jetcityimage

ChargePoint Holdings, Inc. (NYSE:CHPT) investors who capitalized on its December lows have made an excellent start to 2023, as it recovered nearly 60% toward its highs last week.

We assessed that its upward reversal would likely take a pause, given its marked recovery. Our previous speculative buy thesis was invalidated and would have triggered stop-loss risk management if we had added it. But a re-entry Buy signal appeared at the end of December. Savvy investors who picked those lows have been duly rewarded.

Therefore, the critical question is whether the current buy levels still represent a reasonable entry point for investors?

We will address that subsequently, but we believe it’s crucial to first discuss the recent acquisition of Volta (VLTA) by Shell USA (SHEL) for $169M, or $0.86 per share.

It has been a complete disaster for VLTA holders since its post-IPO highs of $14.30 in September 2021. Accordingly, VLTA had lost nearly 98% from those highs, as investors bailed out before the Shell acquisition offer took it back to $0.86.

As such, the market likely expects the merger to go through successfully, which is expected to close in H1’23.

But why did Shell decide to acquire Volta, and is it in line with its EV charging strategy? We believe the incredible collapse in Volta’s acquisition has likely driven Shell to leverage Volta’s existing infrastructure with the record profits from its downstream business over the past two years.

Shell “is reimagining the filling station as a place with coffee, snacks, and space to hang out while recharging the car. As such, it’s Volta’s “dual charging and media network” strategy that is in line with Shell’s vision.

Accordingly, Volta intends to “use its charging stations as a tool for attracting shoppers and diners to locations like shopping malls, restaurants, and grocery stores.” Hence, its charging network needs to be located in critical transport arteries. With Shell’s highly extensive network of “46K stations in 80 countries,” the combination makes sense for Shell.

It also makes sense for Volta, as the company is not expected to turn a profit through 2027, and running down its cash reserves, including repeating a going-concern warning in May.

Therefore, Shell likely sensed a timely opportunity to absorb Volta into its ranks as it looks to leverage the fast-expanding EV charging market.

What does it mean to ChargePoint? It depends on whether you are an optimist or pessimist. The EV charging market is still expected to reach $100B in investments in 2023, up from last year’s $62B. However, China remains the dominant market, accounting for more than 60% of public chargers.

The optimist will likely see ChargePoint operating in a massive market and scaling quickly, supporting EV adoption. Note that EVs accounted for just 10% of the global market share, with the penetration in the US amounting to just under 6% in 2022.

Hence, ChargePoint still has significant opportunities to leverage as it continues on its path toward profitability, as discussed in our previous article.

What makes ChargePoint so different? Keen investors should recall that ChargePoint operates an asset-light model. As such, it does not need to commit significant CapEx to build its charging networks. Instead, its customers and partners will leverage ChargePoint’s hardware and software solutions to develop their infrastructure.

Case in point. In early January, Mercedes-Benz (OTCPK:MBGAF) announced a partnership with ChargePoint and MN8 Energy to “launch 10,000 high-power electric vehicle charging points in the US, Europe, and China.”

Accordingly, the network is expected to cost about $1.05B, with the costs shared between Mercedes and MN8, leveraging ChargePoint’s Express Plus DC fast-charging technology for the charging hubs.

So ChargePoint provides the solutions but does not need to foot the bill for the CapEx. That has helped the company avoid the intensive CapEx load of its peers. Instead, the company focuses on improving its hardware and software solutions, enhancing the value proposition for its customers and partners.

| Name | NTM EV/REV | NTM EV/EBITDA | NTM P/E |

|---|---|---|---|

| ChargePoint | 5.57x | (18.80x) | (19.29x) |

| Wallbox (WBX) | 3.06x | (24.13x) | (10.06x) |

| Blink Charging (BLNK) | 7.31x | (9.84x) | (8.65x) |

| Tritium DCFC (DCFC) | – | – | (2.23x) |

| Beam Global (BEEM) | 4.48x | (21.24x) | (16.40x) |

| Nuvve Holding (NVVE) | 1.70x | (0.69x) | (1.14x) |

CHPT valuation metrics with peers. Source: S&P Cap IQ

Notwithstanding, note that the leading pure-play EV charging players are not profitable. Hence, investors must demand a generous margin of safety and be disciplined with capital allocation, as traditional valuation metrics are likely ineffective.

Also, any opportunity in CHPT should also be considered speculative, as it’s still early in its ramp cadence.

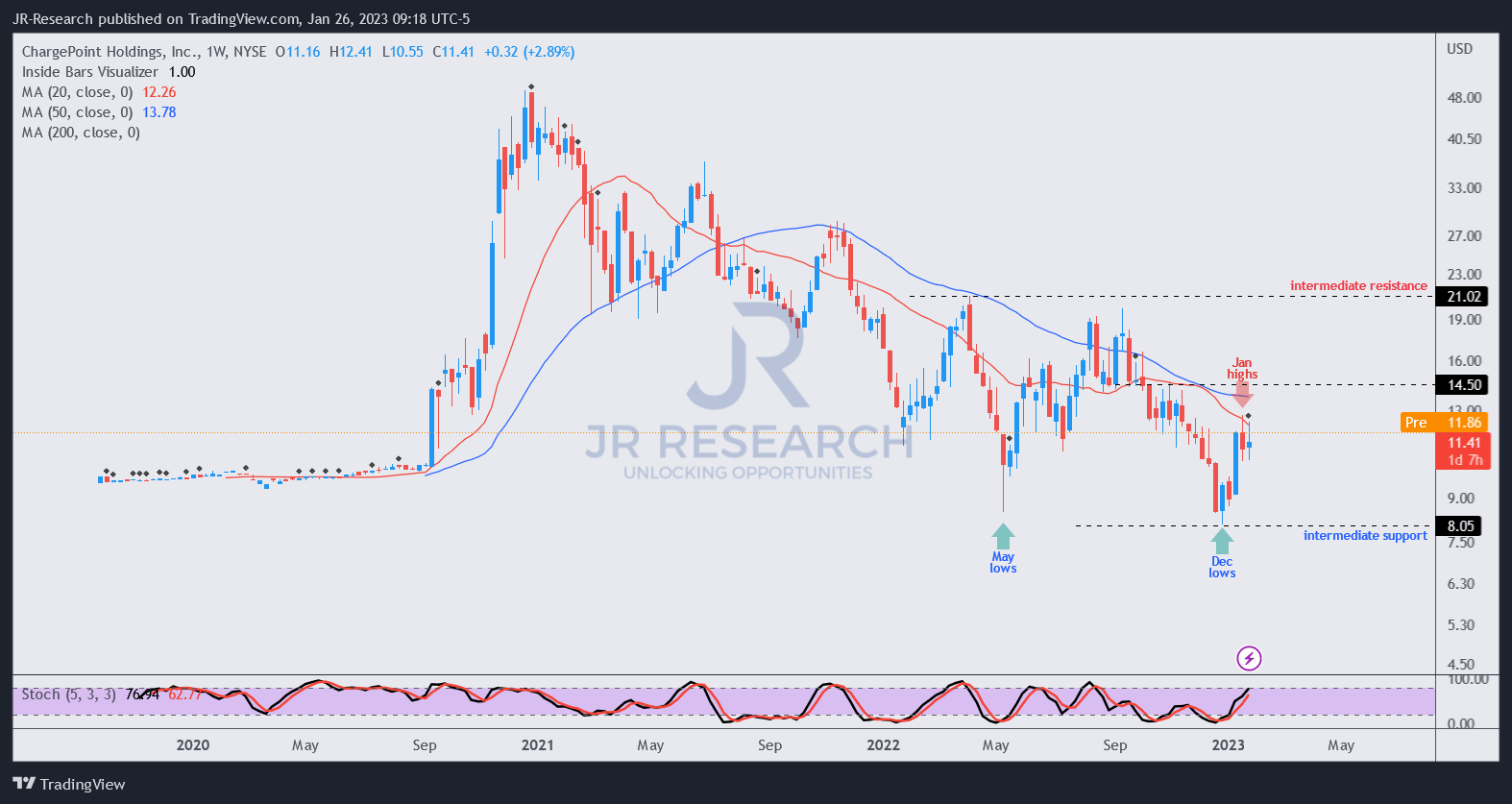

CHPT price chart (weekly) (TradingView)

We previously anticipated CHPT’s May lows to hold robustly. However, it was initially invalidated in the selloff to form its end-December lows.

Despite that, it proved to be an astute bullish reversal price action that likely took out the dip buyers in May.

With CHPT still in a medium-term downtrend, as seen above, investors need to know whether the current recovery can be sustained.

We think CHPT could be in the early stages of a bullish recovery but expect near-term downside volatility, given the sharp recovery.

Therefore, more conservative investors can consider adding after seeing more constructive consolidation.

Rating: Speculative Buy (Reiterated).

Note: As with our cautious/speculative ratings, investors must consider appropriate risk management strategies, including pre-defined stop-loss/profit-taking targets, within an appropriate risk exposure.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment