georgeclerk

Thesis

Amazon (NASDAQ:AMZN) has sold off largely for good reasons, as it’s struggled to generate growth while cash flow turned negative. If Amazon can turn things around, it still has huge potential and could nearly match its return of 900% in the last 10 years. But there are substantial risks that could lead to a lost decade for Amazon shareholders in my bear case. The actual returns are likely to be somewhere in the middle, which makes Amazon a buy, albeit not a very strong one at this point.

Negative Cash Flow And Slowing Growth

It’s been difficult to be an Amazon shareholder recently, as the stock is down over 30% year to date and recently fell below its pre-COVID high set over two years ago. That fall comes even as Amazon’s P/E ratio compressed from over 250 in 2017 to 55 today.

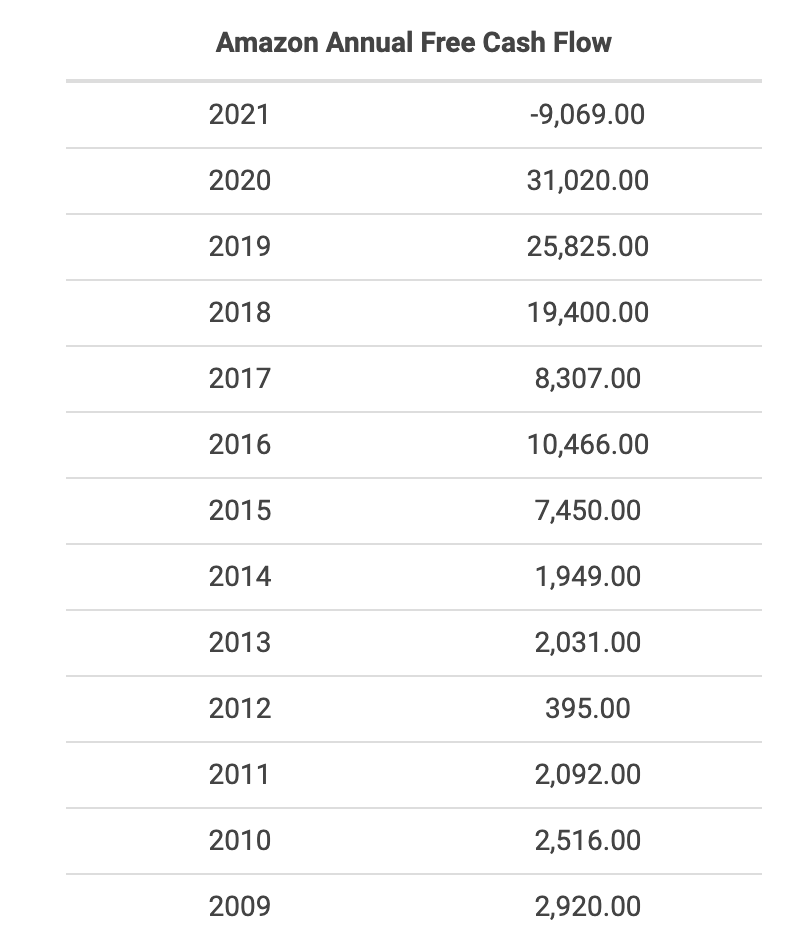

To understand why the selloff happened, look no further than the free cash flow metric, which went negative in 2021 for the first time in over a decade.

MacroTrends

This annualized table smooths over some bumps; Amazon actually posted negative free cash flow in 65% of quarters since 2009. The annual cash flow has been positive in all years prior to 2021 because Amazon typically has strong cash flow in Q4 of each year. However, with a strong Q4 absent in 2021, Amazon has now posted five consecutive quarters of negative free cash flow.

MacroTrends

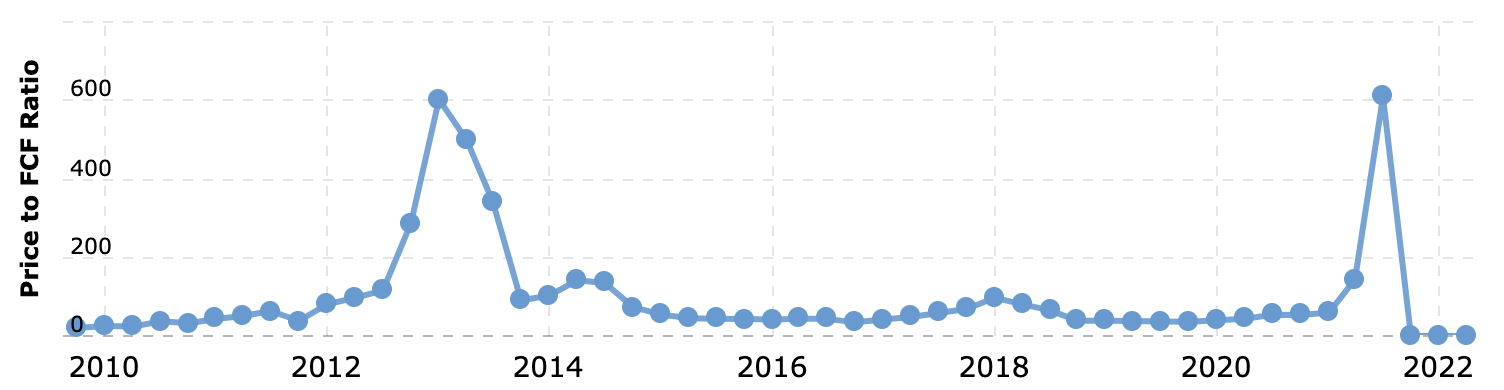

Because Amazon has never looked cheap by the traditional P/E metric, its management has often encouraged investors to look at P/FCF instead. By that metric, Amazon usually looked reasonably valued, as it traded below 60 P/FCF for most of the 2015-2020 period. Now that cash flow has turned negative, P/FCF is essentially meaningless and doesn’t make Amazon attractive at the current valuation.

MacroTrends

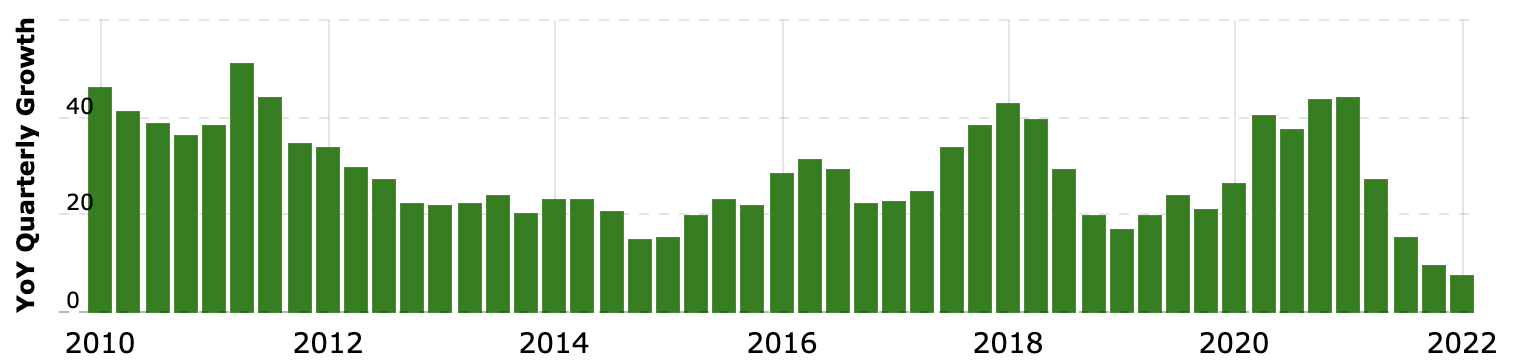

In the past, investors could overlook a high P/E partly because Amazon had strong revenue growth. However, growth has been in the single digits for two consecutive quarters. Those are the only quarters of single digit revenue growth since 2010. This slowing growth is another big reason for the selloff.

The Bigger Picture

Although the current growth and valuation metrics look bleak for Amazon, long term investors should consider where Amazon will be in 10 years or longer, not where it is today. According to Seeking Alpha, analysts project an 11% revenue CAGR and 42% EPS CAGR through 2031. That represents a substantial acceleration from the current growth rates, and would give Amazon a P/E of 8 in 2031 if the massive EPS growth comes to fruition.

For some comparison, Microsoft (MSFT) has an expected forward P/E of 10 in 2031, while Walmart (WMT) is at 9 and Apple (AAPL) is at 8. This means that despite the currently high P/E and negative cash flow, analysts view Amazon as fairly valued for the long term relative to other big tech and retail peers.

The Bull Case

Rather than using analysts’ estimates, I prefer to generate my own. In the bull case, analysts’ estimates from the previous section for massive EPS growth may actually be too conservative.

The overall cloud industry is expected to grow somewhere between 20% and 30% through 2026 (sources: 1, 2, 3). As the leader in the industry, AWS has typically grown faster than industry growth forecasts, especially when it comes to EPS growth. But that benefit may be offset by further growth deceleration between 2026 and 2031. If we take the average and project AWS to experience 25% operating profit CAGR for the next decade, that means AWS would generate $173 billion in operating income in 10 years. At its current share price, that would give AMZN stock a 10 year forward P/E of 7 from AWS profits alone.

Unfortunately, the other major segment (e-commerce) is currently detracting from income, as the segment posted an operating loss in the most recent quarter. That’s unlikely to continue forever, as the segment was profitable in 2021 and competitors like Walmart and Target (TGT) are consistently profitable. In the long term, e-commerce still has a lot of room to grow, as in the bull case nearly all transactions could be facilitated by e-commerce compared to less than 30% today. If we forecast an 11% revenue CAGR for Amazon’s e-commerce business and terminal profit margin of 5% (in between where Walmart and Target are today), that would allow the e-commerce business to contribute $58 billion in operating income in 10 years.

Taking the two segments together, that puts Amazon’s 10 year forward P/E at just 5. And that’s not even accounting for other bets with significant potential like advertising. If about 20% of profits come from these other bets in 10 years, that could bring the forward P/E down to 4.

Today, commerce and big tech peers trade in a wide P/E range, with Target (12 P/E) at the low end and Costco (41 P/E) at the high end. Even conservatively assuming that Amazon eventually trades as low as 12 P/E, in the bull case it could still approximately triple in the next 10 years. With a higher terminal P/E, it could even grow 5x or more.

The Bear Case

Microsoft famously struggled after Steve Ballmer became CEO in 2000, but turned around after appointing Satya Nadella as CEO in 2014. Although many factors contributed to Microsoft’s performance over 20 years, it’s one of many examples of companies that struggled after their visionary founder stepped down.

While Jeff Bezos made industry dominance and the growth that comes with it look easy, I can’t help but wonder if Amazon’s recent struggles should be at least partially attributed to new CEO Andy Jassy. With Jassy’s expertise being in AWS, I wouldn’t be surprised to see the e-commerce business continue to struggle against founder-led competitors around the world like Shopify (SHOP), MercadoLibre (MELI), JD.com (JD), and Sea Limited (SE).

Amazon faces increasingly competitive offerings locally too, especially from Walmart. AWS also faces significant competition, as it has been growing slower than Azure and GCP for years now.

Amazon is still a giant and isn’t going anywhere. But I think there is potential for a lost decade similar to what Microsoft experienced from 2000-2014. My bear case estimates are for AWS to grow profits at just a 13% CAGR, while the e-commerce business grows at a 6% CAGR with just 1% terminal profit margin. That would give Amazon just $70B in operating income in 10 years, which means that Amazon stock would have the same price in 10 years as it does today if it had a terminal P/E of about 17. I think this P/E is reasonable – perhaps even too high – for a cyclical company with low margins.

This result would be similar to what happened to Microsoft in its lost decade, where it did grow revenue significantly but also experienced significant multiple compression.

Conclusion

I see a wide range of possible outcomes for Amazon stock over the next 10 years, ranging from a slightly negative return to a gain of more than 5x. The key question that will determine the actual outcome is whether Amazon can continue to assert dominance over the fast growing e-commerce and cloud computing industries.

At this point, I haven’t seen enough from Amazon’s new leadership to feel confident that its market position in 10 years will be as strong as it is today. After a year or so of strong results, I’d feel more confident about the bull case.

Nevertheless, I expect that even in an average case, strong industry growth will propel Amazon stock to a positive return. The price target that I shared with members of Tech Investing Edge is $159, which implies 40% upside to fair value. Based on that price target I expect Amazon to return 200-300% this decade. This would be a solid return, which makes Amazon a buy.

However, I believe that some of Amazon’s big tech peers have similar total return potential with less potential for a lost decade. Thus, I prefer to own other big tech companies at this point, especially since I already have significant exposure to Amazon through indexes.

Be the first to comment