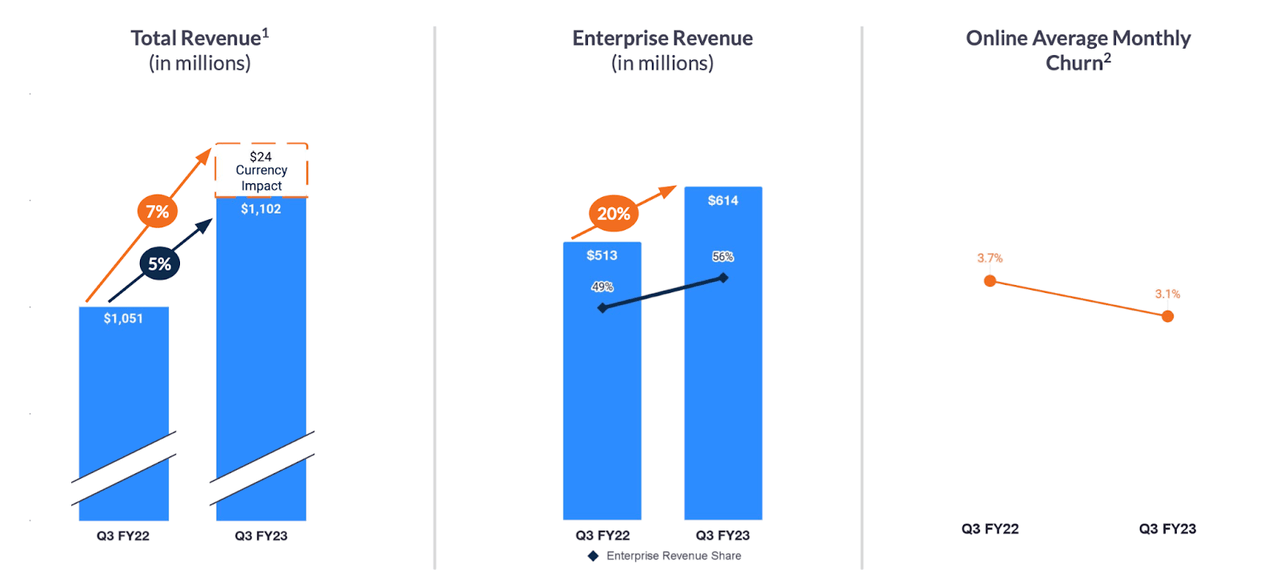

In its most recent quarter, ZM delivered 5% revenue growth (or 7% on a currency neutral basis). Whereas Online revenues declined 9% YOY, enterprise revenue grew at a robust 20% clip.

FY23 Q3 Presentation

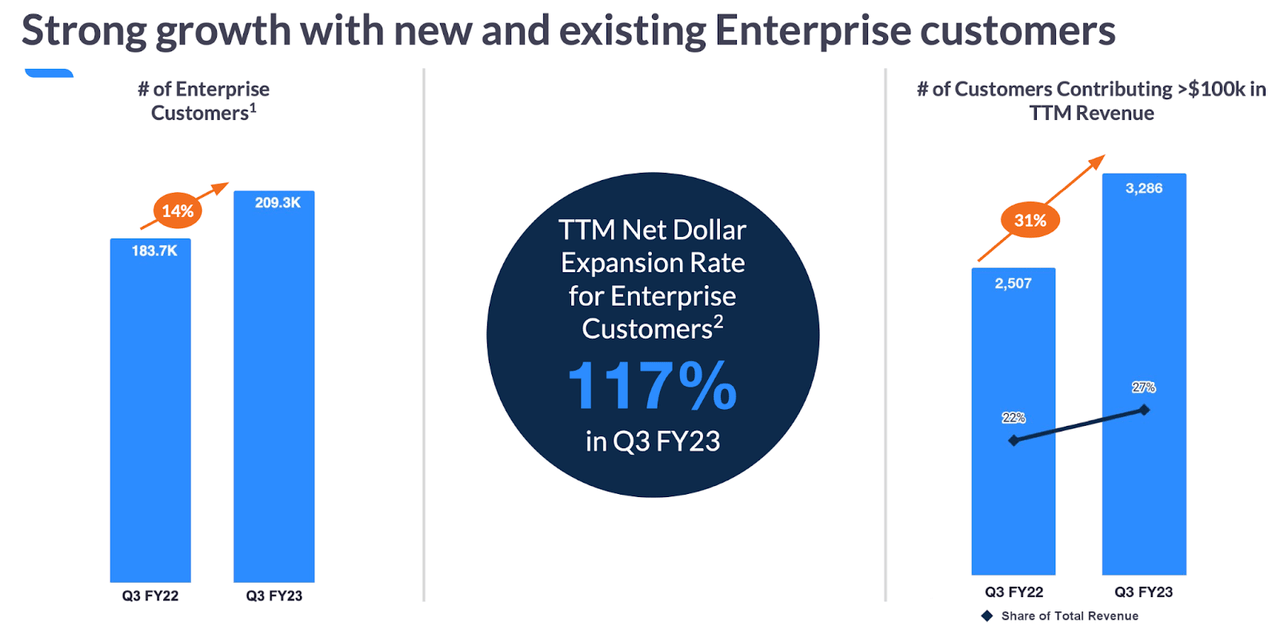

ZM continued to grow its enterprise customer base, with total customers growing by 14%. ZM generated a 117% net dollar expansion rate over the trailing twelve months.

FY23 Q3 Presentation

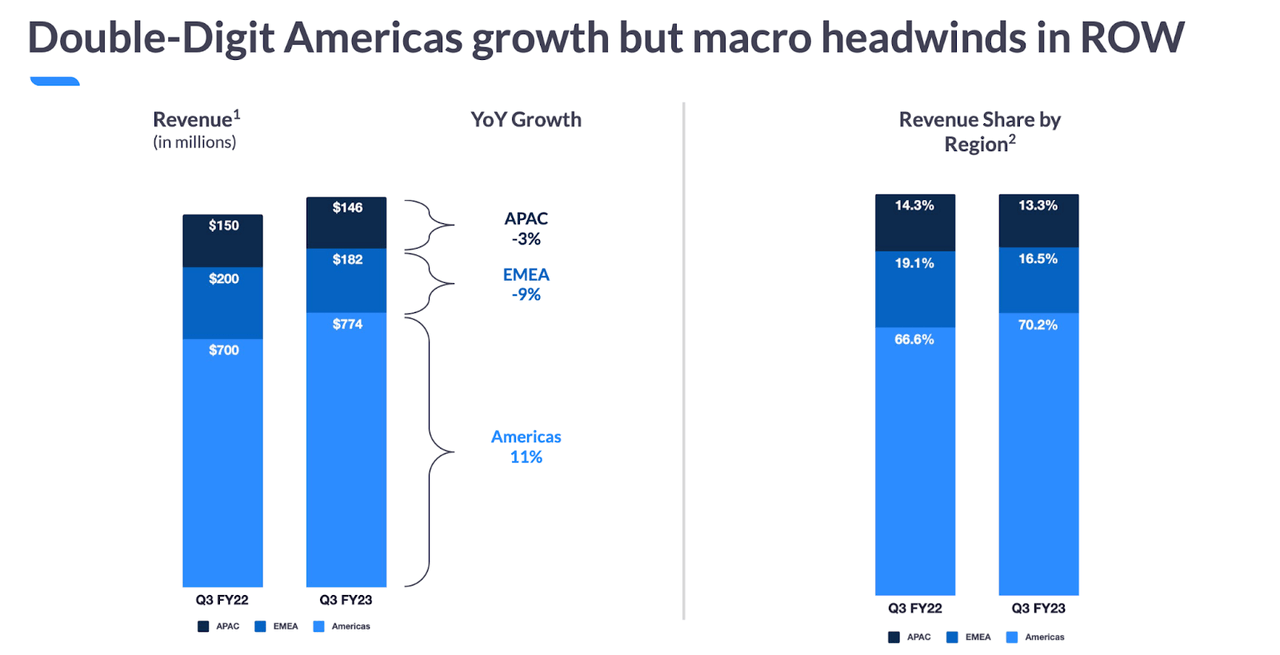

ZM also appears to be held back by localized macro headwinds. Whereas the Americas grew at a double-digit pace, it experienced negative growth everywhere else. That was in large part due to both currency fluctuations as well as the Ukraine war.

FY23 Q3 Presentation

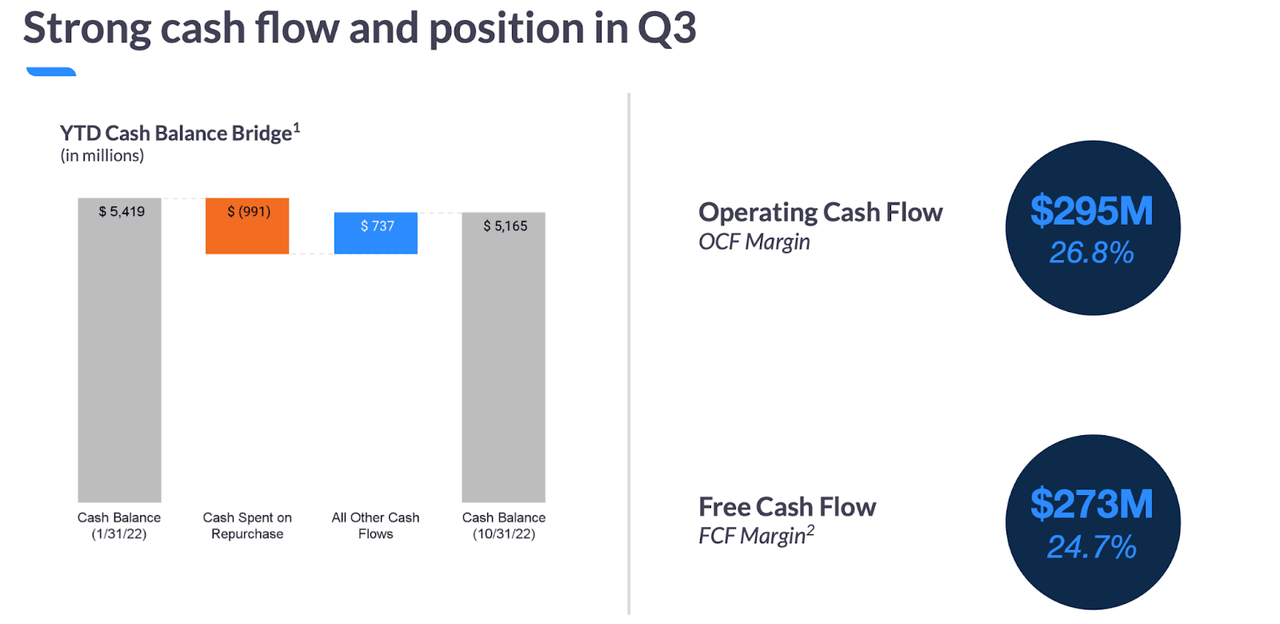

While growth is slowing down, ZM has emerged from the pandemic as a mature tech company with robust profit margins. ZM generated $273 million of free cash flow in the quarter, good for 24.7% of revenues.

FY23 Q3 Presentation

ZM ended the quarter with $5.165 billion of cash versus no debt – that net cash position made up around 25% of the current market cap. With a strong balance sheet and robust margins, ZM was able to repurchase $990.8 million of stock year to date.

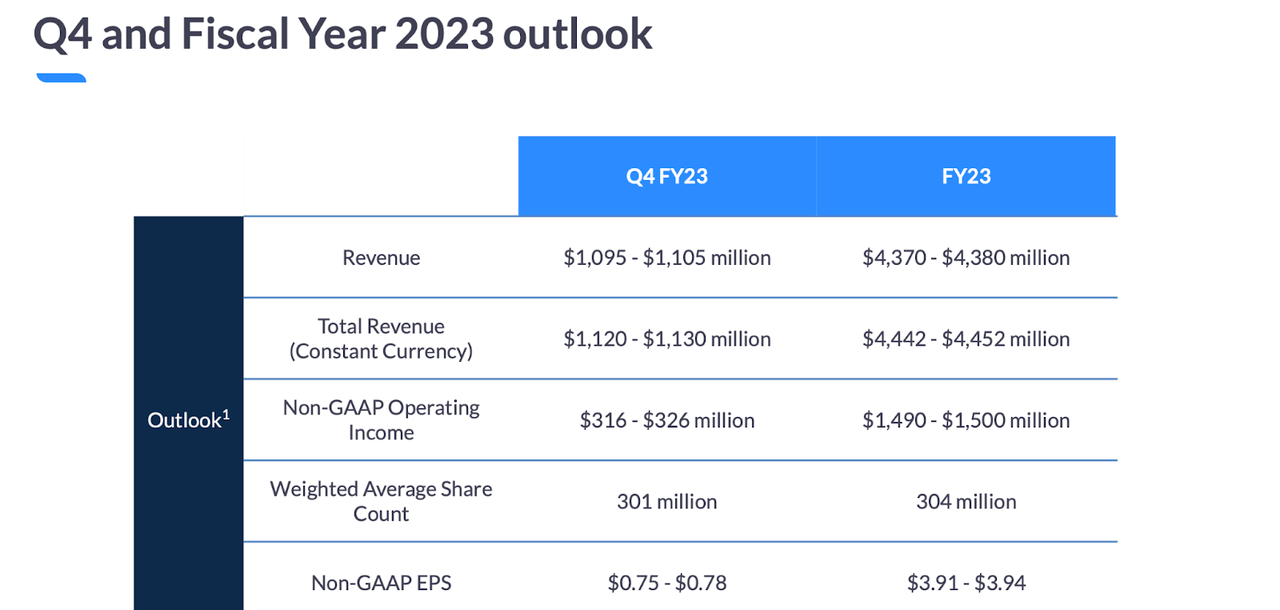

Looking ahead, ZM expects $1.1 billion in revenues in the fourth quarter, representing just 3.1% YOY growth.

FY23 Q3 Presentation

On the conference call, management broke out the projected growth as coming from 8% expected declines in the Online business which would be more than offset by “low-to-mid 20s” growth in their Enterprise business. Management believes that their Enterprise business can sustain growth due to the fact that the company is not just a video conferencing company but instead a complete communications company, with many customers eventually adding on more products to their catalog.

Is ZM Stock A Buy, Sell, or Hold?

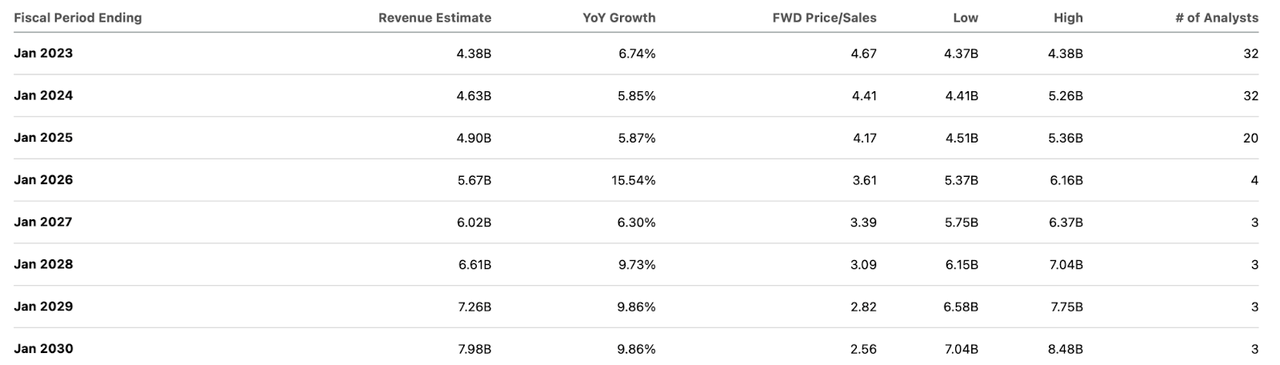

At recent prices, ZM is trading at 18x earnings and is expected to grow its top-line at a single-digit clip moving forward.

Seeking Alpha

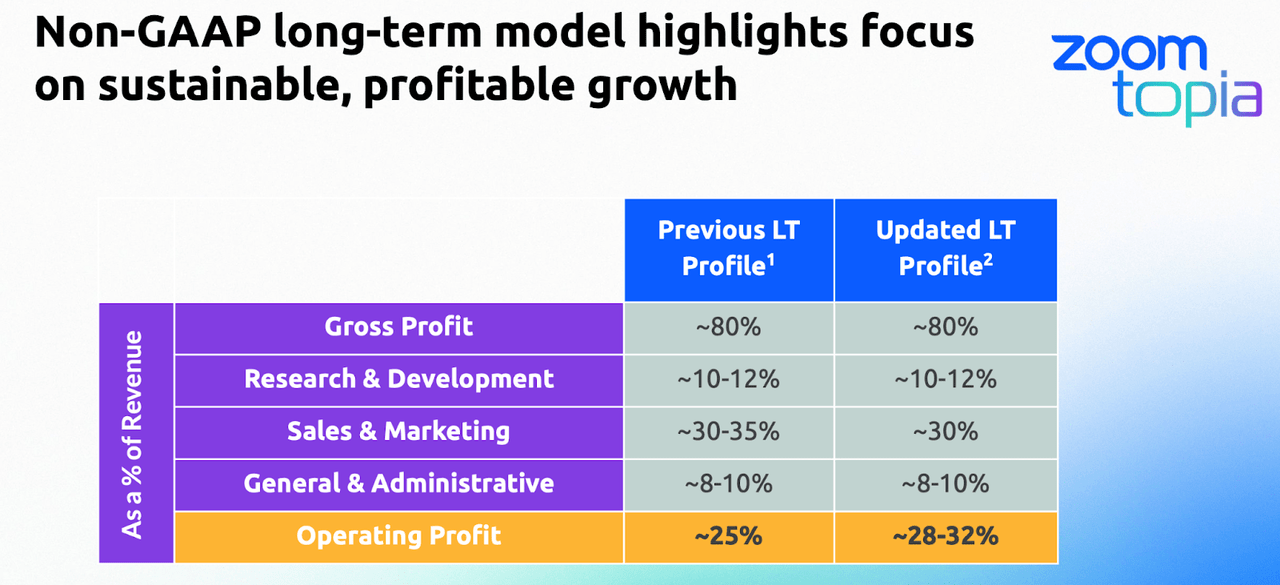

Between its 18x earnings multiple and single-digit projected growth rate, the valuation looks reasonable at the very least. Yet I suspect many investors are buying the stock on a sum-of-the-parts basis, with the Enterprise segment being the crown jewel. ZM did $614 million in enterprise revenues in the latest quarter and it is projected to grow in the 20% range for a while. What might this segment be worth? ZM has guided for 32% operating margins over the long term.

2022 Investor Day

Considering that ZM is already operating at 34.6% margins as of the latest quarter, I expect that target to prove too conservative. Using 32% long term net margins, a 20% growth rate, and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see the Enterprise segment being valued at 10x sales, or $24.6 billion. For the Online business, we can value that at 2x sales giving a valuation of $4 billion. That $28.6 billion estimate far surpasses the current $20.4 billion market cap (and I note that I have not assigned any value to the 25% net cash balance sheet). As the company continues to repurchase stock, I can see the valuation re-rating higher as the market rewards the stock for the cash flow generation and potential for operating leverage.

What are the risks? Competition may be the most important risk. ZM’s negative growth in its Online segment is easily explainable as being due to the post-pandemic recovery, but it is possible that Microsoft Teams (MSFT) eventually takes market share in the future. Customers might prefer to use Teams as part of a larger MSFT bundle. ZM historically won market share arguably due to having a superior product to the incumbent Cisco Webex (CSCO), but the mega-cap cloud titan MSFT is likely to create a highly competitive offering moving forward. As far as valuations go, there is risk that the Enterprise segment sees weakness amidst a tough macro backdrop – if growth rates for the next year end up falling closer to 10% than 20%, then I could see the stock getting hit as the Enterprise segment is really the only thing supporting the valuation. ZM is trying to increase growth by increasing its free-to-paid conversion, but such efforts may hurt its market share growth over the long term. As discussed with subscribers to Best of Breed Growth Stocks, a portfolio of undervalued tech stocks is my preferred way to take advantage of the tech stock crash. ZM fits right in with such a portfolio as a higher quality allocation due to the strong balance sheet and profitability – I rate the stock a buy.

Be the first to comment