imaginima

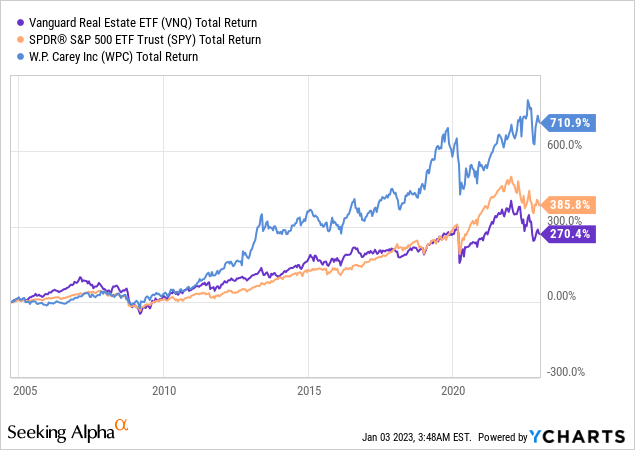

W. P. Carey (NYSE:WPC) has consistently delivered strong returns, having outperformed both the S&P 500 index (SPY) and the popular Vanguard Real Estate ETF (VNQ) for many years. Founded in 1973, the company has a long track record of successfully acquiring, managing, and leasing commercial properties, and has a diversified portfolio of assets that spans across various sectors and geographies. Its focus on long-term, triple-net leases helps to mitigate some of the risks associated with owning and operating commercial properties.

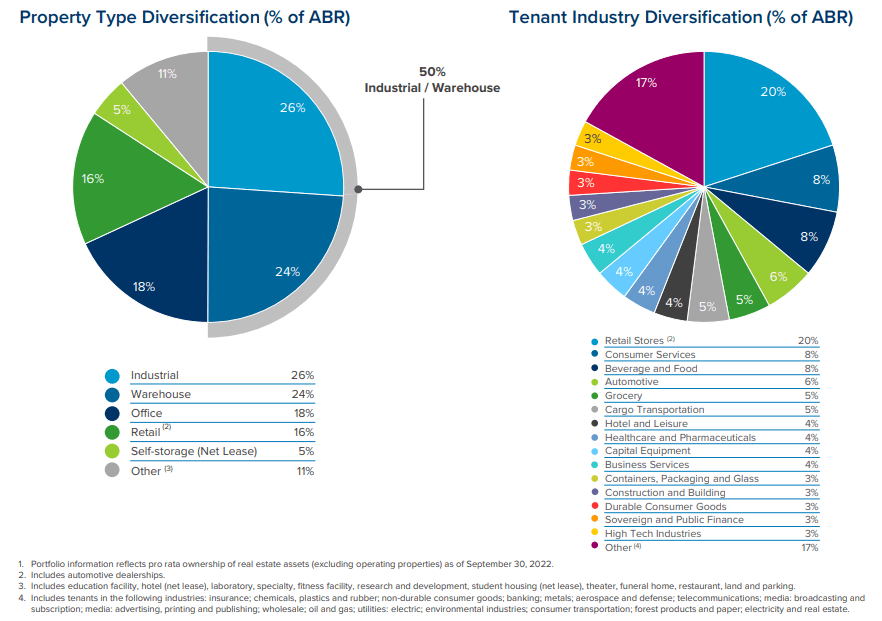

One concern we do have about the company is that it has a non-negligible exposure to offices, currently ~18% of the portfolio, as we believe this asset class will underperform due to the work-from-home trend.

The company’s smart, strategic acquisitions and portfolio management have resulted in stable occupancy even during the global financial crisis and throughout the Covid pandemic. At the end of the most recent quarter occupancy was 98.9%, which is quite impressive. Similarly, coming out of the global financial crisis occupancy was a still very respectable 96.6%. This level of stability is one of the main reasons that W. P. Carey shares are worth considering.

Rent Increases

Rent escalations or index-linked rent increases, are critical to help protect investors against inflation. This is particularly true for W. P. Carey given its long-term leases, with a weighted-average lease term of 10.9 years, which means it would be easy for rents to fall well below market rates before they can be adjusted. Fortunately, over 99% of the company’s annualized base rent comes from leases with contractual rent increases, including 55% linked to CPI. In Q3 2022 its annual contractual same store growth reached 3.4%, which while still considerably below the rate of inflation, was at least higher than the sub 2% same store growth the company was posting during 2020 and 2021. We would be more concerned that same store growth is trailing inflation if the company had more variable-rate debt, but as we’ll see more than 80% of its debt is fixed interest. One of the weakest segments in terms of annualized base rent increases was the office property type, with only a 2.2% same store annual rent increase in the last quarter.

W. P. Carey Investor Presentation

Diversification

The company has a highly diversified portfolio by geography, tenant, property type and tenant industry. The company also likes to explain their strategy as looking for “mission-critical” assets that are essential to a tenant’s operations, making it less likely that they will break their leases. Helping the portfolio stay occupied and resilient are the company’s asset management offices in New York and Amsterdam that are in charge of addressing lease expirations, changing tenant credit profiles, and asset repositioning/dispositions.

We appreciate the fact that roughly half the portfolio is in the industrial and warehouses categories, which we believe have better prospects. We are a little less optimistic about retail and self-storage, but our biggest concern is without a doubt the exposure to the office segment. Given the increasing vacancy in offices in many cities due to the work-from-home trend, this is a major headwind for the company. As we saw in the section above, office is already posting the weakest same-store growth, and we would not be surprised if the company had to lower rents to maintain occupancy in the future. In terms of geographic diversification, around 65% of NOI comes from the US, 32% from Europe, and roughly 3% from other countries.

W. P. Carey Investor Presentation

Growth

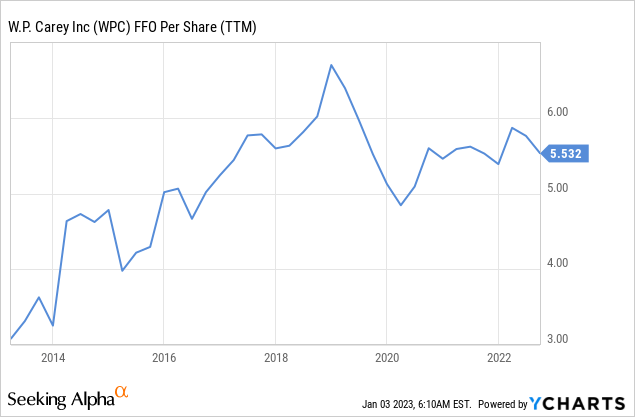

FFO per share has grown from ~$3 per share ten years ago, to ~$5.1 per share for the trailing twelve months. This is a respectable compounded annual growth rate of ~5.4%, but FFO per share is still below the peak reached around 2019. Given a number of headwinds, including the work-from-home trend, rising interest rates and financing costs, we believe FFO per share growth will be sub 5% for the next few years.

Balance Sheet

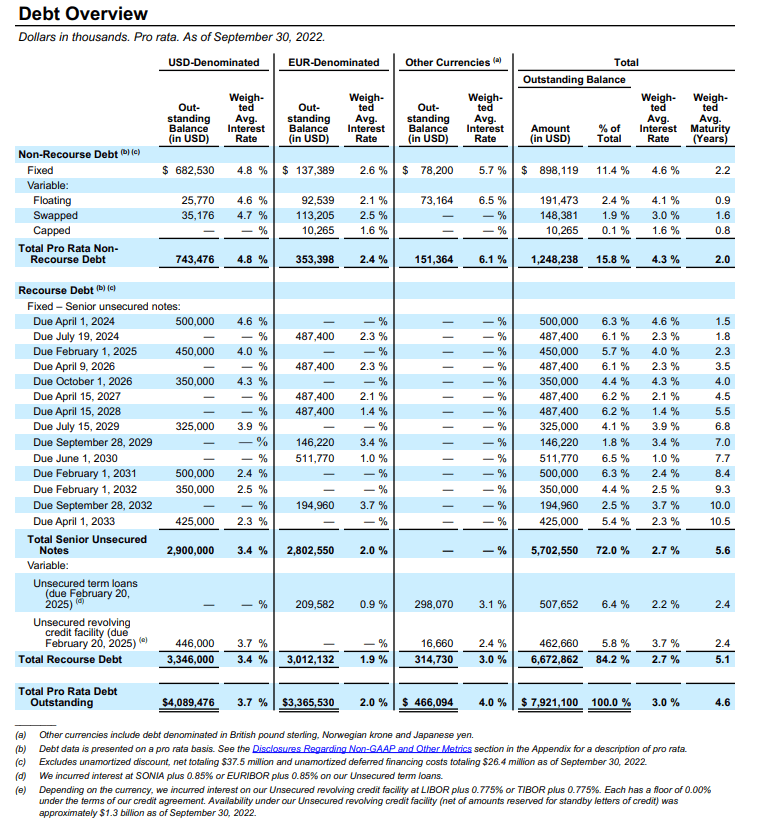

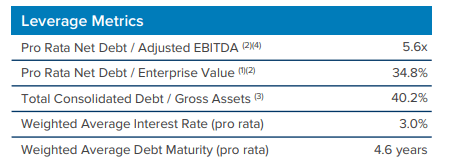

W. P. Carey does have a solid, Investment grade, balance sheet which was recently upgraded to Baa1 (stable) from Moody’s and a BBB (positive) from S&P. There are several things we like when looking at its debt profile. First, most of the debt is fixed interest type. Second, the weighted average interest rate is very low, at ~3%. Third, the weighted average maturity is a healthy 4.6 years. It is also worth pointing out that a significant part of the debt is Euro denominated, which has a very low average interested rate of ~2%. Finally, the debt is well laddered, with maturities spread through 2033.

W. P. Carey Supplemental Report

Leverage remains at a reasonable level, with net debt/adjusted EBITDA at 5.6x, and total consolidated debt at ~40.2% of gross assets.

W. P. Carey Investor Presentation

Valuation

If we add adjusted funds from operations for the last four quarters, we get $5.32 per share. At current prices around $78 that results in a multiple of ~14.6x. This is only slightly cheaper than the sector median of ~15.2x.

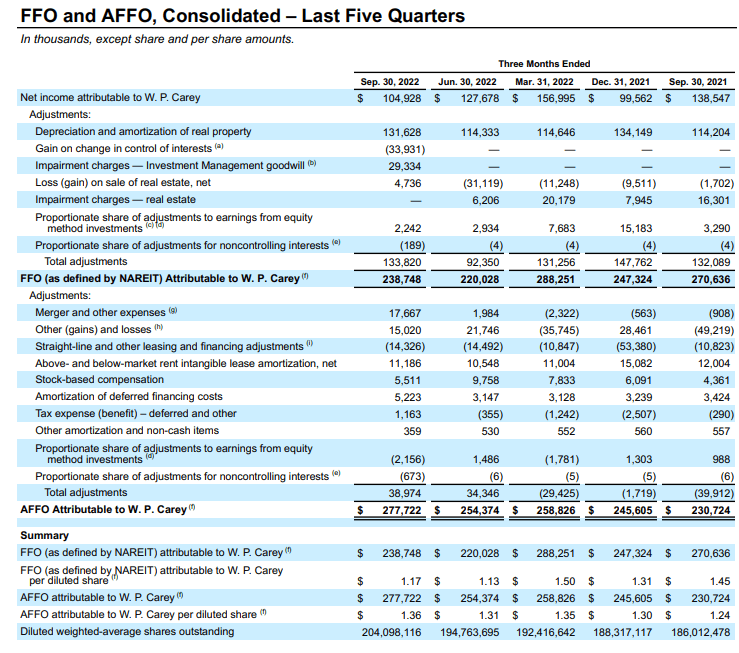

As can be seen in the table below, the company has issued many shares resulting in the diluted weighted average shares outstanding considerably increasing in the past year, yet this barely increased per share FFO/AFFO.

W. P. Carey Supplemental Report

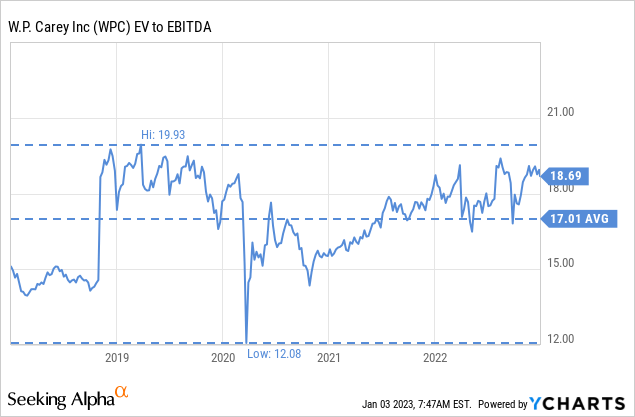

Compared to its own history shares are not cheap either. In the last five years EV/EBITDA has averaged ~17x, which is actually lower than the current ~18.6x.

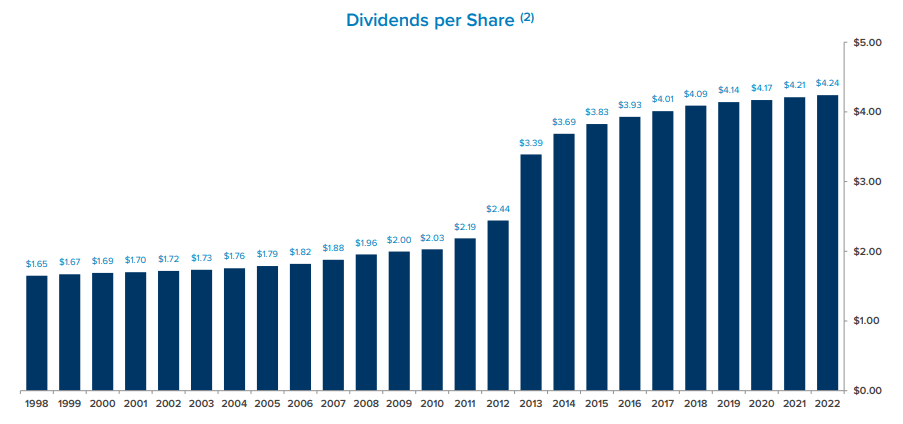

At $78 the dividend yield is not that exciting either, with shares currently yielding ~5.4%. While W. P. Carey has raised its dividend since going public in 1998, its most recent increases have been extremely modest, and we believe the next few years dividend growth will remain low.

W. P. Carey Investor Presentation

We estimate fair value for the shares at ~$83 per share, which means we believe shares to be only very moderately undervalued. Our estimate is based on the net present value of the REITs future earnings stream, and assumes ~3% FFO per share growth for the next couple of years, recovering to ~6% in FY25. We assume a terminal growth rate of 3% and we use a 10% discount rate. Based on this we rate shares a ‘Hold’ at the moment.

| FFO | Discounted @ 10% | |

| FY 22E | 5.31 | 4.83 |

| FY 23E | 5.47 | 4.52 |

| FY 24E | 5.63 | 4.23 |

| FY 25E | 5.97 | 4.08 |

| FY 26E | 6.33 | 3.93 |

| FY 27E | 6.71 | 3.79 |

| FY 28E | 7.11 | 3.65 |

| FY 29E | 7.54 | 3.52 |

| FY 30E | 7.99 | 3.39 |

| FY 31E | 8.47 | 3.27 |

| FY 32 E | 8.98 | 3.15 |

| Terminal Value @ 3% terminal growth | 128.27 | 40.87 |

| NPV | $83.21 |

Risks

While it can be argued that the valuation is still at a reasonable level, we believe there are several headwinds worth considering. The biggest one in our opinion is the exposure to the office segment at ~18%, which is likely to be significantly impacted by the work-from-home trend. Other risks worth considering include the rising interest rate environment, a potential recession in 2023, and significant debt maturities in 2024 and 2025 of over a billion dollars.

Conclusion

We believe W. P. Carey shares are only slightly undervalued, and that there are much better bargains currently in the market. That said, we understand why some investors would be willing to continue to hold the shares, given the outperformance the shares have delivered. While the company has good property type and geographic diversification, we are mostly concerned by the exposure to office properties. We believe FFO per share growth will remain modest due to this and other headwinds, including rising interest rates and a weakening economy. The current share price is very close to our estimated fair value, which is the main reason behind our ‘Hold’ rating. Among the things to like we would list a strong balance sheet, a long history of paying and increasing dividends, and exposure to industrial and warehouse properties.

Be the first to comment