shaunl

Thesis

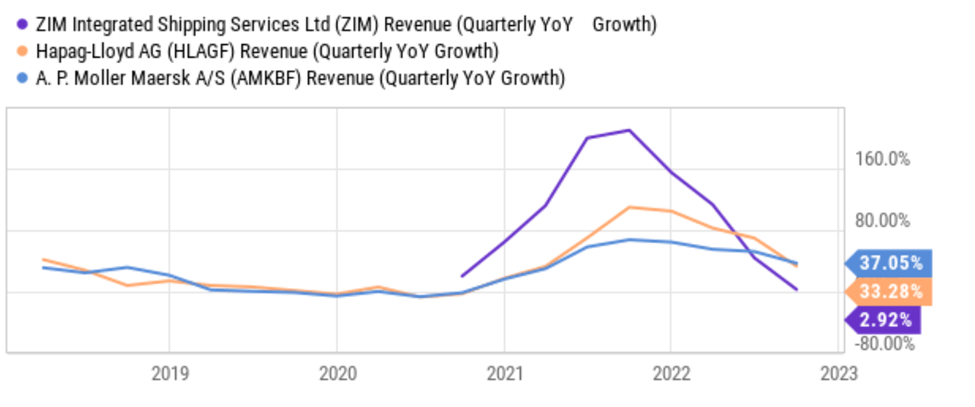

ZIM Integrated Shipping (NYSE:ZIM), as the world’s 10th largest ocean carrier, has grabbed investors’ attention disproportionately in the past 1~2 years. And a major reason involved its tremendous earnings and stock price performance during the recent shipping boom, unexpectedly catalyzed by the COVID pandemic. As you can see from the following chart, compared to its peers such as Maersk’s and Hapag-Lloyd’s, its revenue growth literally exploded in an already-skyrocketing sector. Take Hapag-Lloyd as an example – its YOY quarterly revenue growth registered almost 100% during late 2021 which is really an astronomical growth rate. However, such a growth rate only pales when compared to ZIM’s growth rate during that period. ZIM YOY quarterly revenue growth almost peaked at 200%, doubling that of Hapag-Lloyd.

And this leads me to the main thesis of this article. in the remainder of this article, I will argue that its above outperformance was largely caused by its concentrated capacity in the high-earning transpacific routes. Such exposure is a double-edged sword, and now I anticipate it to hurt ZIM more than other peers.

Source: Seeking Alpha data

Importance of the Transpacific route

ZIM’s main contract exposure is on the transpacific trade routes. And about 50% of the trade volumes on this route would be under annual contracts renegotiation each year. ZIM has recently confirmed that this year, the rates for the transpacific trade routes were renegotiated lower according to this report from the BoA Global Research.

And I anticipate such lower rates to hurt ZIM more than other peers for a few key reasons. And as you can see from the chart above, the impacts are beginning to show already. ZIM rose faster during the boom than its peers as just mentioned, and now its revenues are also falling much faster than its peers as the rates begin to renormalize. To wit, as of the most recent quarter, Hapag-Lloyd reported a year-over-year quarterly revenue growth rate of 33%, a far cry from its peak growth rate of over 100%. And ZIM YoY revenue growth fell much more quickly to 2.9% only. And next, I will argue that such a fall would continue for a few key reasons.

The first reason is that shipping volume on these lucrative routes is also falling. During its Q3 earnings report, management reported a worse-than-expected Q3 volume decline of -5% and further attributed the decline mainly to lower volumes on the Transpacific routes. As a result, it also lowered its 2022 volume guidance to below the 2021 levels (compared to earlier guidance of a 2~3% expansion).

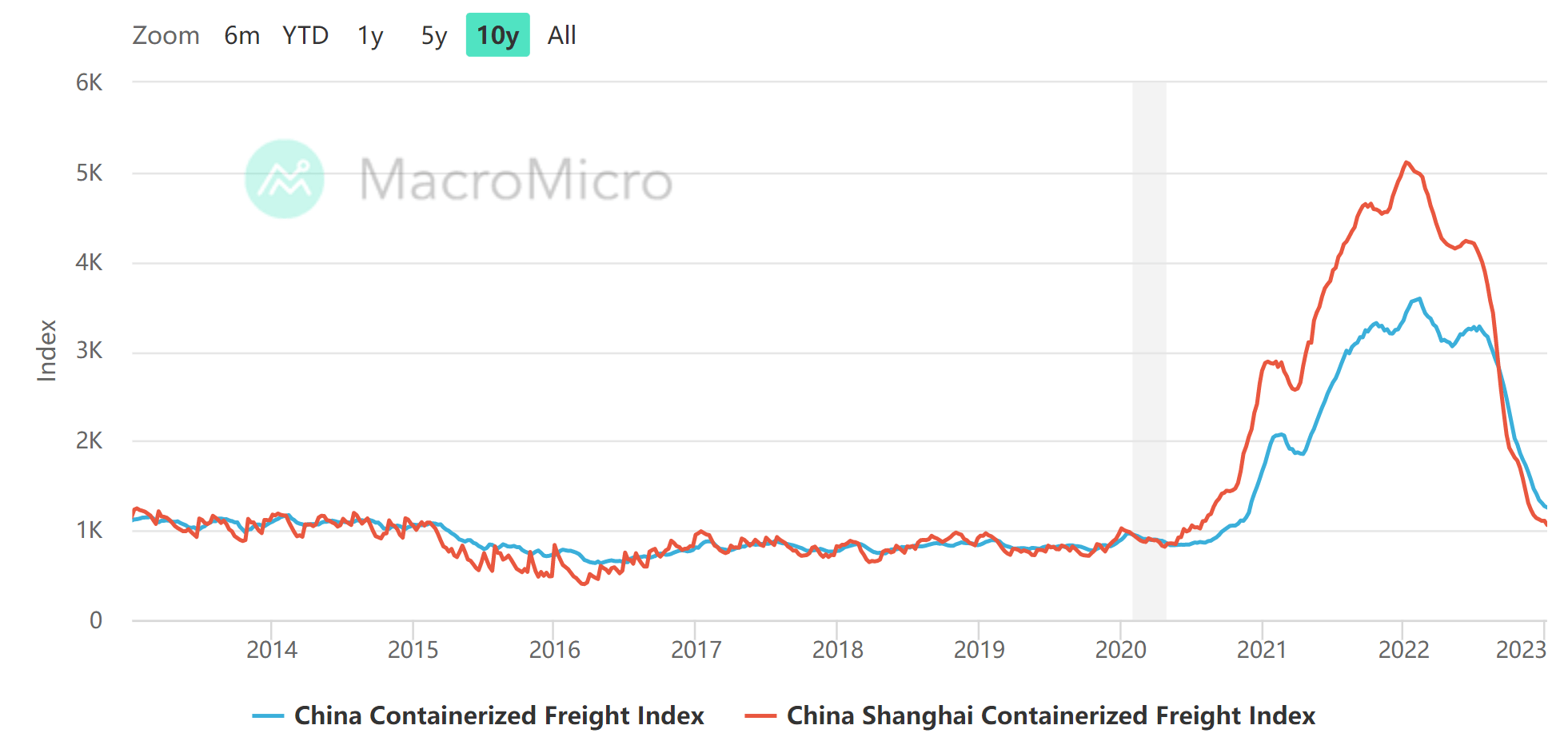

The second reason is the key SCFI index (the Shanghai Containerized Freight Index) keeps declining sharply as seen in the chart below. The index has dropped by about 80% YoY.

Even in the past month, the China Containerized Freight Index dropped from 1,271 in Dec 2022 to the current level of 1,255 (first week of January 2023). And a bit of background on the importance of the index as provided by DSV (slightly edited by me):

The Shanghai Containerized Freight Index is the most widely used index for sea freight rates for import China worldwide. The index is therefore named after the largest container port in the world, Shanghai. The SCFI is based on the most used trade routes from Shanghai: Europe, Mediterranean, United States, Persian Gulf, New Zealand, West and South Africa, Japan, Southeast Asia and South-Korea.

Looking ahead, I anticipate the contraction of the SCFI index to persist at least during 2023, if not longer. China’s COVID situation is still very fluid. After it abandoned its zero COVID policy recently, there had been a large resurgence of cases, which could cause it to reconsider its COVID control strategies. At the same time, there are good possibilities that the global economy would suffer a slowdown as the Russian/Ukraine situation drags on, high inflation continues, and the U.S. continue tightening its monetary and fiscal policies. The shipping sector typically is the sector that responds most sensitively to economic slowdowns.

Source: MacroMicro data

Valuation difficult to sustain even at $10 share price

Finally, in terms of valuation, the stock is still quite expensive despite its price plummeting from the peak level of ~$90. With an FW PE around 0.5x, ZIM seems to be a dream coming true for value investors. However, it is nothing but the way I see things.

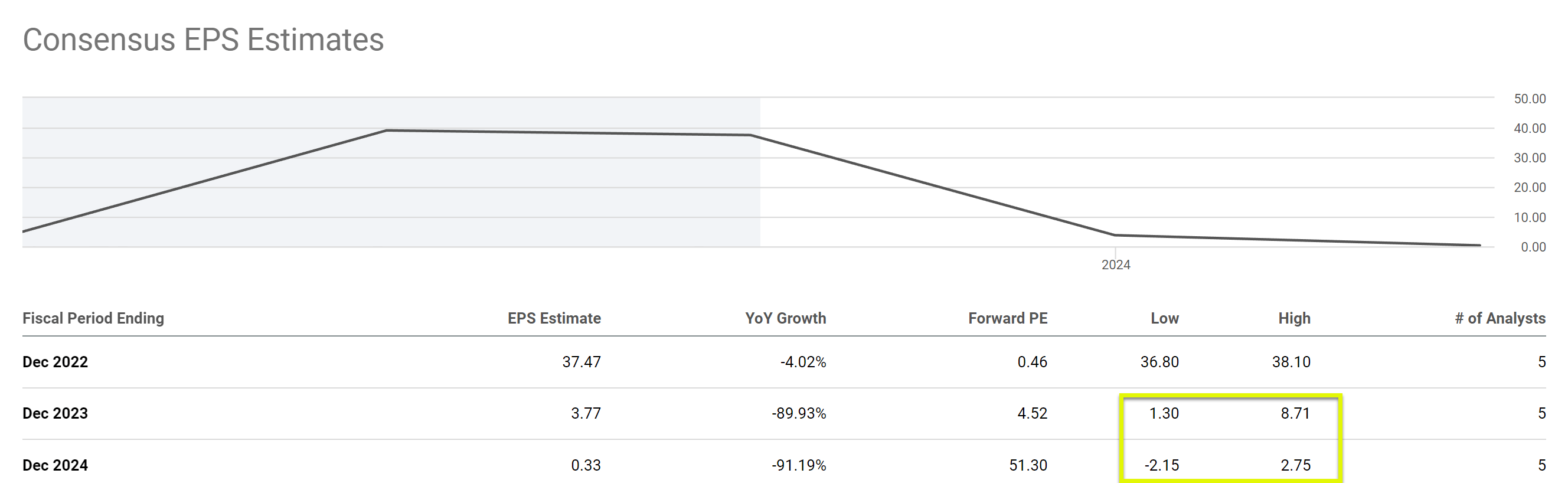

I see its EPS drop sharply due to the deadly combination of lower volume and lower rates as analyzed. And consensus estimates seem to share this gloomy view as you can see from the chart below. More specifically, consensus estimates project its EPS to be $3.77 in 2023, almost only one-tenth of what it is in 2022. And in 2024, the estimate is $0.33, less than one-hundredth of its 2022 level. More importantly, note the variance in the consensus estimates as highlighted in the yellow box. Such a large variance really speaks volumes of the risks ahead.

Source: Seeking Alpha data

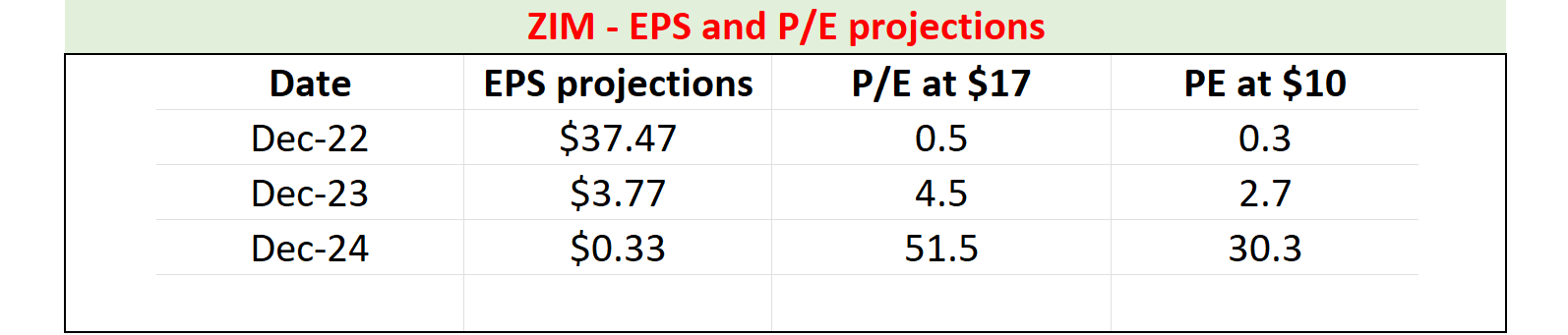

Even based on the mid-points of the consensus estimates (which is a quite optimistic assumption in my view because of the large variance just mentioned), I see its valuation as not sustainable even if its stock prices further drop to the $10 range. As seen, with the mid-point EPS projections, the P/E multiple at a share price of ~$17 (its current price as of this writing) would be about 4.5x in 2023 and 51.5x in 2024. And even at a share price of $10, the P/E multiple would still be 2.7x in 2023 and 30.3x in 2024. To me, these PE multiples are probably the opposite of a value stock, especially if you consider the highly cyclical nature and narrow moat of the container business.

Source: Author based on Seeking Alpha data

Summary and final thoughts

This article mostly focused on the downside risks. And before closing, I wanted to point out some of the upside risks to my thesis as well. The main upside catalyst in my view is the continuation or worsening of port congestion and shipping vessel backlogs. If such congestion and backlog persist, they could cause contract rates to climb up (or at least preventing them from further dropping). The ongoing Russian/Ukraine war and the uncertain COVID situation provide some good causes for such congestion and backlog.

To summarize, ZIM may seem to be a dream stock for value investors. However, it is more likely a value trap in my view. My main argument here is that ZIM spectacular rise during the recent shipping boom is largely due to its concentrated exposure to the transpacific route. The exposure is a double-edged sword, and I am seeing signs that can cause ZIM to fall faster and deeper than its peers in the quarters ahead. The renegotiated rates for its transpacific route are lower, forming a deadly combination with the falling shipping volume too on these lucrative routes. Finally, on the macroscopic side, the SCFI index has contracted by almost fivefold in the past year. And I see plenty of reasons for the contraction to persist given the fluidity of the COVID situation (especially in China), global geopolitical conflicts, and the ongoing inflationary pressure.

Be the first to comment