GOCMEN/iStock via Getty Images![]()

Introduction

When last discussing Western Midstream Partners (NYSE:WES), my previous article highlighted that a very high 12% distribution yield could be coming soon as they move towards rolling out their enhanced distributions. Although at the time, they were still lacking one of the elements that had to be fulfilled to see these rolled out but thankfully, this is no longer the case and thus my eyes are on their distributions next month when they released their upcoming results for the fourth quarter of 2022.

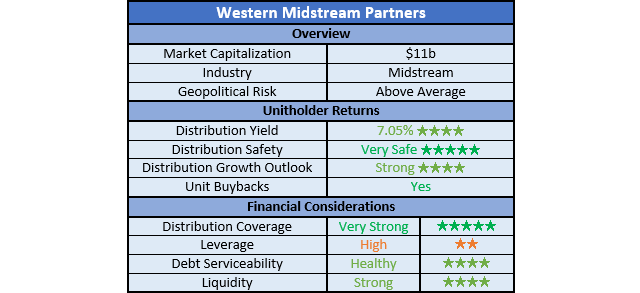

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

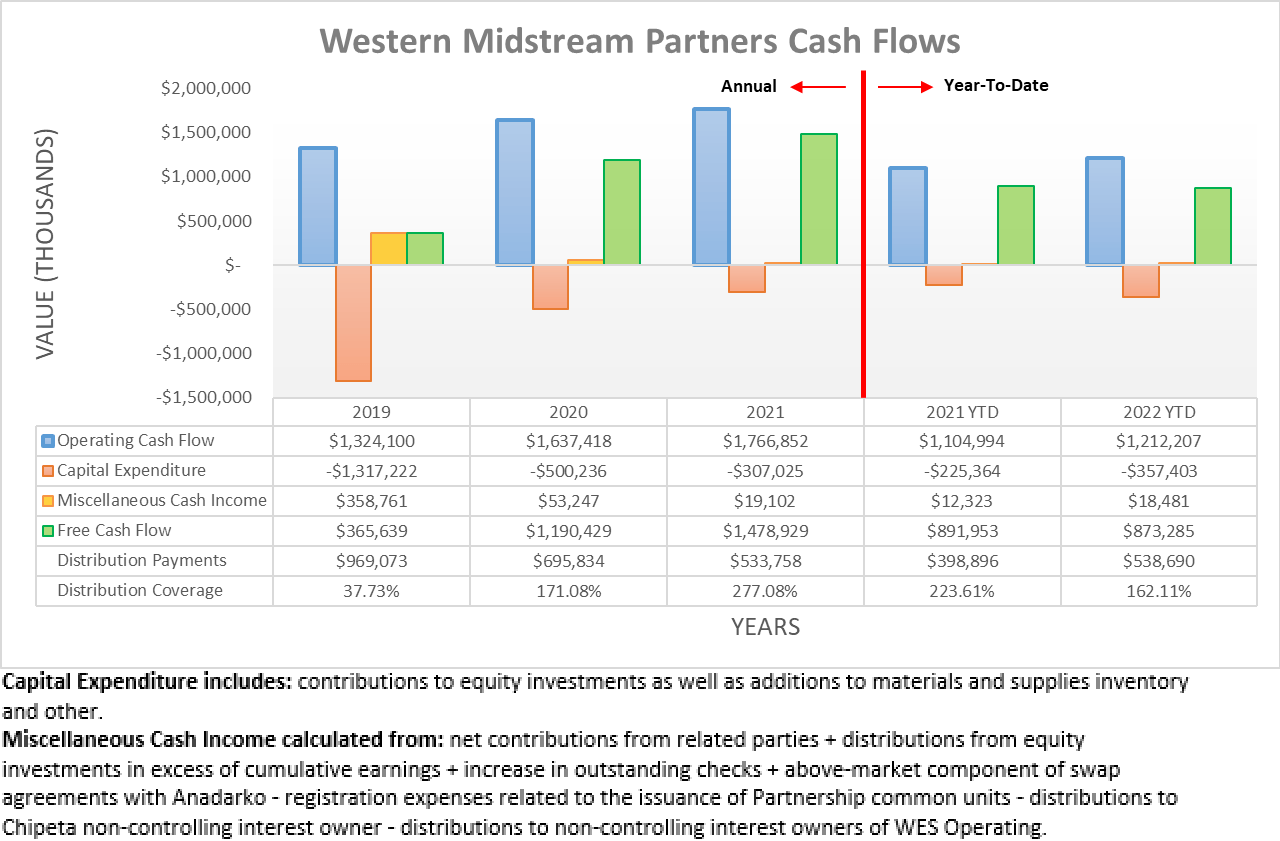

After enjoying strong cash flow performance during the first half of 2022, it was positive to see this continue into the third quarter with their operating cash flow climbing to $1.212b during the first nine months and thus now almost 10% higher year-on-year versus their previous result of $1.105b during the first nine months of 2021. Equally as important, this actually marks an acceleration from the first half of 2022 that at the time, saw its results only ahead circa 4% year-on-year, which creates a favorable backdrop heading into their upcoming fourth quarter of 2022 results, plus further afield into 2023.

Author

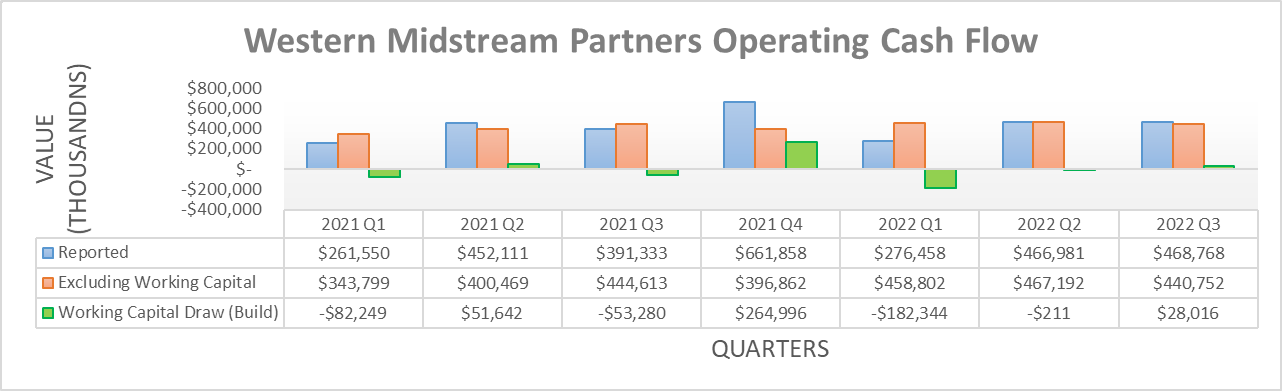

When viewed on a quarterly basis, the same story broadly continues regarding the third quarter of 2022 that only saw a relatively minor working capital draw of $28m. When combined with their modest capital expenditure during the first nine months, they managed to generate ample free cash flow of $873.3m that provided strong distribution coverage of 162.11% against their corresponding payments of $538.7m. That said, if excluding their working capital build of $182.3m during the first quarter along with their relatively minor build of $0.2m and draw of $28m during the second and third quarters respectively, it lifts their underlying free cash flow even higher to $1.027b. This sees the capacity for very strong distribution coverage of almost 200% that as a result, helps pave the way for their enhanced distributions.

Western Midstream Partners Third Quarter Of 2022 Results Presentation

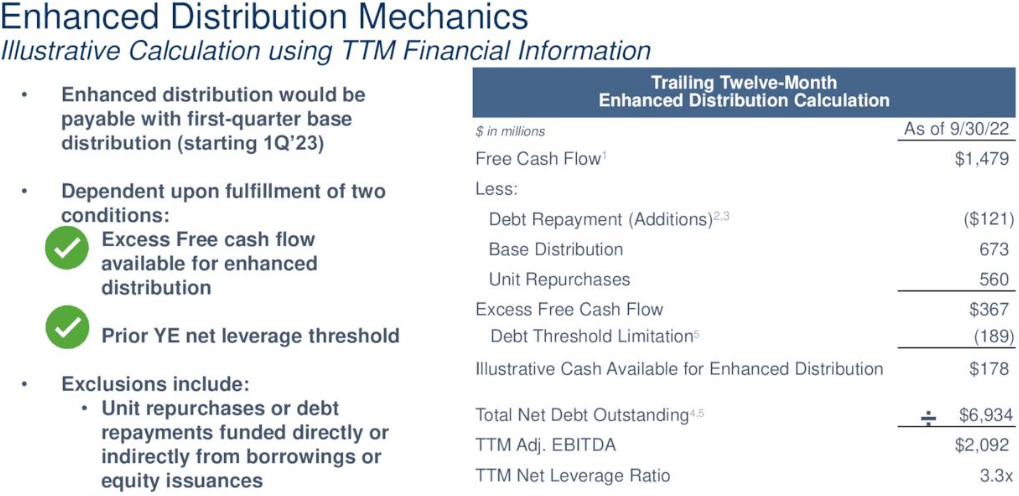

Unlike when conducting the previous analysis, they can now tick both of the boxes for enhanced distributions, in particular, the first box for “excess free cash flow available for enhanced distributions”. Despite hitting this milestone, alas management thus far refrained from declaring any additional distributions, although I suspect this will change as soon as next month when their upcoming results for the fourth quarter of 2022 are released. Apart from being a natural point in time as management also lays out their guidance for the year ahead, it also marks one year since they last pushed their quarterly distributions higher.

Ultimately, no one can necessarily know the future but at the same time, it would be quite odd for management to take the time to formulate this unitholder returns strategy unless they have a real intent to follow through in the short-term. When reviewing their most recent conference call for the third quarter of 2022, I see no reasons stopping this from eventuating. Granted, they calculate their scope for enhanced distributions their unique way that is affected by their credit facility drawings, as per the commentary from management included below.

“Additionally, we consider borrowings under our revolver to be a component of our optimal capital structure. Thus, as it relates to 2022, the amount of debt we ultimately pay off on the revolver at year-end will impact the size of any potential enhanced distribution.”

-Western Midstream Partners Q3 2022 Conference Call (previously linked).

As a result of this approach, it adds a degree of uncertainty to the extent of their likely forthcoming enhanced distributions but at the end of the day, more free cash flow will always equal more scope for more distributions. Meanwhile, unexpectedly high capital expenditure during 2023 could throw a spanner in the works, as they have not presently released this guidance. In my eyes, they have seemingly moved away from their high growth era as seen during 2019 when their capital expenditure was north of $1.3b and thus many times above its recent levels. Whilst this remains a risk, its probability is not too high, especially because circling back to earlier, management likely would not have laid out this framework for enhanced distributions if there was no intent of pursuing this path.

Author

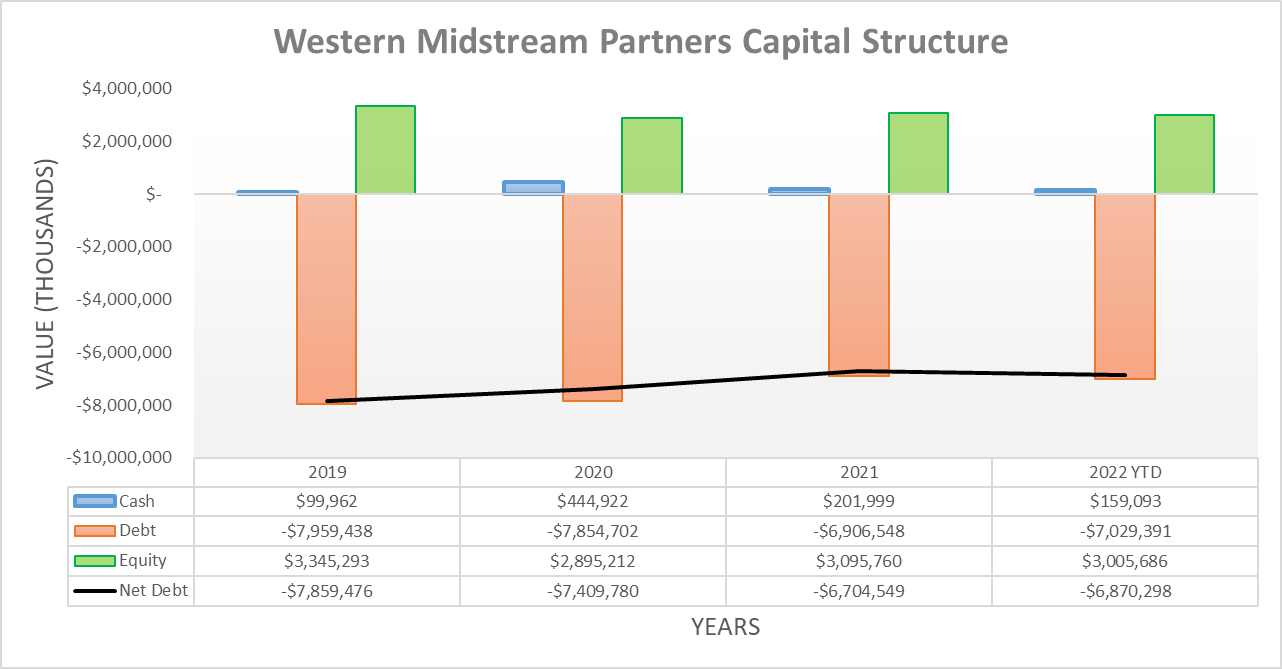

Despite continuing to generate ample free cash flow during the third quarter of 2022, their net debt still edged higher to $6.87b versus its previous level of $6.561b following the second quarter. This was primarily a result of their unit buybacks, which already totaled $447.1m in the third quarter alone and very impressively, equates to circa 4% against their current market capitalization of approximately $11b. This further paves the way for additional distributions but at the same time, these will obviously have to scale back slightly going forwards to ensure their net debt and thus leverage remains under control.

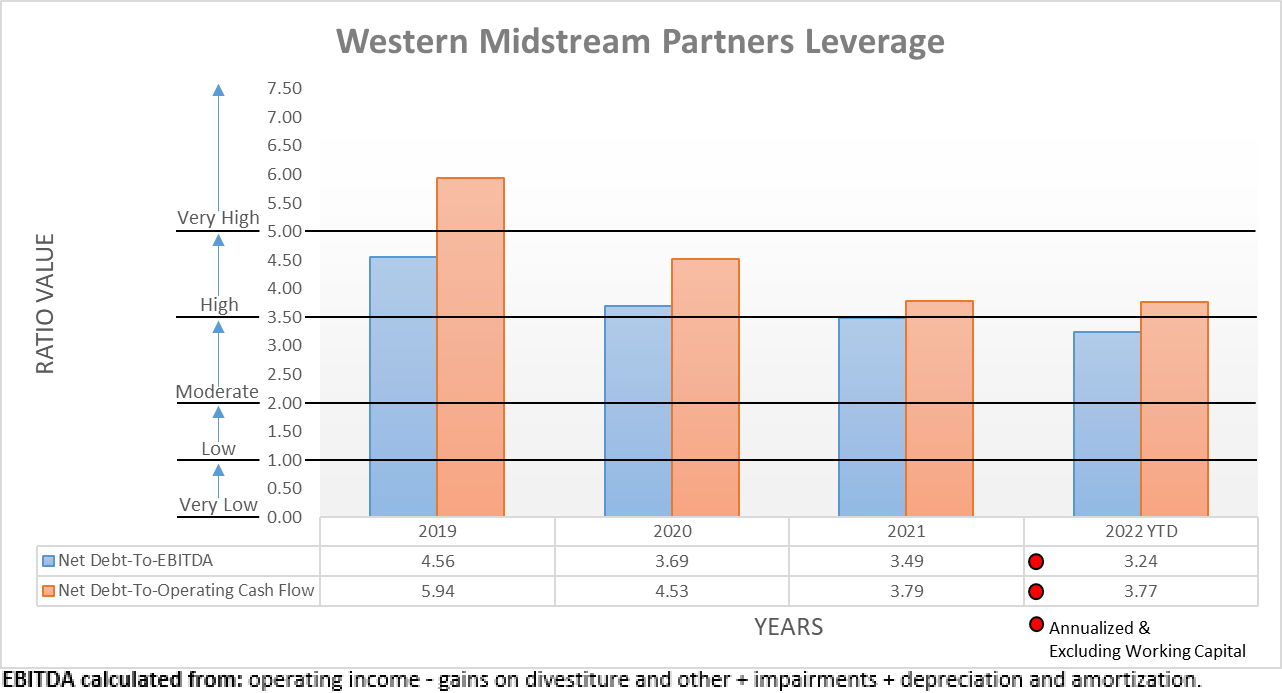

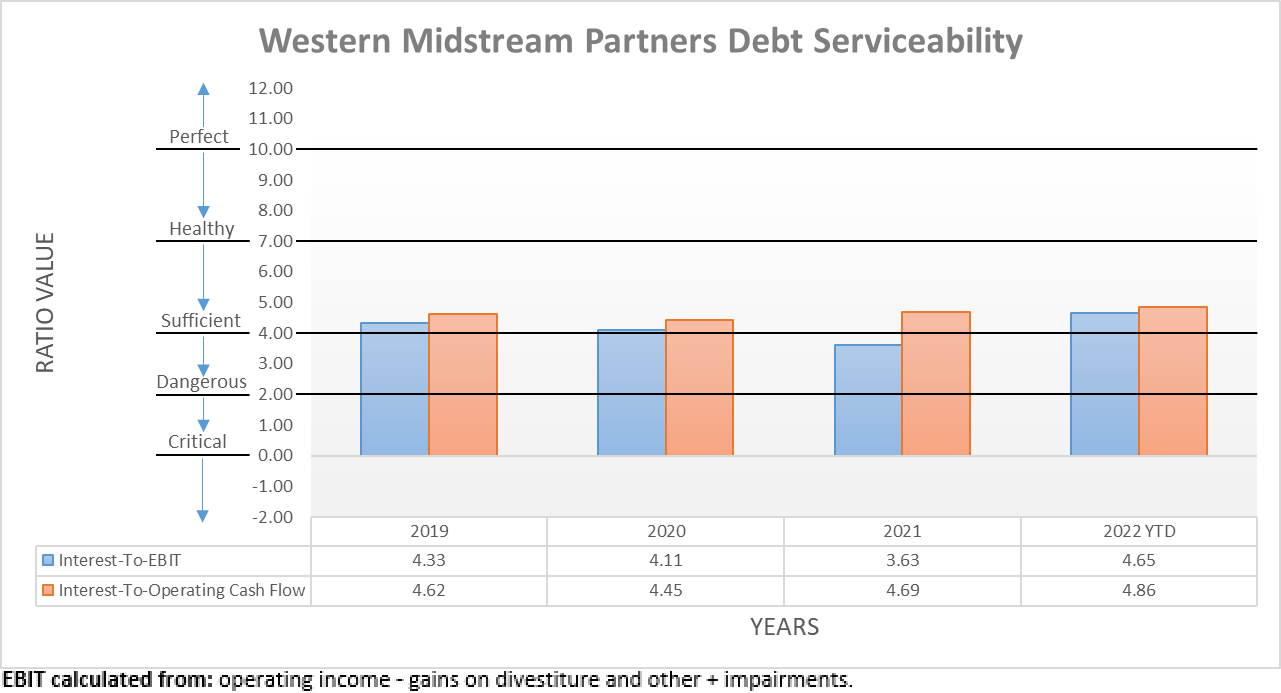

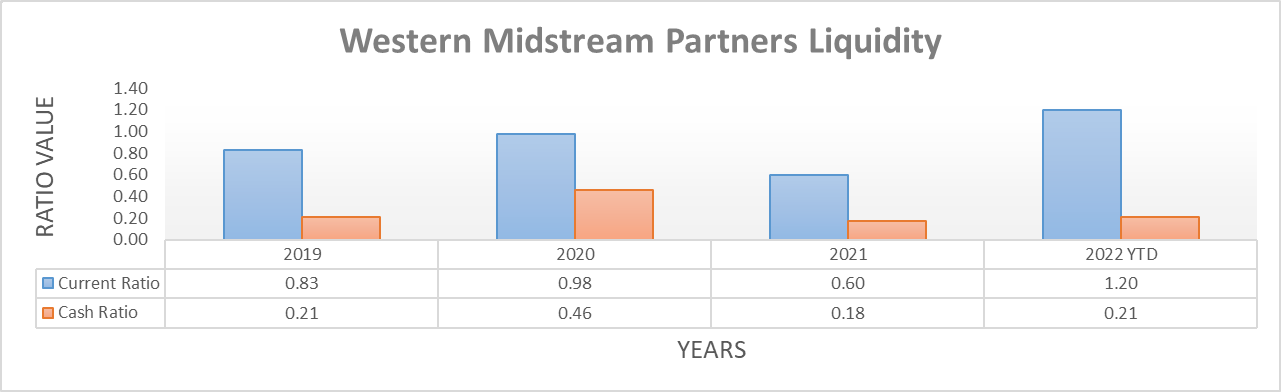

Since their net debt only increased slightly after conducting the previous analysis, it would be redundant to reassess their leverage or debt serviceability in detail, as these would not have materially changed. Concurrently, the same also applies to their liquidity because it has never been a point of concern in the past and given their cash balance increased to $159.1m during the third quarter of 2022 versus $97.4m following the second quarter, it could not house any material issues.

The three relevant graphs are still included below to provide context for any new readers, which shows their net debt-to-EBITDA lands at a moderate 3.24, whilst their net debt-to-operating cash flow of 3.77 is still slightly in the high territory of between 3.51 and 5.00 but, this is not concerning given their cash flow performance. Elsewhere, their debt serviceability is healthy with interest coverage of 4.65 and 4.86 when compared against their EBIT and operating cash flow, respectively. Unsurprisingly, their higher cash balance now leaves their liquidity strong with a current ratio of 1.20, along with a cash ratio of 0.21. If interested in further details regarding these topics, please refer to my previously linked article.

Author Author Author

Conclusion

Unlike when conducting the previous analysis, the company can now tick both of the boxes for enhanced distributions and thus my eyes are firmly focused on this front when their upcoming results for the fourth quarter are released next month. Since their strong cash flow performance persists and their financial position is solid, it helps pave the way for additional distributions and thus, it should not be a surprise to see that I believe maintaining my strong buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Western Midstream Partners’ SEC filings, all calculated figures were performed by the author.

Be the first to comment