skodonnell/iStock Unreleased via Getty Images

Overview

Yum China (NYSE:YUMC) stock has rallied to my previous price target based on my initial assumptions, but I think there is still an upside given the current outlook. I believe YUMC is now 15% undervalued. The same-store sales (SSS) during Chinese New Year were especially promising in light of the overall results. Though it’s not conclusive proof of a consumption recovery due to shaky consumer confidence and the possibility of a second wave, it does bode well for FY23 growth. Furthermore, management’s projection of 1,100 to 1,300 net new stores (9 to 10% growth) is consistent with my own growth forecasts. Overall, I see YUMC as one of the best plays for China’s reopening and a long-term hold for growth thanks to its sturdy resilience, strong execution, and dependable management team.

SSS

Overall, KFC’s performance was superior to Pizza Hut (PH) because of an uptick in business at transportation hub locations and better-than-anticipated results in lower-tier cities. However, management is cautiously optimistic about FY23 prospects. While increasing sales is still a top priority for FY23, management plans to increase its average selling price by offering new products at lower and higher price points. Management also plans to take advantage of the reopening theme by reducing the number of promotions offered but increasing their effectiveness in 2023 in order to boost sales and profit margins. Other initiatives include the likes of KFC, which is also launching a high-end wagyu beef burger as part of a broader strategy to increase sales of its premium products across a wider price range.

Store openings

In 2023, YUMC aims to invest between $700 and $900 million in CAPEX and open 1,100 to 1,300 net new stores. KFC and PH both kept their store payback periods at 2 years, and the newest stores were even capable of being profitable in just 3 months. For the benefit of the investors, I’d like to pause here and explain just how crazy a period of three months that involves doubling capital every three months actually is (from a stock investment POV). Moving forward, management intends to maintain a steady and methodical strategy for expanding the store network, all while strengthening the business as a whole. It’s worth noting that 60% of the new stores are located in secondary or tertiary cities, while in primary or tertiary cities, YUMC aims to increase store density with smaller store formats to meet customer needs of delivery convenience.

The KFC brand, in particular, will keep using small format stores to expand into lower-tier cities and boost density in higher-tier cities. As a point of reference, in 2022, smaller-sized KFC restaurants accounted for more than half of all new locations. The plan is to strengthen store resilience while expanding into smaller stores (which already make up about 20% of the portfolio), as they have a faster payback period and are better set up to offer delivery services. I’m glad to see that management is committing more resources to this strategy, which I highlighted as a central plank of YUM’s business model in my initial post. I see no reason why management shouldn’t keep pursuing this strategy for expanding the store count.

Cost inflation

For FY23, management anticipates commodity inflation in the low-single-digit but hopes to keep cost of sales relatively flat. Growth in labor costs is forecast to accelerate to the mid to high single digits from the low single digits in FY22. Although the one-time rental relief of $86 million in FY22 is not likely to be sustained in FY23, management has seen a sustainable improvement in rent due to lower rates and a higher flexible component. In general, I believe the cost concern is being handled satisfactorily, with management having taken some precautions to lessen the blow. However, I agree with management that any cost savings realized here should be re-invested into the business, as expansion is still a priority.

Model update

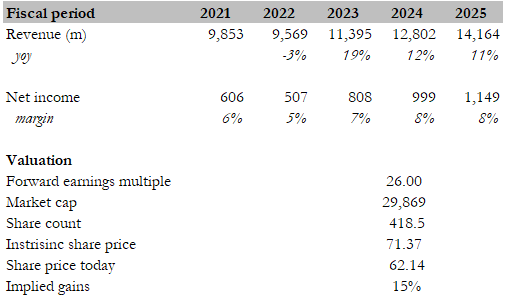

YUMC has performed exactly as expected, with the share price reaching my previous price target. Fundamentally, my investment thesis remains unchanged; I expect YUMC to grow further by capitalizing on multiple tailwinds and successfully executing its growth strategies. Given the updated financials and valuation, I continue to believe there is room for growth. I calculated an intrinsic value of $71.37, or a 15% increase over the current share price ($62.14), using consensus figures through FY25 and a normalized forward PE (currently at 31x, which I believe is too high relative to history).

Author’s estimates

Conclusion

I believe YUMC has significant potential for growth. The strong performance of KFC, especially in lower-tier cities, and the optimistic outlook for same-store sales in the coming year, bode well for growth. Management’s plans to increase the number of stores and improve sales through the introduction of new products and more effective promotions further support this view. In conclusion, my investment thesis remains unchanged, and I see YUMC as a long-term growth play, given its resilience, strong execution, and dependable management team

Be the first to comment