Hugh Hastings/Getty Images News

Once thought by many to be the realm of science fiction, the space economy has really started heating up in recent years. One company in this market that is often overlooked is a firm called Virgin Orbit (NASDAQ:VORB). Fundamentally speaking, the company does not leave investors much to work with. But at the end of the day, buying into a business with limited revenue and significant net losses and cash outflows has to be more about the market opportunity than it does the firm’s current condition. Even so, management has reported some positive results lately that illustrate significant growth potential moving forward. And while it is impossible to truly value the business at this time, it does appear to make for an interesting prospect for long-term investors who believe that management can take this company to the moon.

Understanding Virgin Orbit

When investors first hear about Virgin Orbit, a common misunderstanding might be that the company is alternatively known as Virgin Galactic (SPCE). But this is not the case. That is not to say that they are not related though. In fact, they are cut of the same cloth so to speak. Previously, before the company went public in 2021, it fell under the umbrella of Virgin Group. Prior to that, it and Virgin Galactic were one company, but, in 2017, the two split so that Virgin Galactic could focus on space tourism, while Virgin Orbit could focus on its own niche offering. This offering involves providing launch services for companies and governments interested in placing satellites in orbit.

The company achieves these launches in a rather novel way. Unlike some competitors, Virgin Orbit has modified a Boeing 747, dubbed Cosmic Girl, to carry LauncherOne, a two-stage rocket that serves as the world’s first liquid-fueled, air-launched rocket that can reach space. The company’s business model does focus on using this technology to deliver satellites to space. In all, the company has succeeded in launching 26 different satellites into space so far. But the company does also have other plans for generating revenue in the future. On the national security and defense side, for instance, the company plans to provide government squadron services where an entire air-launch system can be a program of record that is then sold to government customers who, in turn, will actually own and operate the system in question. Also, starting in 2023, the company plans to launch its own satellites that it will then use to provide to customers who want access to their capabilities. Management calls this a satellite as a service business model. Other plans include offering value-added services for IoT (Internet of Things) and earth observation applications.

Author – SEC EDGAR Data

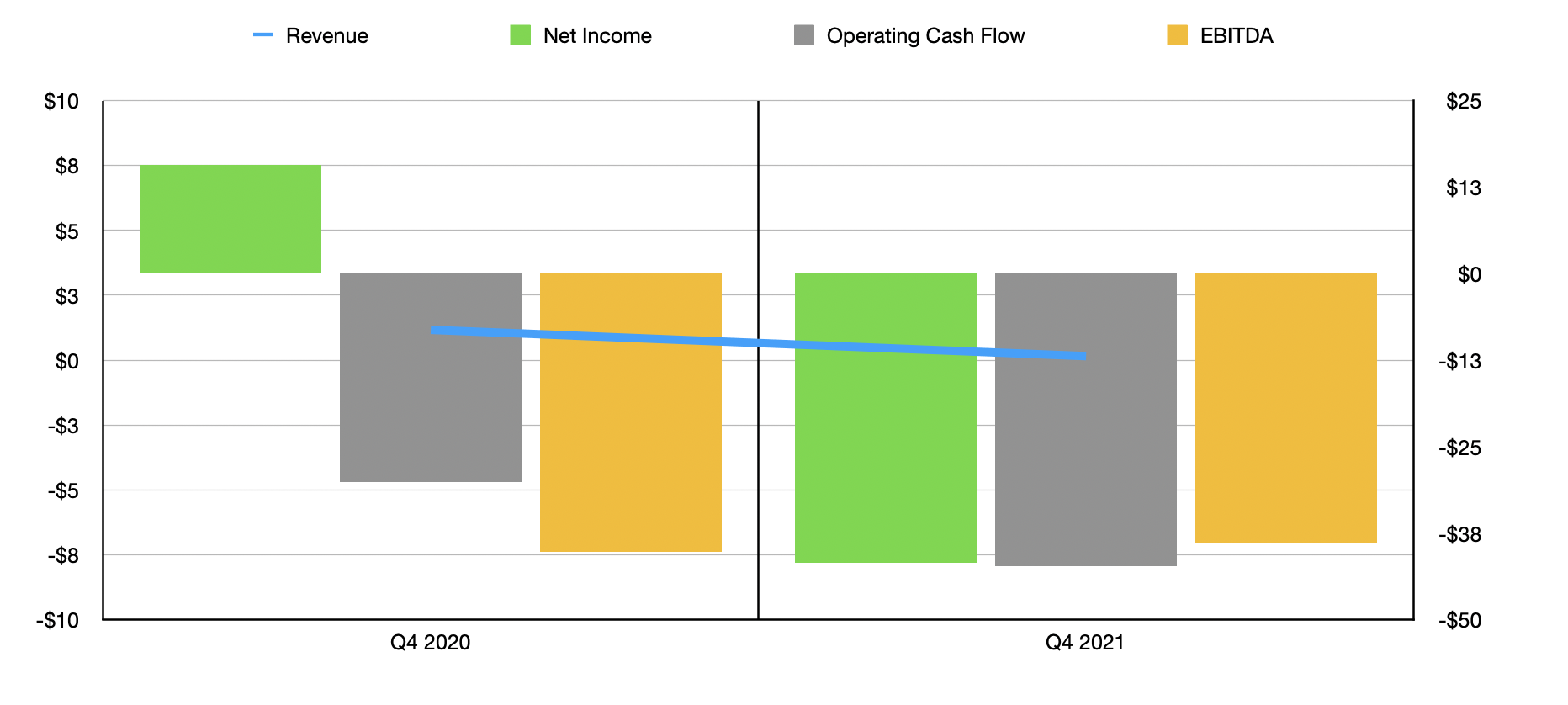

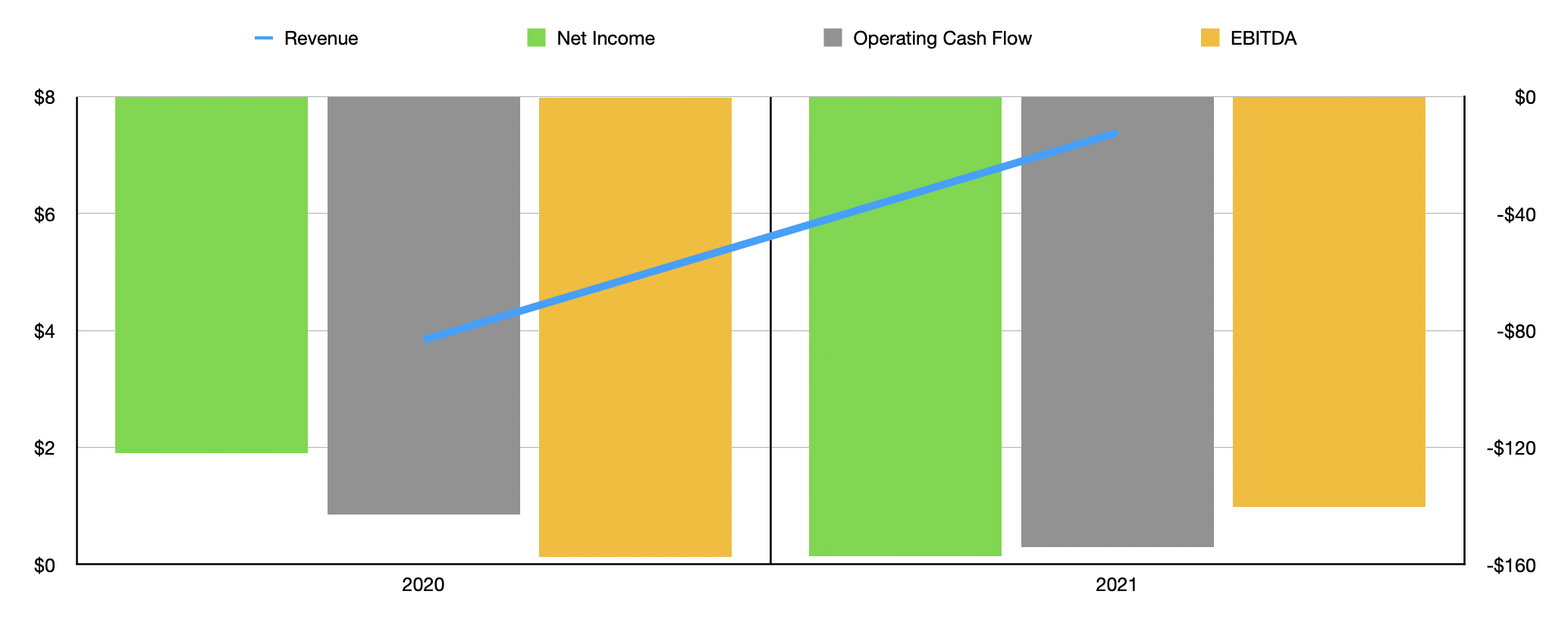

Fundamentally, there is not currently much to look at regarding the company. In the latest quarter, for instance, the company reported revenue of just $0.16 million. This compares to the $1.17 million the company generated the same quarter one year earlier. Even though the business did experience a decline here, it is worth noting that overall revenue for the entire fiscal year improved. Sales came in at $7.39 million. That was nearly double the $3.84 million the company reported in all of 2020. For a business with a market capitalization of $2.46 billion as of this writing, this looks rather disappointing. But as you will see, the picture is more complicated than that.

Author – SEC EDGAR Data

When it comes to profitability, Virgin Orbit has proven to struggle some. For the full 2021 fiscal year, for instance, the company generated a net loss of $157.29 million. A sizable portion of this loss, $41.73 million in all, came in the final quarter of the year. By comparison, the loss in 2020 was $121.65 million. That year was aided by a $15.72 million profit achieved in 2020’s final quarter. If this looks odd, it’s because it is. You see, during 2020, the company booked as income $62.2 million because of a non-refundable deposit that was made to it by its largest customer, a company that ultimately declared bankruptcy, essentially forfeiting the deposit.

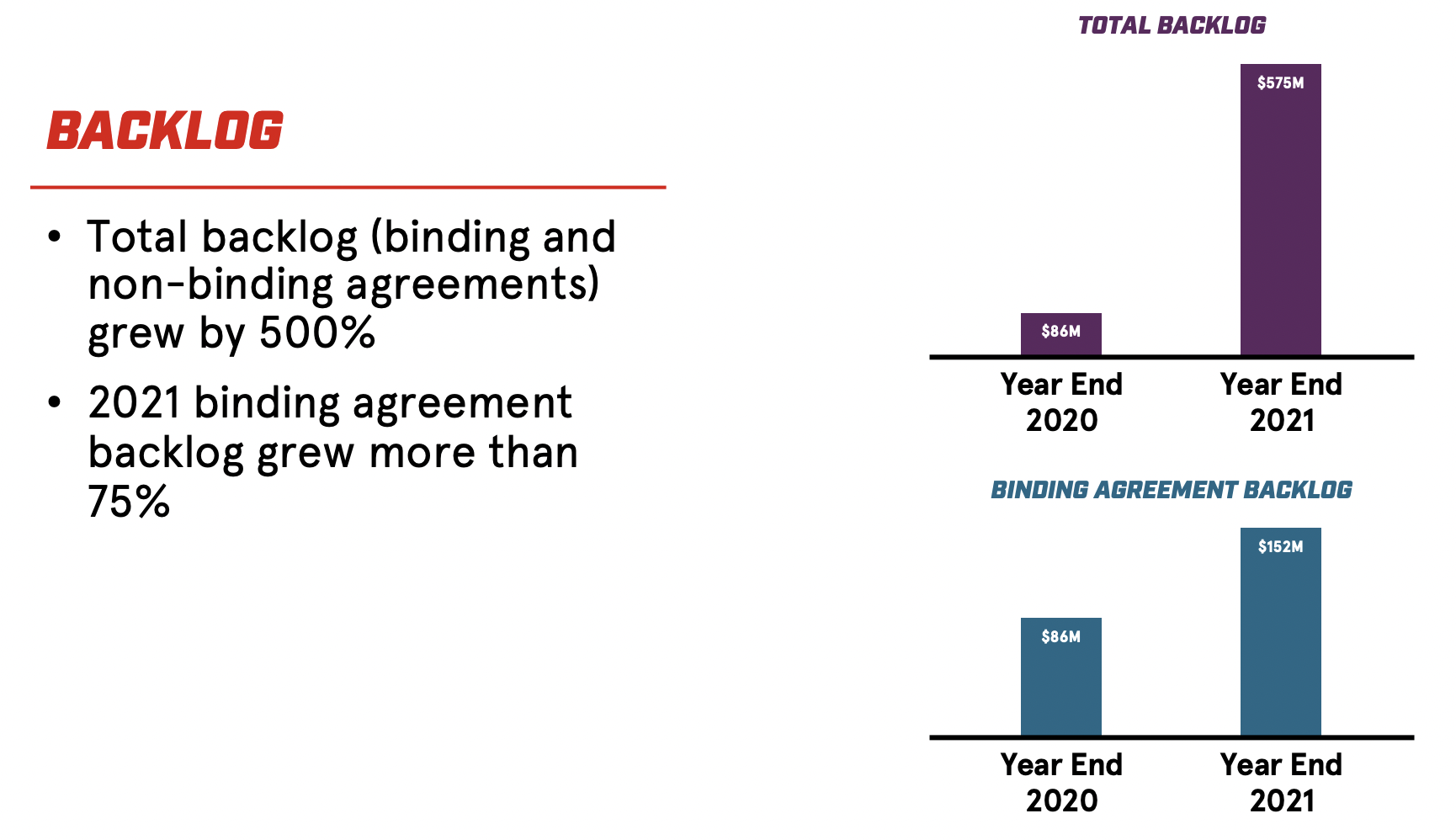

Perhaps more reliable than profitability would be cash flow. During 2021, Virgin Orbit generated operating cash flow of negative $154 million. This compares to the $143.02 million in negative cash flow generated in 2020. Another profitability metric to keep in mind is EBITDA. This also came in negative for the year. But in an interesting twist, it did improve relative to 2020, dropping from negative $157.5 million to negative $140.4 million. At this time, management’s goal is to become EBITDA positive by 2024. If this seems outlandish, especially given the company’s high-cost structure and low revenue, it’s important to point out an interesting leading indicator that management reported. This is the company’s backlog.

At the end of the 2021 fiscal year, the firm’s backlog swelled to $575 million. This compares to just $86 million reported one year earlier. The business has landed a number of valuable contracts recently, including, recently, a deal covering five flights that the business made with Arqit, plus it was recently chosen to provide its services to Oman for an initial satellite launch later this year and to participate in a voyage into deep space by the third quarter of 2024. As important as this backlog figure is, it is important to note that only $152 million worth of it is binding. This compares to the $86 million that was binding one year earlier. So, in theory, much of this could evaporate at a moment’s notice if clients were to lose faith in the business.

Virgin Orbit

This increase in backlog is good no matter how you look at it. It is clearly indicative of confidence from customers and it should provide confidence to investors. This is incredibly important because, fundamentally, there is not much value in Virgin Orbit at this time. So all of the value assigned to the company’s stock relates to expectations of the future. And if analysts are correct, the company could well have significant opportunities for itself in the future. This is because, according to one source, the total space economy was worth $447 billion in 2020. Another source pegged the value at $424 billion in 2019, with growth expected to take it to $1.4 trillion by 2030. As for where Virgin Orbit fits into this, the company is undeniably focused largely on the launch services niche at this time. While the company will expand and other avenues, it is worth noting that the global space launch services market is considerably smaller. One source estimated it was worth just $9.5 billion in 2019. But with a 15.1% annualized growth rate, it should expand to $47.6 billion by 2030.

Takeaway

Based on all the data provided, I will say that I find Virgin Orbit to be an interesting prospect for investors who want a satellite launch service business that has aspirations for more diverse operations in the future. To be clear, this is not a fundamental or value play. The assets of the business are likely worth far less than what the firm is trading for. And it generates neither the revenue nor the cash flow to justify its valuation if taken from a purely textbook approach to assessing its prospects. Rather, this is about whether management can succeed in capturing a sizable portion of a large and growing market over the next few years. If so, the gamble for investors today might well be worth it. But with the company likely on the hook for hundreds of millions of additional dollars in order to get where it needs to be, this is no trip for the cautious.

Be the first to comment