VioletaStoimenova

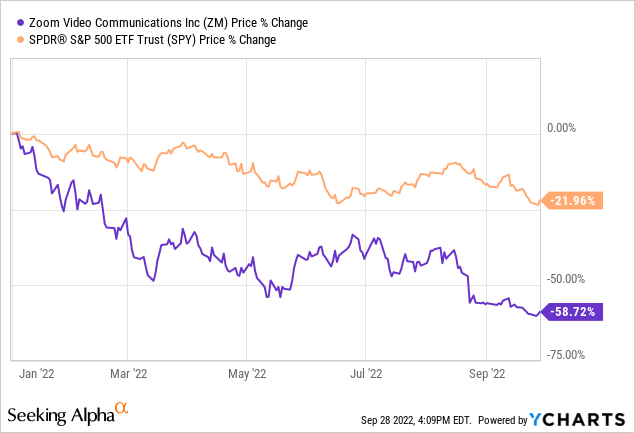

Zoom Video Communications’ (NASDAQ:ZM) stock price has fallen as much as 59% year-to-date, substantially underperforming the broader market.

In May 2022, we have published our first article in Zoom, titled: “Zoom in – Zoom out“. In that article, we outlined the main reasons why we believed at that time that Zoom may not be a great investment. These reasons included:

- EPS was expected to decline in the near term

- The firm’s strategy did not sound entirely convincing

- Intense competition

- Overvaluation

Since our article, ZM’s stock price has fallen another 22%.

Today, we will revisit our previous thesis and provide an updated view on Zoom taking the latest news, events and earnings results into account.

Q2 earnings report

While revenue has showed year-over-year growth of 8%, income from operations has seen a huge decline to $121.7 million compared to the $294.6 million in the same period a year ago.

Net income and diluted net earnings per share have also fallen substantially.

GAAP net income attributable to common stockholders for the second quarter was $45.7 million, or $0.15 per share, compared to GAAP net income attributable to common stockholders of $316.9 million, or $1.04 per share in the second quarter of fiscal year 2022.

While it is positive that Zoom is able to grow its customer base (18% growth in Enterprise customers, 37% increase in the number of customers continuing more than $100,000 in TTM revenue) and generate more revenues than a year ago, we believe that he large drop in earnings is concerning.

According to the firm’s latest guidance, they also do not see a dramatic change in the EPS trend for the rest of the year.

Also, a large portion of the firm’s revenue is being generated outside of the United States, meaning that currency exchange headwinds created by the strong USD are likely to keep negatively impacting the company’s financial performance in the near term.

EPS decline was already highlighted in our previous article and was one of our main reasons for rating the stock as a sell. To date, we see no improvement in this regard.

Competition

Many pandemic-induced effects and tailwinds for certain software companies are slowly disappearing. We believe, however, that the newly evolved trends in communication and collaboration are here to stay for the future, despite numerous firms increasingly switching back to 100% working from office. Both Microsoft Teams and Zoom have grown quickly in popularity and have captured large chunk of the market share during the last years. Currently, however, we are seeing industry consolidation to a certain extent, meaning that firms that have decided to use a certain tool, are likely to stick with this for the long run.

We believe it will be difficult for ZM to capture a larger market share and simultaneously improve its EPS. Further, while Microsoft has many other products it can offer (which could lead to potential synergies and economies of scale), Zoom is relying only on a limited amount of products and services.

Credit Suisse has also recently published an article, in which the analysts have pointed out the importance of competition that Zoom faces from companies like Microsoft and Cisco.

At the moment, we still do not see that Zoom has a meaningful moat or a competitive advantage against other players in the communication space, which would justify improving our rating.

Valuation

While stock price has fallen by more than 20% since our last writing, but EPS has also declined. Actually, the firm became even less attractive from a valuation perspective. Traditional price multiples are still indicating that Zoom is trading at premium compared to the information technology sector median, with P/E Non-GAAP (TTM) being 16.6x and P/E Non-GAAP (FWD) being 20x.

As earlier stated, we do not believe that these multiples are justified. Due to the uncertain growth going forward, partially driven by potential industry consolidation and Zoom’s lack of moat, we believe there may be further downside for the stock in the near term.

Key takeaways

Despite the growing revenue and customer base, the declining earnings and the outlook for the rest of the year do not make the firm an attractive investment right now.

We still believe that Zoom does not have a substantial moat or competitive advantage, which could help the company gain market share, while also improving its financial performance.

In our opinion, the firm remains overvalued.

At this point, we see no positive development, neither in the macroeconomic landscape nor in the firm’s financial performance, that would justify upgrading the stock.

For these reasons, we maintain our sell rating.

Be the first to comment