MasaoTaira

With a positive total return of ~5%, Whitestone (NYSE:WSR) shares have outperformed the broader REIT market over the past year. The company has made some positive changes to its corporate governance (discussed below) and is benefiting from strong leasing conditions in its sunbelt shopping center portfolio.

While Whitestone does carry a greater risk profile than its larger shopping center peers (discussed below), with a total cap below $1.2 billion and trading at an implied cap rate of over 8%, the company could be a buyout candidate. In my estimation, shares could have 40% upside potential.

What’s to Like About Whitestone?

Sunbelt pureplay

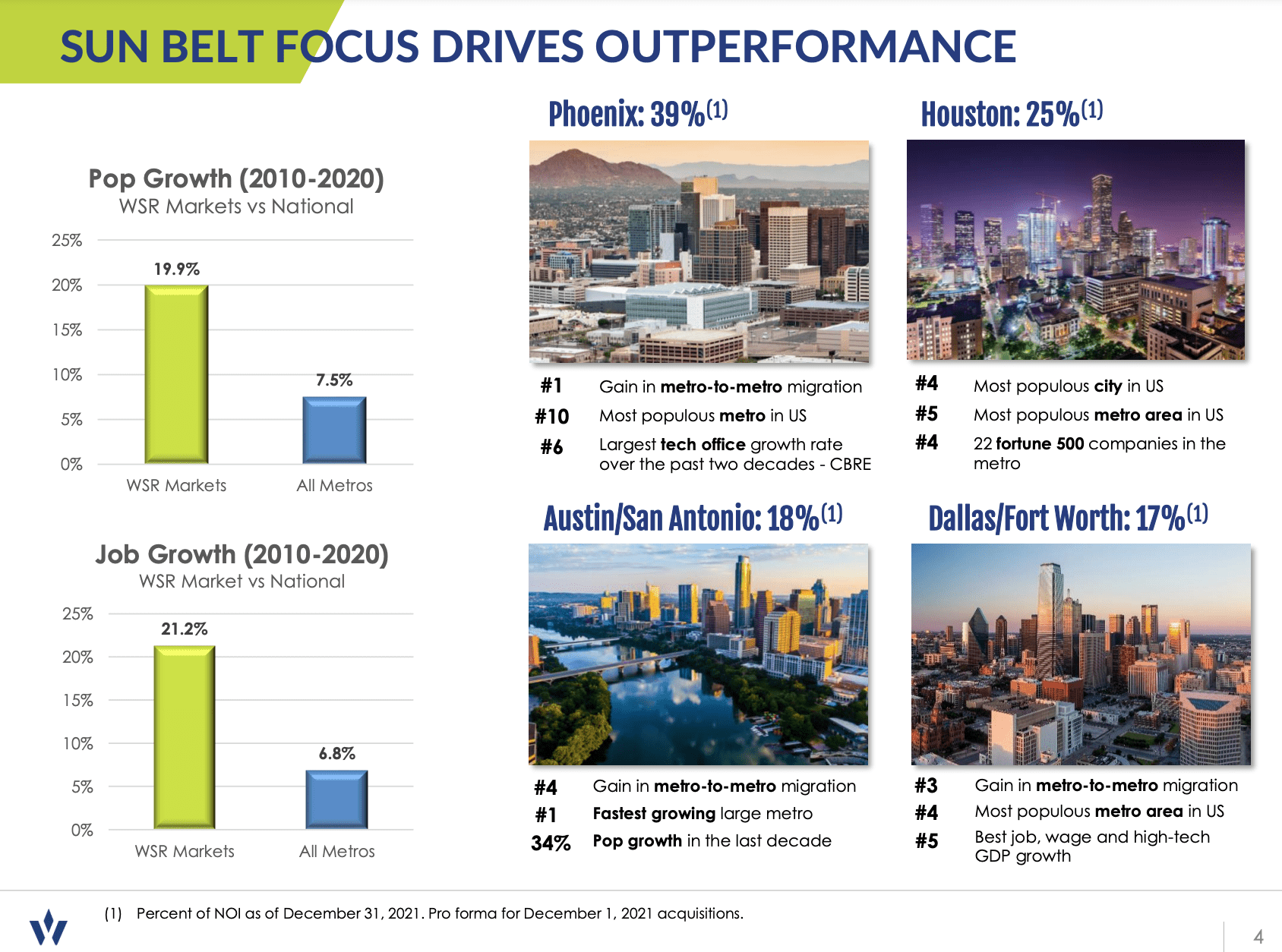

NOI by market (Investor Presentation)

As shown above, Whitestone’s portfolio is a pure-play on four sunbelt markets – all of which have and are expected to continue to experience population and job growth in excess of the national average.

Strong Current Results

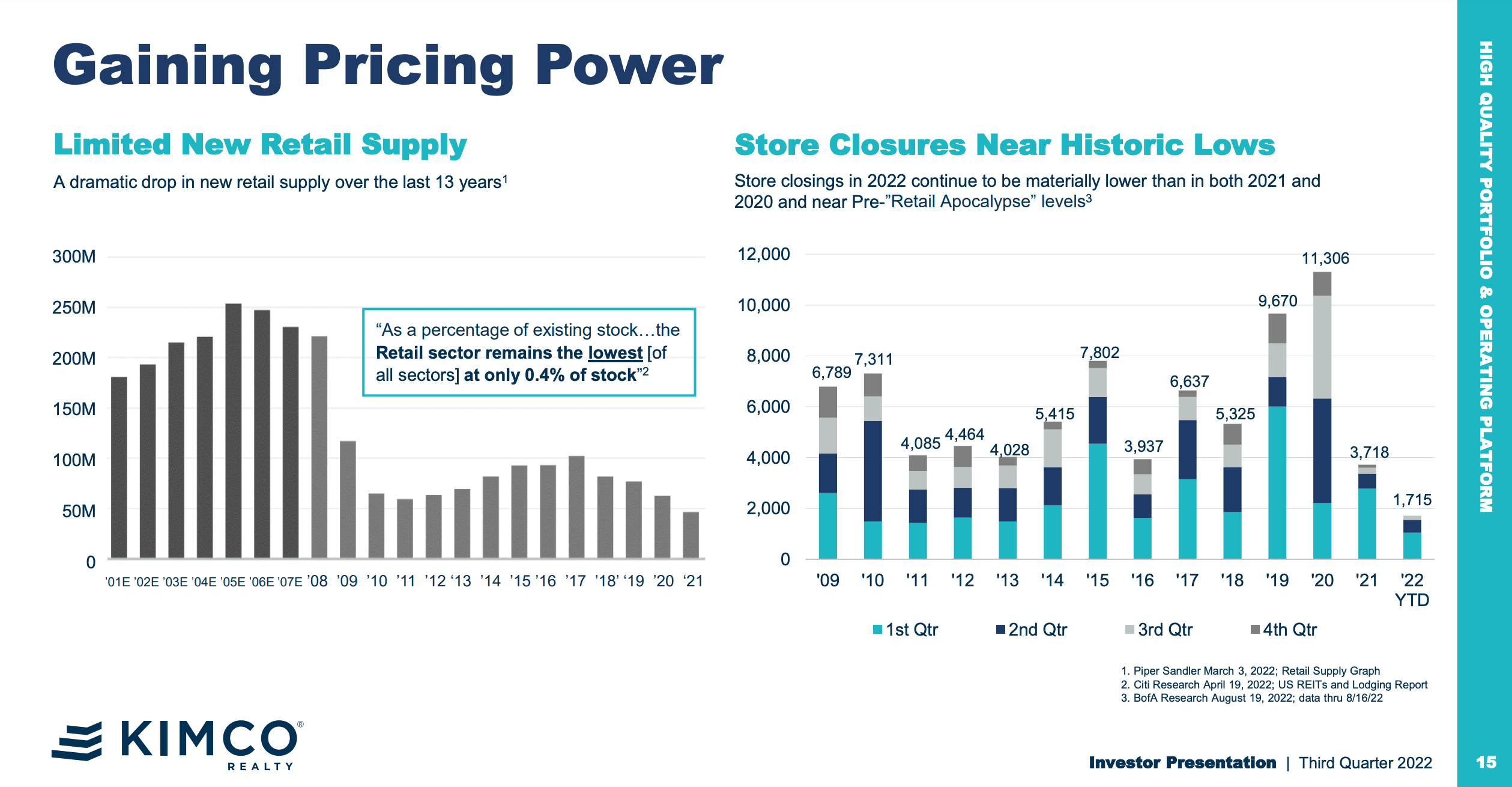

Shopping centers have experienced a bit of a renaissance in recent years as retailer store openings are in excess of store closings (a reversal of what we saw from 2017-2020). Coupled with relatively limited increases in new supply (shown below), this has improved pricing power for shopping center landlords which has caused improvement in leasing spreads.

New Shopping Center Supply over Time (Kimco Investor Presentation)

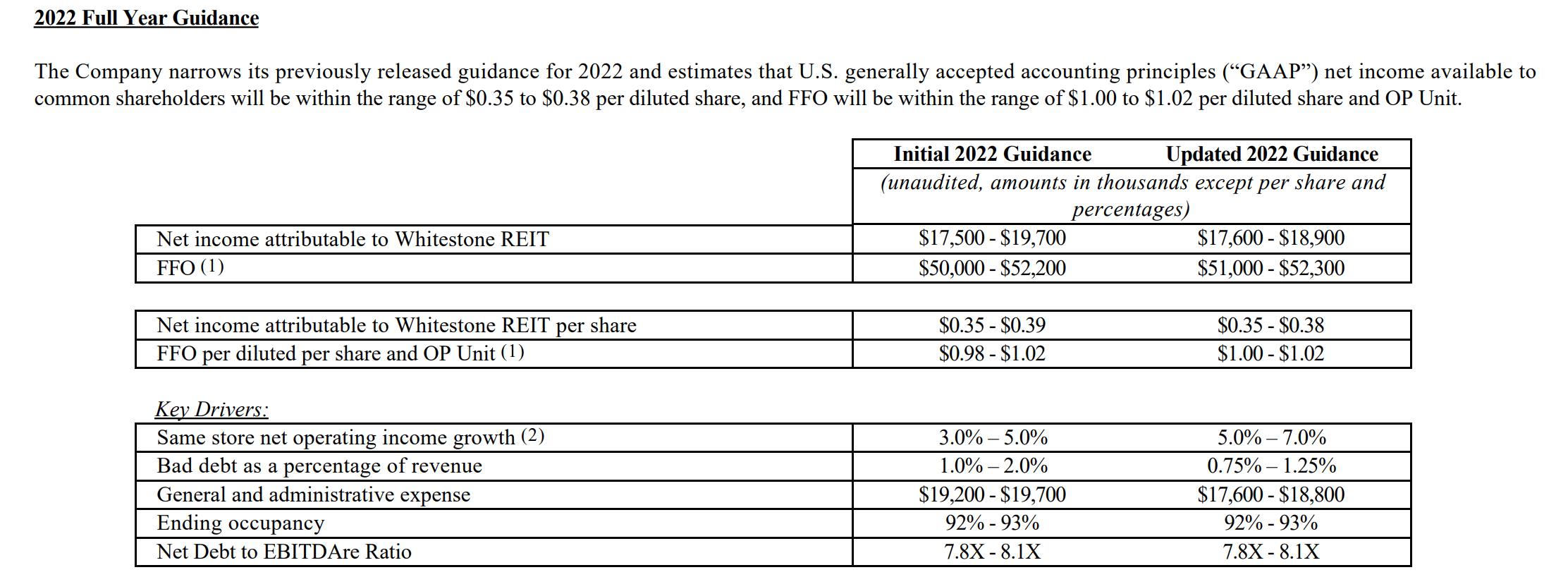

As shown below, the strong leasing environment has allowed Whitestone to increase its expected same store NOI growth as tenant demand has remained strong as the year progressed.

Whitestone 2022 Guidance (Whitestone 3Q22 Quarterly Supplemental)

Improved overhead – Early in 2022, Whitestone dismissed its highly compensated former CEO. New management appears to have a sharper focus on overhead costs. Overall G&A expenses are on track to be ~$4 million lower (20%) year-over-year in 2022.

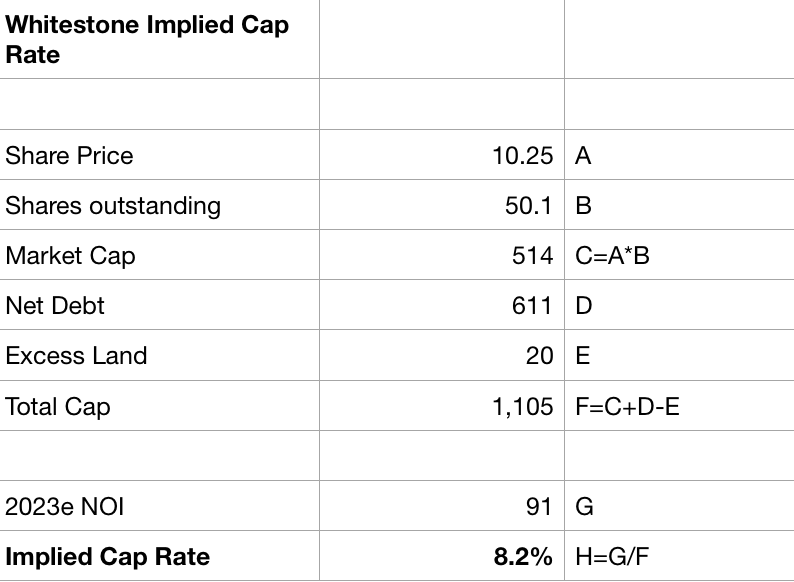

Valuation – As shown below, Whitestone trades at an implied cap rate just north of 8% which is at the high end (lowest valuation) amongst shopping center REITs (implied cap rates for the sub-sector range from 6.5-8%).

Whitestone Implied Cap Rate (Company Filings; Author Estimates)

Assuming a 7% cap rate, implies an NAV (net asset value) of $14 per share for Whitestone suggesting nearly 40% upside to its current share price.

Potential buyout candidate – In conjunction with the departure of its former CEO, Whitestone terminated its ‘Poison Pill’ in early 2022. Coupled with its relatively small size (sub $1.2 billion total cap), attractive valuation, and sunbelt-only focus, this makes Whitestone a potential takeover candidate.

Concerns I have about Whitestone

Sub-scale/ High G&A burden– while overhead expenses have been reduced following the departure of former CEO, Whitestone’s G&A-to-NOI ratio of 20% is higher than its larger, more efficient shopping center peers which have G&A-to-NOI ratios in the 13-17% range.

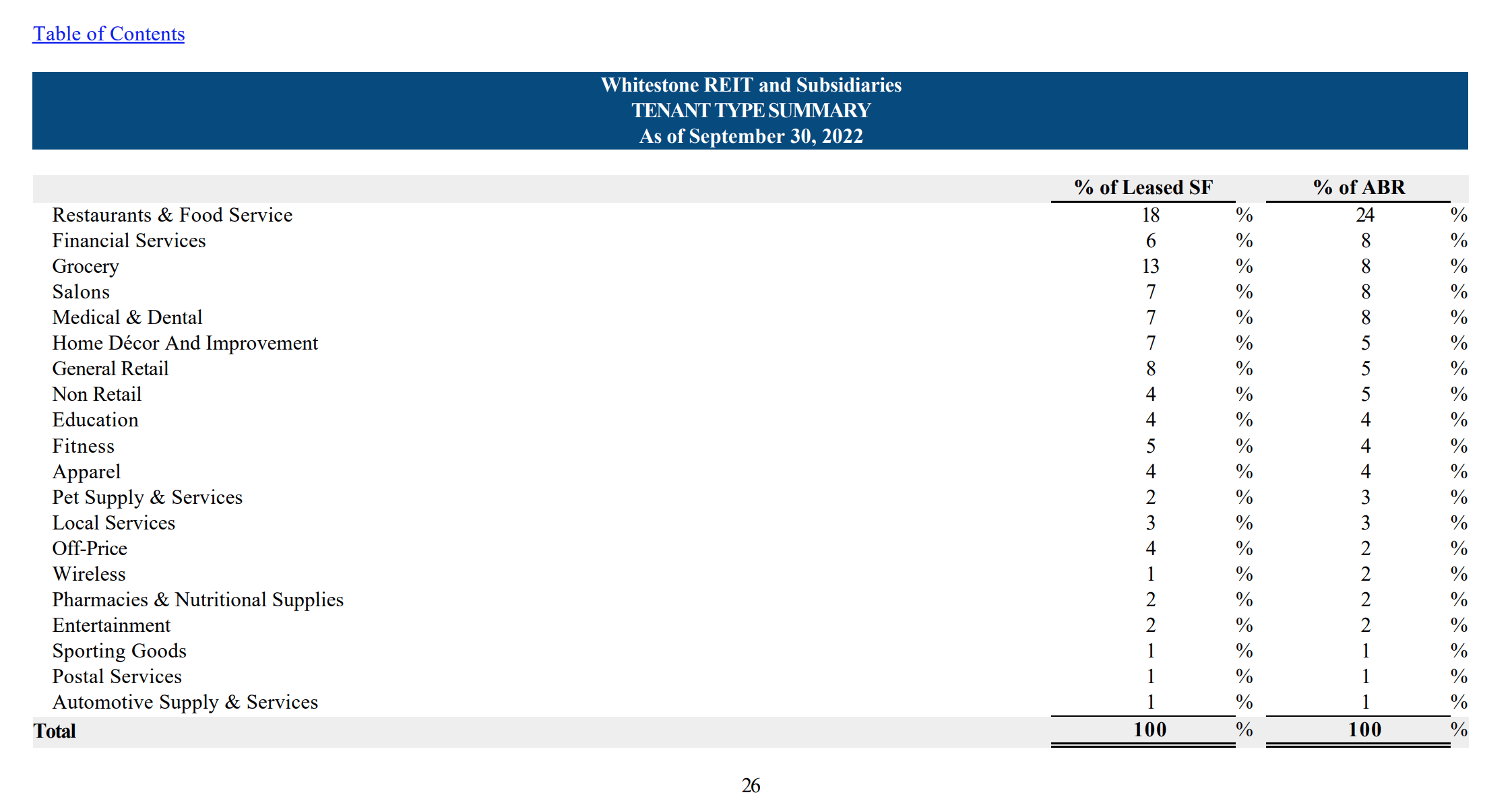

Significant exposure to restaurant tenants– As shown below, Whitestone has significant exposure to restaurant tenants. Similarly, Whitestone has less grocery exposure and less exposure to more creditworthy national tenants/investment grade tenants than its larger shopping center peers. I believe that this makes Whitestone more vulnerable to an economic downturn than its peers whose tenants have greater financial resources to make rent payments in a recession.

Tenant Summary (Whitestone 3Q22 Quarterly Supplemental)

Shorter leases – Relative to shopping center peers, Whitestone has a shorter average lease duration (3.9 years vs. average of 5.2 years for peers). While this has benefited Whitestone as it has allowed more frequent re-pricing as leasing spreads have risen, in a downturn this could result in higher vacancy levels (currently 92.5% occupied).

High leverage – with net debt to EBITDA of ~8x, Whitestone is more leveraged than shopping center peers (range from 5-6x). Coupled with shorter lease duration and fewer investment grade tenants, this suggests greater downside risk in a severe recession.

Conclusion

Whitestone is a case of higher risk, higher potential return than its shopping center peers. At this time, I have no position in the shares but would likely begin a position should shares fall 10-15%. Given Whitestone’s greater risk profile, I require a somewhat larger (40% in this case) discount than usual (I typically buy at a 30% discount to my fair value estimate).

Be the first to comment