Surendra Sharma/iStock via Getty Images

Investment Thesis

The Invesco S&P 500 Top 50 ETF (NYSEARCA:XLG) provides focused exposure to the largest 50 S&P 500 companies for a 0.20% expense ratio. Essentially, it’s a mega-cap ETF similar to the iShares S&P 100 ETF (OEF) and the Vanguard Mega Cap ETF (MGC). Therefore, the purpose of today’s article is to compare the three funds on a variety of fundamental metrics. XLG is too concentrated, with investors sacrificing a surprising amount of diversification at the company and industry levels. Furthermore, Apple (AAPL) and Microsoft (MSFT), representing 22.59% of the portfolio, have poor EPS Revision Scores, placing the fund at significant risk this earnings season. Therefore, I don’t recommend investors buy XLG, and I look forward to describing why in further detail next.

XLG Overview

Strategy Discussion and Historical Performance

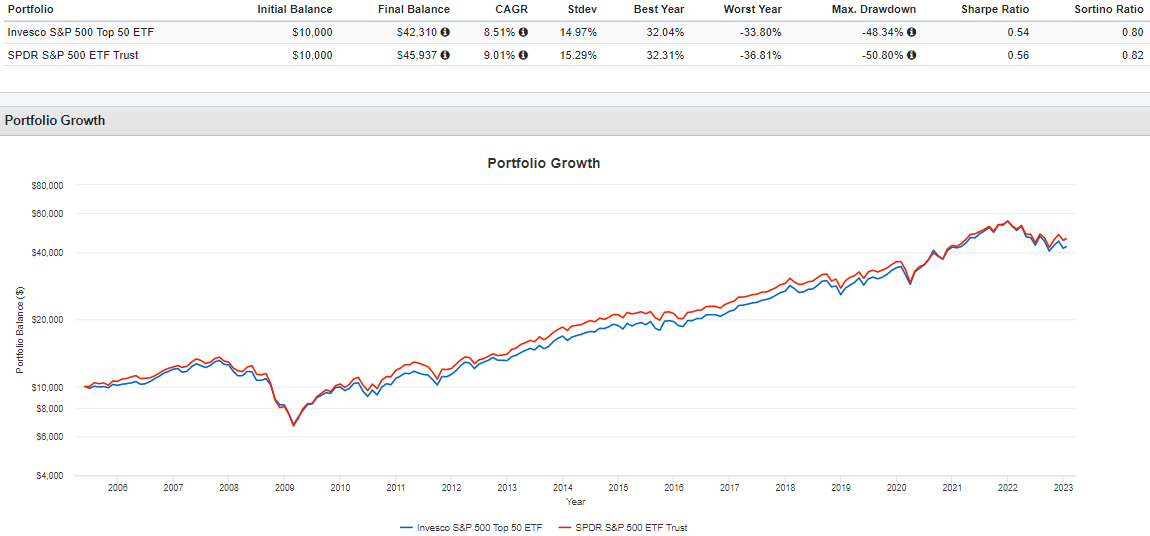

XLG’s straightforwardness is as simple as you’d imagine. It holds the 50 largest companies from the S&P 500 Index and weights based on free-float market capitalization, with reconstitutions occurring annually in June. A 10% buffer rule applies, meaning if current constituents remain in the top 55 at reconstitution time, they still qualify. Other than that, it’s a simple run-of-the-mill Index ETF with a slightly higher 0.20% expense ratio. Is it worth it? Not according to historical returns dating back to May 2005. XLG gained an annualized 8.51% compared to 9.01% for the SPDR S&P 500 ETF (SPY). The one bright spot was a slightly lower drawdown (48.34% vs. 50.80%) during the Great Financial Crisis.

Portfolio Visualizer

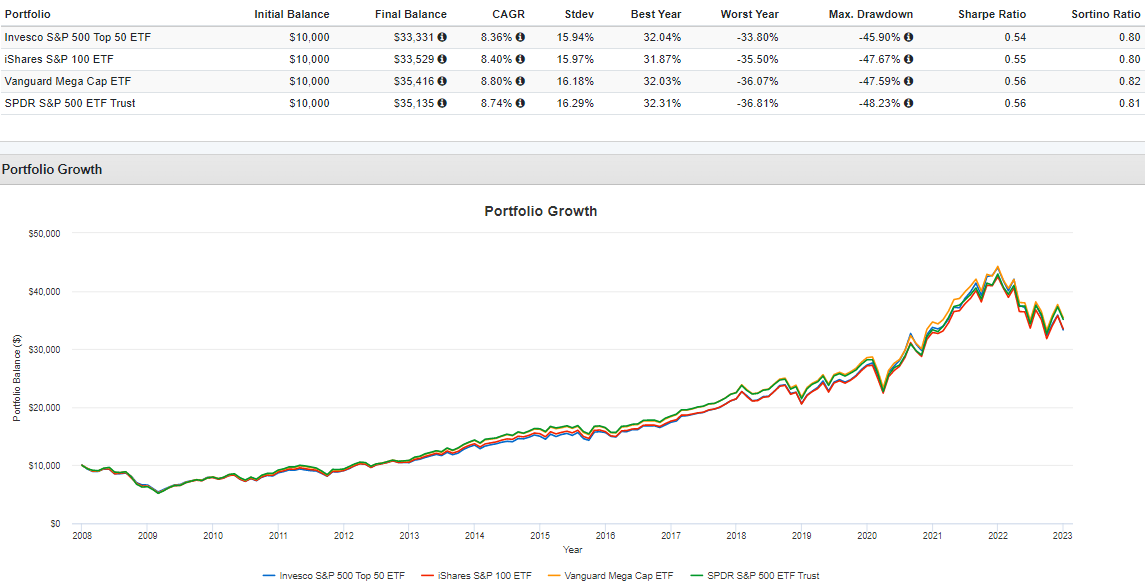

The iShares S&P 100 ETF and the Vanguard Mega Cap ETF are alternatives for investors wanting better diversification. Since January 2008, each outperformed XLG, albeit with slightly higher volatility. It’s possible to own too many stocks, but these results suggest 50 is too few.

Portfolio Visualizer

Sector Exposures and Top Ten Holdings

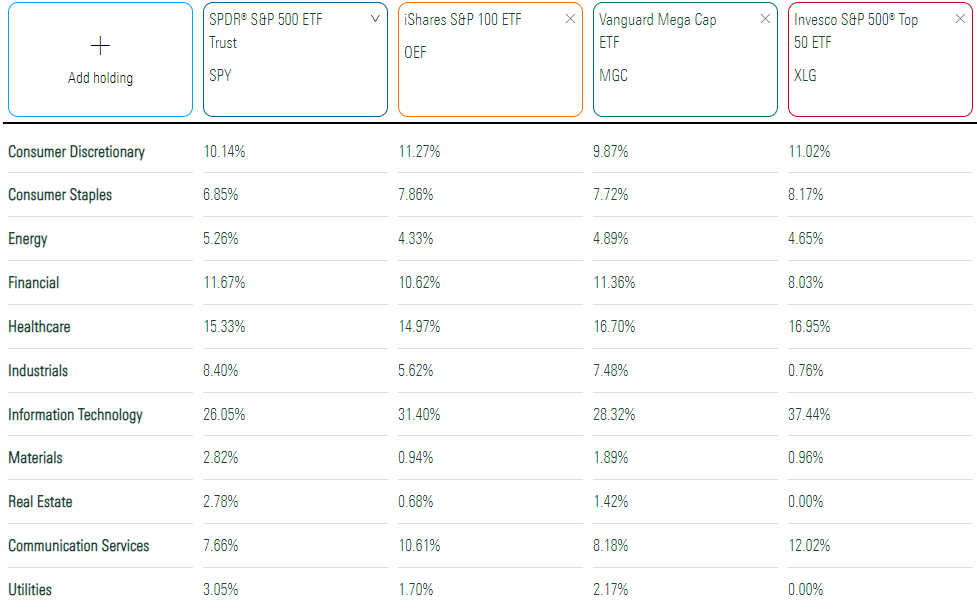

The sector exposures for SPY, OEF, MGC, and XLG are listed below. Technology and Communication Services is where XLG stands out, featuring approximately 11.5% and 4.5% more exposure than SPY. Industrials is the main offset, representing just 0.76% of the portfolio.

Morningstar

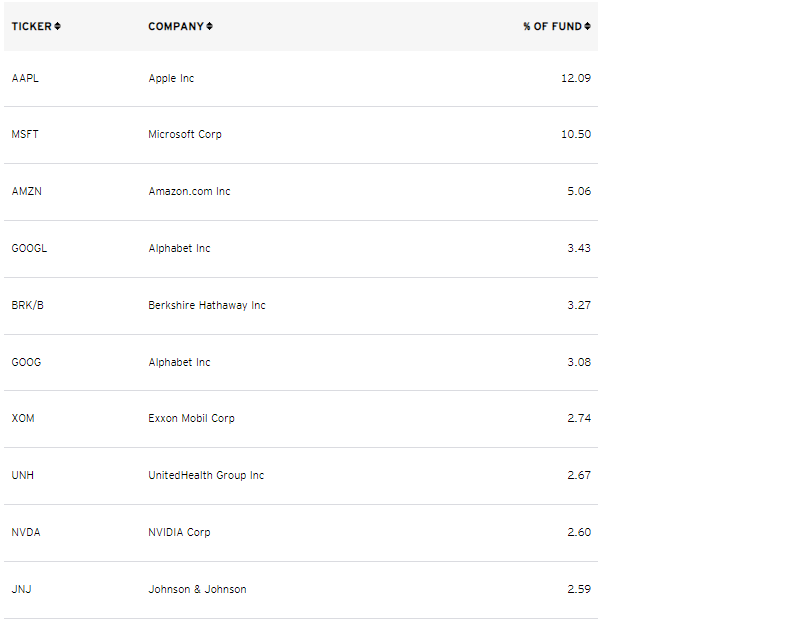

XLG’s top ten holdings are below, representing 48.03% of the ETF. In addition to Apple and Microsoft, Amazon (AMZN) and Alphabet (GOOGL, GOOG), and prominent. These stocks were top performers post-pandemic but declined recently, likely the result of poor earnings results and poor expectations, which I’ll discuss later.

Invesco

XLG Analysis

Diversification Issues: 50 Isn’t Enough

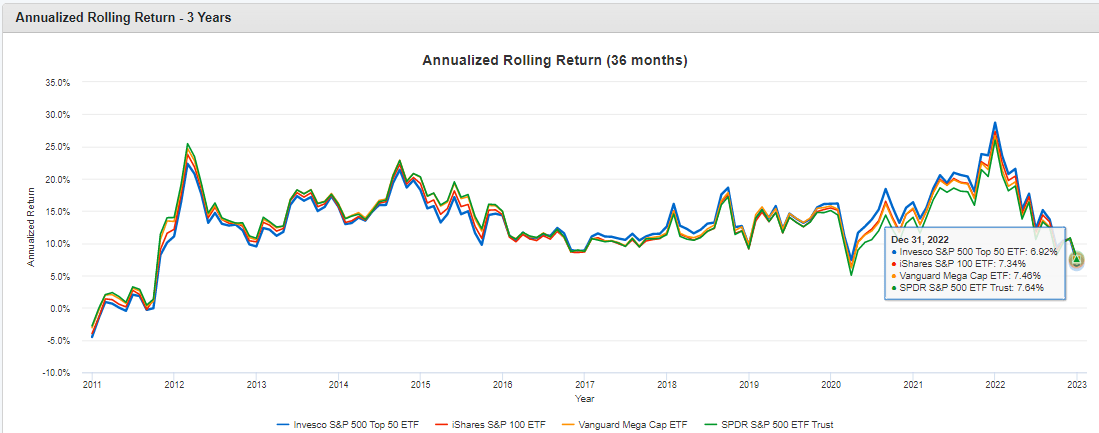

Long-term performance charts suggest 50 stocks is too few. Even for the three years ending December 2022, XLG’s annualized returns were 0.40-0.70% behind OEG, MGC, and SPY. It’s a generous lookback period considering how well mega caps performed in 2020.

Portfolio Visualizer

It’s helpful to consider the industries XLG avoids. Consider these under-allocations compared to SPY, OEF, and MGC:

- Electric Utilities (1.93%, 1.66%, 1.68%)

- Aerospace & Defense (1.79%, 1.91%, 2.10%)

- Oil & Gas Exploration & Production (1.37%, 0.71%, 1.02%)

- Specialized REITs (1.30%, 0.48%, 0.97%)

- Financial Exchanges & Data (1.21%, 0.00%, 0.99%)

- Investment Banking & Brokerages (1.19%, 1.68%, 1.31%)

- Packaged Foods & Meats (0.99%, 0.55%, 0.77%)

- Property & Casualty Insurance (0.95%, 0.00%, 0.89%)

- Health Care Equipment (0.94%, -0.37%, 0.77%)

- Regional Banks (0.94%, 0.00%, 0.45%)

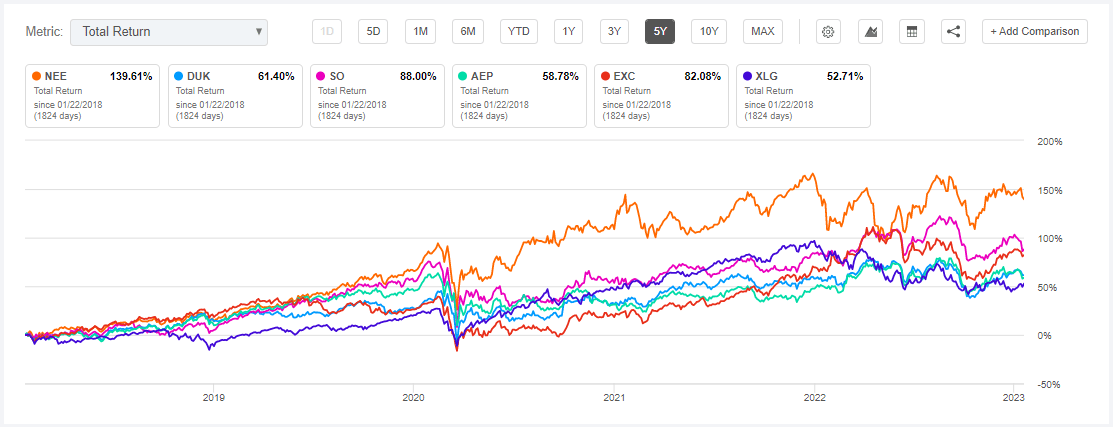

The Electric Utilities industry illustrates why it’s beneficial to have some exposure to some of the smaller companies in the S&P 500. XLG avoids all of them, but here’s how the top five performed over the last five years.

Seeking Alpha

All outperformed XLG, yet only NextEra Energy (NEE) is likely to join XLG when it reconstitutes in June. Duke Energy (DUK) is next in line with a $79 billion market capitalization, the 97th largest in the S&P 500.

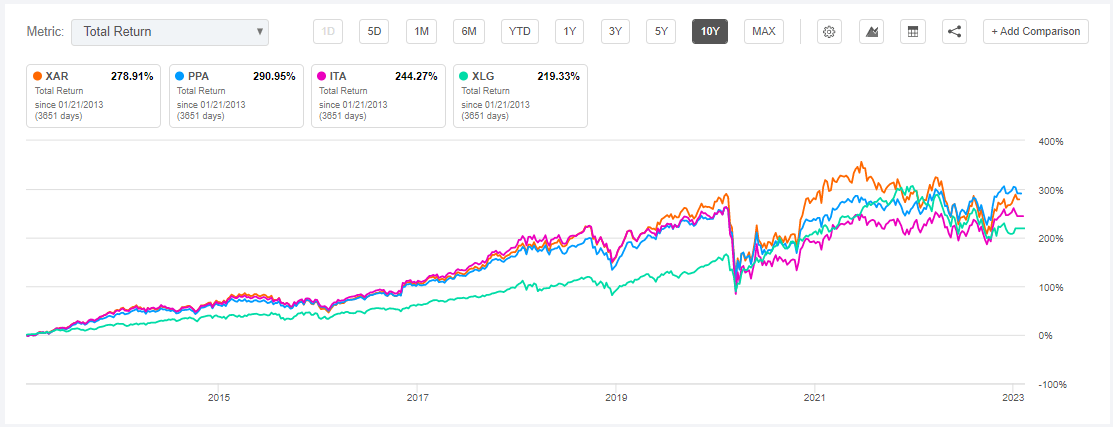

Aerospace & Defense is another industry that XLG avoids but is solid long-term. Although five-year returns were lower, three industry ETFs outperformed XLG over the last ten years. PPA and ITA even gained 10% last year.

Seeking Alpha

The takeaway is that while owning 500 stocks in SPY probably isn’t necessary, 50 is too few. Long-term returns don’t support the strategy, and it’s not worth the higher fee.

Fundamentals By Company

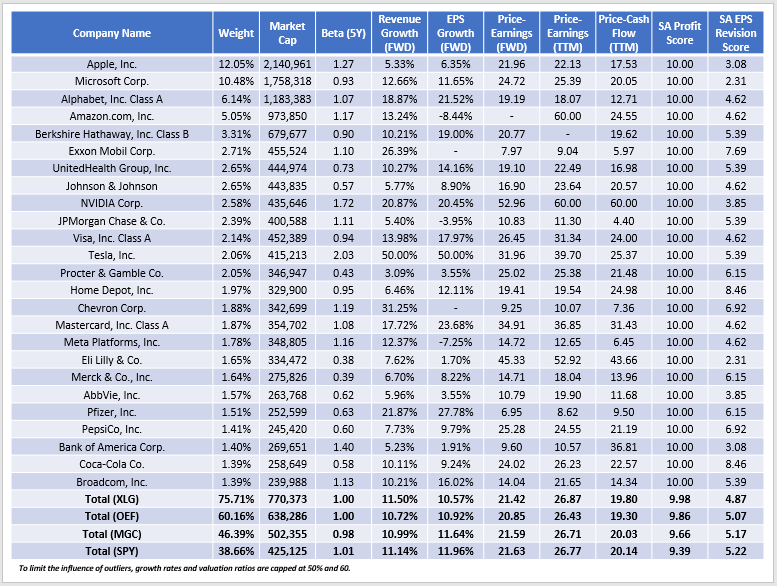

The fundamentals don’t support XLG, either. Consider the following metrics for its top 25 holdings compared to OEF, MGC, and SPY, ordered from most to least concentrated.

The Sunday Investor

XLG has twice as much concentration in its top 25 holdings compared to SPY (75.71% vs. 38.66%), and a $355 billion more market capitalization. The beta for all four ETFs is around 1.00, indicating similar volatility with the overall market, and XLG is arguably the higher-quality fund. Its near-perfect 9.98/10 Profitability Score, derived using company Seeking Alpha Factor Grades, is consistent with a partially efficient market. The most valuable companies are the most profitable, as you’d expect.

However, most comparisons aren’t favorable. XLG’s estimated earnings growth rate is 10.57%, the lowest of the four, and 1.39% behind SPY. There isn’t a valuation edge either – XLG trades at 21.42x forward earnings, slightly more expensive than OEF’s 20.85x. Finally, XLG has the worst EPS Revision Score (4.87/10), primarily due to Apple and Microsoft’s “D+” and “F” Grades.

Seeking Alpha

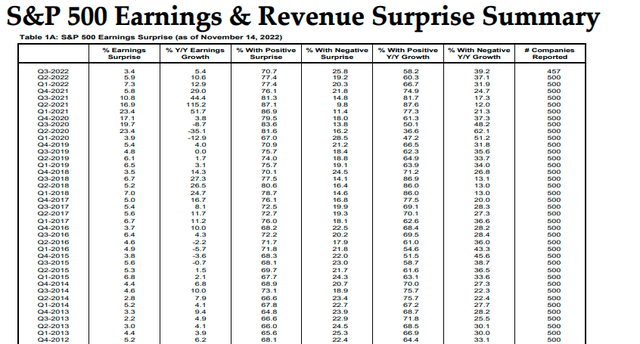

Each barely beat earnings estimates last quarter. The result was a poor 3.40% aggregate earnings surprise for the S&P 500 Index, the lowest in a decade. It’s only prudent to overweight these underperforming stocks when there is a clear sign of a turnaround. That hasn’t happened yet.

Yardeni Research

Investment Recommendation

There are two reasons why I don’t recommend XLG. First, its historical returns suggest 50 stocks is too few. Mega-cap alternatives like OEF and MGC are better diversified while still providing a focused portfolio. Second, XLG overweights companies with weak earnings momentum without offering any meaningful benefits in growth and valuation. Mega-caps may surprise to the upside this earnings season, but it’s not worth the additional risk in case they don’t. Thank you for reading, and I look forward to the discussion in the comments section below.

Be the first to comment