ipuwadol

Thesis

WalkMe (NASDAQ:WKME) stock could be an interesting opportunity for investors looking to gain exposure to a nascent and fast growing new software industry vertical – the industry for digital adoption platforms. According to DataIntelo, this industry is expected to grow at a CAGR of approximately 16% through the next decade, reaching a market size of about $3.73 Billion by 2030, up from an estimated $1.02 billion in 2022. And WalkMe is a pioneer and market leader in this industry.

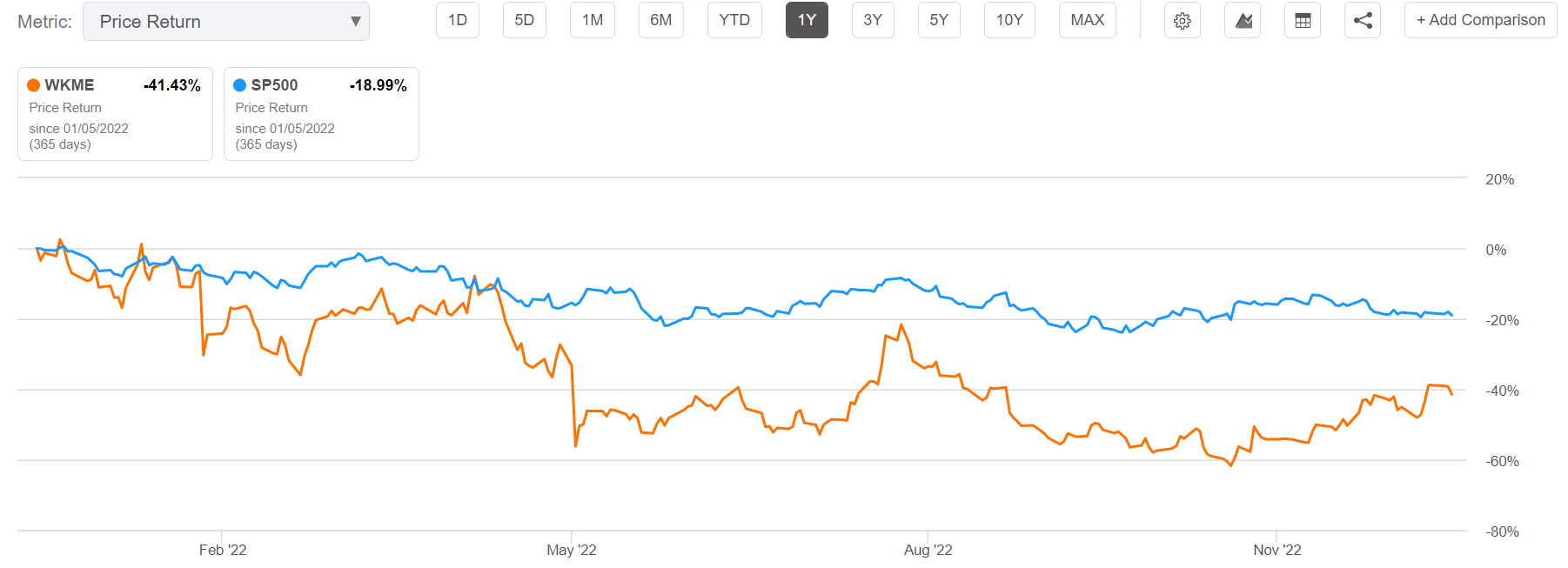

For reference, WalkMe stock is down approximately 41% for the trailing twelve months, as compared to a loss of about 19% for the S&P 500 (SPY). And although WalkMe’s recent share price performance is encouraging, being up more than 50% since early November, the stock is still down approximately 70% from all-time highs.

Seeking Alpha

About WalkMe

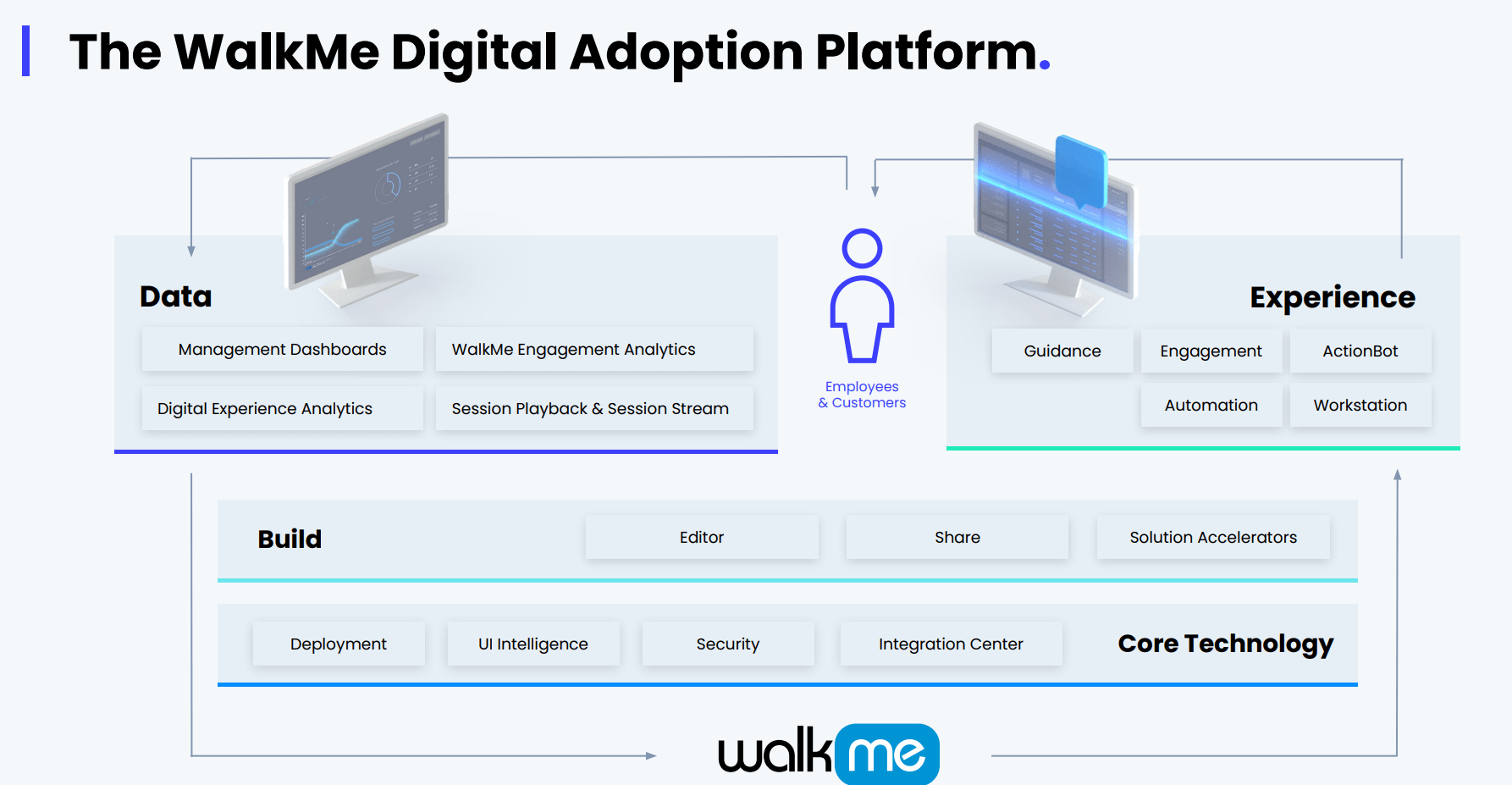

WalkMe is a digital adoption platform that aims to help companies improve the user experience and increase productivity by providing in-app guidance, assistance, and automation. In that context, WalkMe specifically targets companies that have complex digital systems and processes, such as enterprise software, e-commerce platforms, and financial services. These companies often struggle with low adoption and utilization rates, leading to decreased productivity and revenue. By providing in-app guidance and assistance, WalkMe helps these companies improve the user experience and increase adoption and utilization of their digital systems and processes.

WalkMe Q3 2022 Results

The company was founded in 2011 and has raised over $200 million in funding from notable investors including Softbank, Insight Partners and Francisco Partners. WalkMe was founded by in 2011 in Israel by Dan Adika, Rafael Sweary, and Rafi Shwartz. Notably, all founders are still with the company and serve key roles: Adika is WalkMe’s Chief Executive Officer, Sweary and Shwartz hold the positions of President and Chief Strategy Officer respectively.

WalkMe’s Opportunity

The market for digital adoption platforms is still young, but promises lots of potential. According to Forrester, who first covered Digital Adoption Platforms (DAPs) as a distinct industry in late 2021:

DAPs are emerging as catalysts for managing digital transformation, with purpose-built features to enable users to do more with enterprise applications.

Notably, the market is expected to grow at a compound annual growth rate of about 16% throughout the next decade, reaching a market size of about $3.73 billion by 2030, up from an estimated $1.02 billion in 2022. This growth is being driven by the increasing adoption of digital technologies and the need for organizations to improve the user experience and increase productivity. For example, technology research firm Gartner has estimated that:

by 2025, 70% of organizations will use digital adoption solutions across the entire technology stack to overcome still insufficient application user experience.

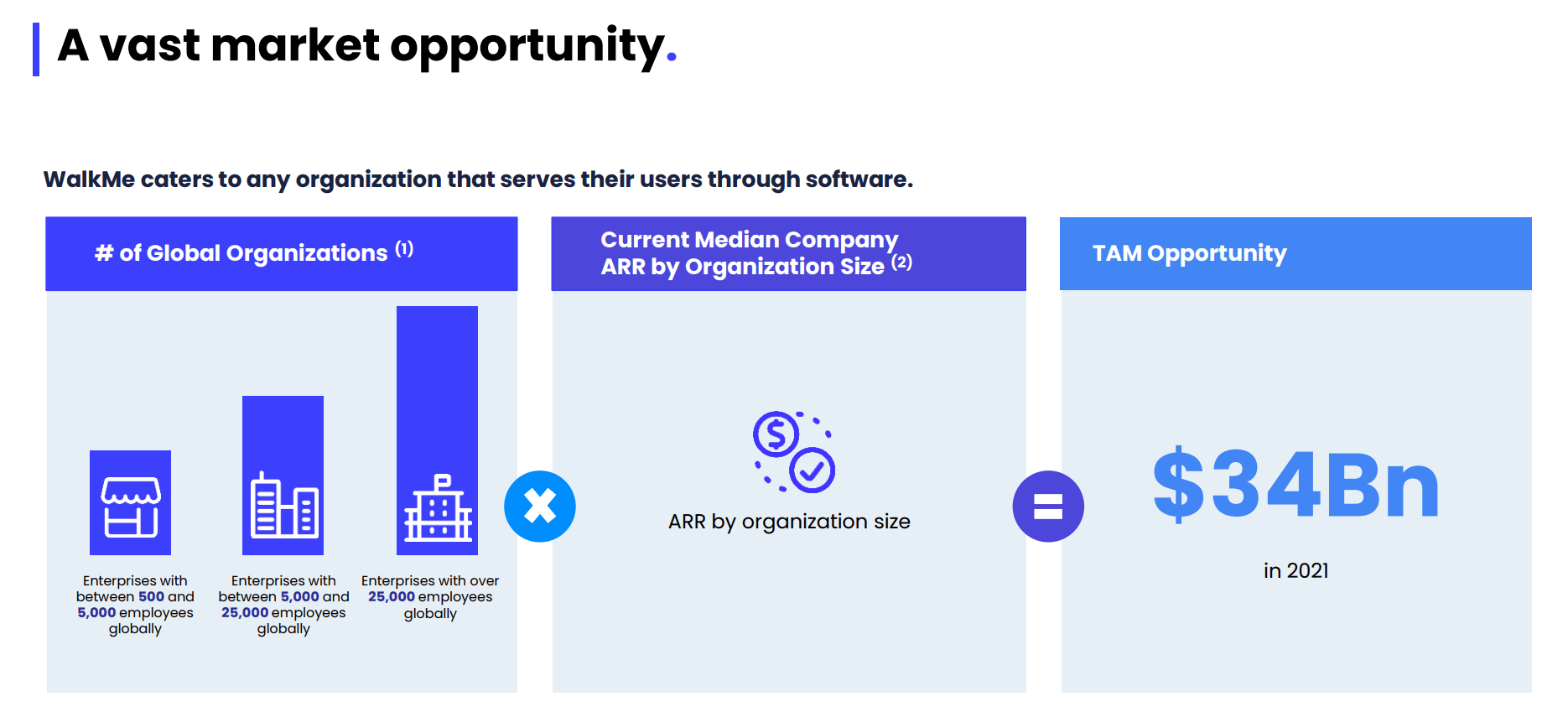

WalkMe management itself has suggested that the company’s market opportunity could be as big as $34 billion.

WalkMe Investor Day Presentation

One of the main drivers of WalkMe’s growth is the increasing digitization of the economy, as more and more businesses are adopting digital products and services. This trend is expected to continue in the coming years, providing a strong tailwind for WalkMe’s growth.

Another key growth driver for WalkMe is the increasing demand for improved user experience. With the proliferation of digital products, businesses are under increasing pressure to deliver intuitive and seamless user experiences. WalkMe’s platform helps businesses achieve this by providing on-screen guidance and interactive walkthroughs, which can help improve user retention and reduce churn.

WalkMe has a number of competitive advantages that have allowed it to become a leading player in the DAP market. One of these advantages is its intuitive and user-friendly platform, which enables companies to easily create and deploy in-app guidance and assistance. This is important because for many software applications, companies need to quickly and effectively onboard and train new users, reducing the time and resources needed to bring them up to speed.

Another competitive advantage of WalkMe is its comprehensive and customizable feature set. The platform offers a range of tools, including interactive walkthroughs, personalized guidance, task automation, and analytics, which allows companies to tailor the platform to their specific needs and goals.

Finally, WalkMe has already built an extensive network of collaboration and partnerships to support the company’s global expansion. For example, WalkMe has already established collaborations with software integrators such as Accenture (ACN), Deloitte and IBM (IBM), as well as a strategic product partnership with Celonis.

Financials And Valuation

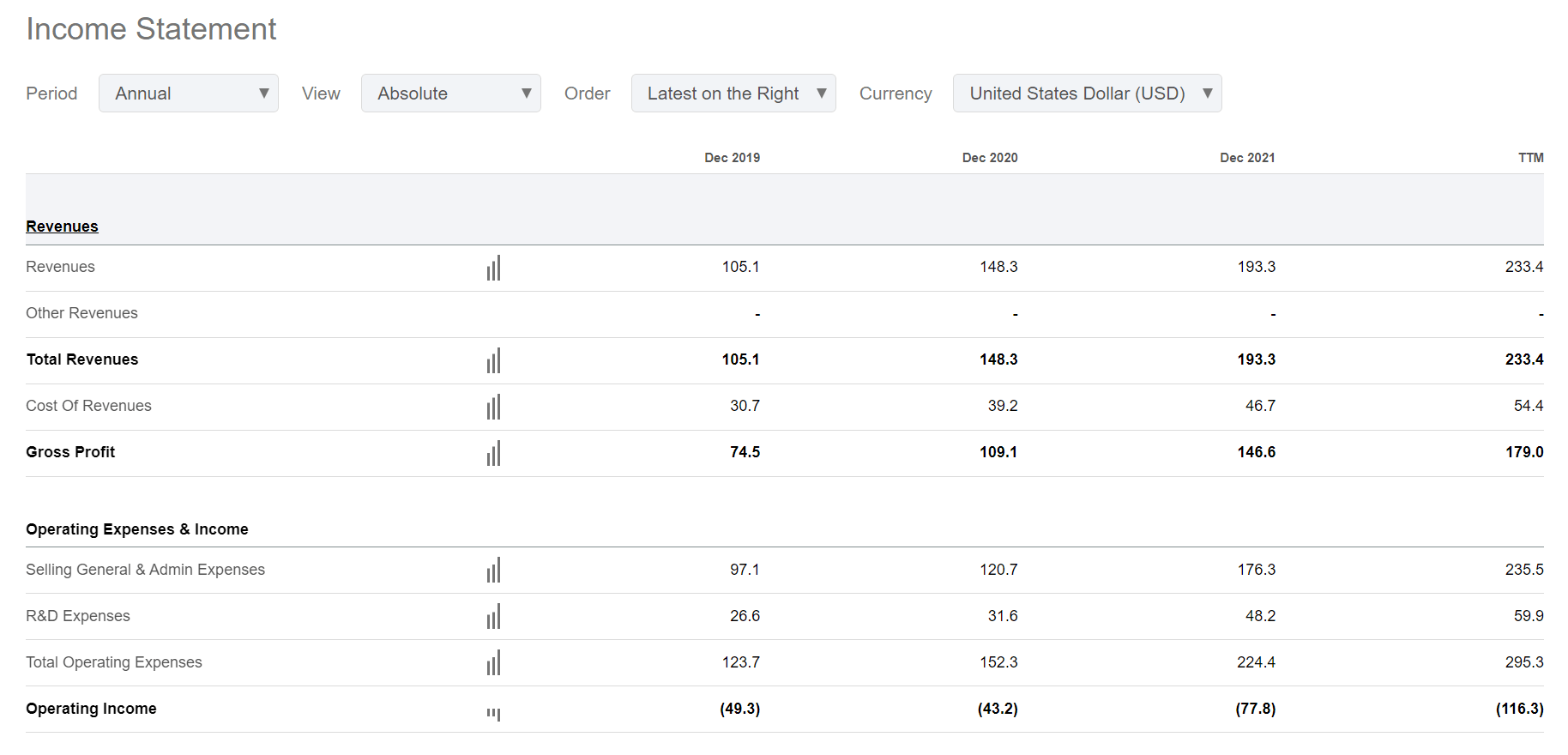

During the period from 2019 until 2022 (TTM reference), WalkMe’s revenues have expanded at a CAGR of approximately 30%, growing from $105 million in 2019 to $233 million for the trailing twelve months (Q3 2022 reference). Gross profit has expanded at a similar rate, jumping from $75 million to $179 million. In 2022, (TTM reference), WalkMe has recorded a loss from operations of $116 million. Cash provided from operations was considerably better: only negative $51 million.

Although WalkMe is still loss-making on an operating income basis, investors should consider that the WalkMe is investing heavily in growth. And accordingly, the metric should be relevant for decision-making purposes, especially since WalkMe’s loss-making is supported by an exceptionally strong balance sheet. As of late September 2022, WalkMe recorded a net-cash position of $304 million.

Seeking Alpha

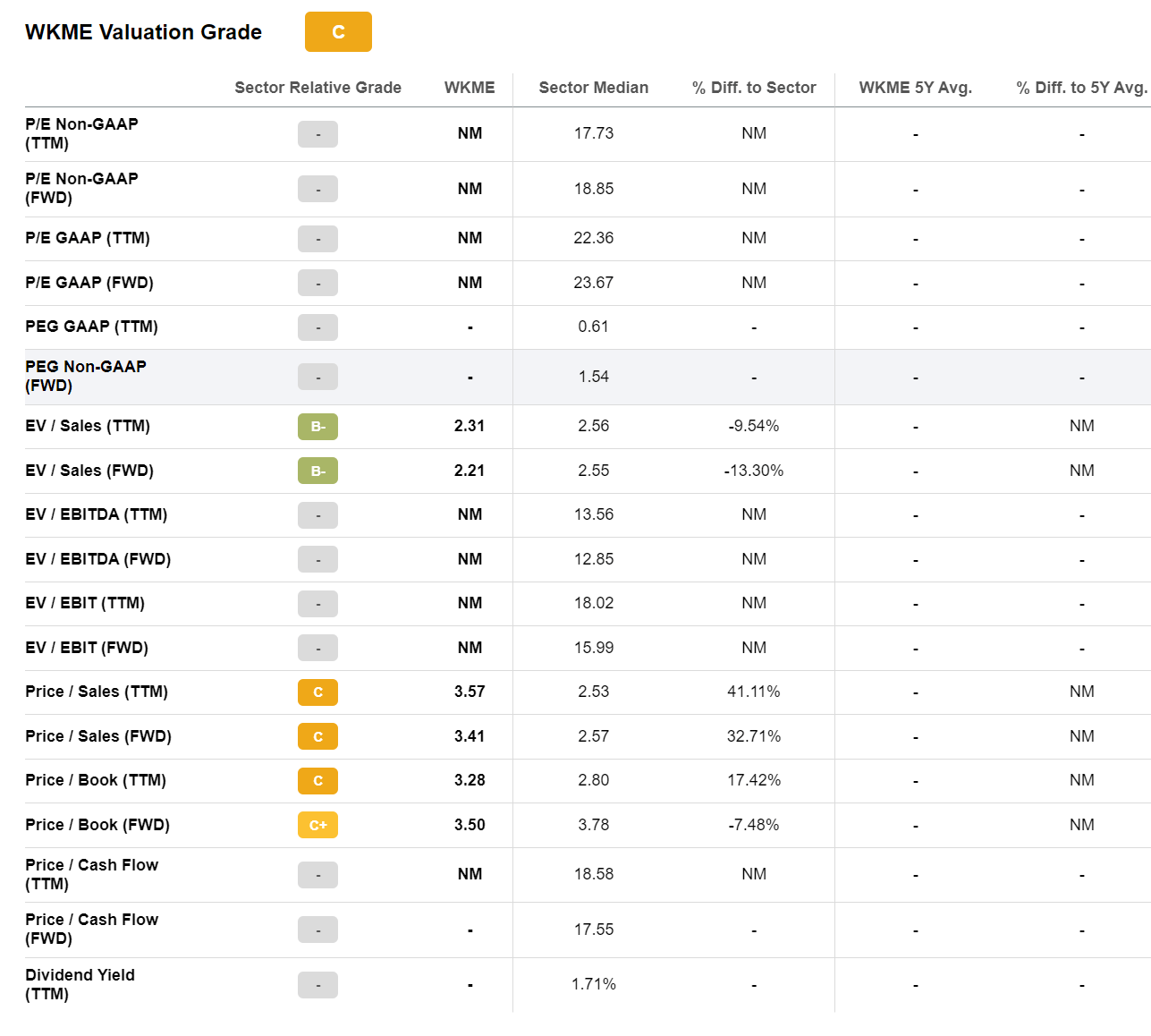

Valuation Looks Cheap

Although WalkMe’s loss-making operations, paired with fast revenue growth and market potential, make it difficult to value WalkMe stock, investors may reasonably argue that WalkMe is trading cheap. According to analyst consensus FWD metrics, WKME stock is currently trading at an EV/Sales of x2.2.

For example, if an analyst would assume that WalkMe can grow in line with the market–at a CAGR of 16% until 2030–and further estimate that the business’ operating income margin would be approximately 15%, then WalkMe would effectively generate about $1.3 billion of operating income in 2030. For reference, WalkMe’s enterprise value is about $530 million. Thus, there is arguably more than sufficient margin of safety in the calculation.

Seeking Alpha

Risks

Competition: WalkMe faces competition from other digital adoption platforms such as Whatfix, Pendo, and Appcues. In order to remain competitive, WalkMe will need to continuously innovate and improve its product offerings.

Dependence on third-party platforms: WalkMe’s technology integrates with a variety of third-party platforms, including web and mobile applications, CRM systems, and customer support tools. If any of these third-party platforms experience disruptions or outages, it could negatively impact WalkMe’s service.

Cybersecurity risks: As a technology company that handles sensitive user data, WalkMe is vulnerable to cybersecurity threats such as data breaches, cyberattacks, and ransomware. The company will need to invest in robust security measures to protect itself and its customers from these threats.

Economic downturns: WalkMe’s business is subject to economic conditions and the company may be negatively impacted by economic downturns or recessions. This risk can be mitigated by diversifying the company’s customer base and expanding into new markets.

Dependence on key personnel: WalkMe’s success is partially dependent on the continued contributions of its key personnel, including its founders and senior management team. The loss of any key personnel could negatively impact the company’s operations.

Conclusion

WalkMe is an interesting investment opportunity due to its leading market position in a young and fast-growing new software industry – the market for digital adoption platforms. While there are some risks to investing in the company, such as the general uncertainty surrounding DAP and a still loss-making business model, investors should consider that the risk/ reward for WKME looks very favorable at an EV/ Sales of x2.2. A simple, although speculative, thought exercise suggests that WalkMe could generate operating income of $1.3 in 2030

Be the first to comment