BalkansCat/iStock Editorial via Getty Images

Before they cut their dividend, you likely remember the barrage of analysts and authors on Seeking Alpha bickering daily as to whether they will cut their dividend. I’m talking about AT&T (T), not V.F. Corp (NYSE:VFC).

The fever pitch for VFC isn’t as extreme as T, but it certainly feels that way when you consider the company is only 1/10th the size. Unlike T though, this dividend story will likely have a different ending; more akin to Exxon Mobil (XOM) in 2022/2023 versus the dark days of 2020/2021.

Second fiddle isn’t so bad

Admittedly the brand power of VFC doesn’t hold a candle to Nike (NKE). That’s okay!

Formerly known as Vanity Fair Mills, V.F. Corp is an apparel and footwear company that has re-invented itself many times over since 1899. Calling them brand churners may be too harsh, but they are in the business of growing brands as well as disposing of them when better opportunities come along.

VFC Investor Day (Sept 2022)

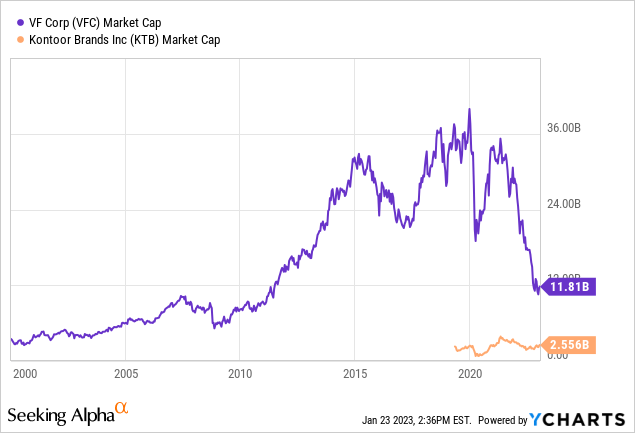

Take what is their flagship brand today, Vans. They weren’t even a part of VFC until 2004. With denim in decline, they spun out Wrangler and Lee as Kontoor Brands (KTB) in 2018. On that note, be aware that financial stats and authors often overlook this successful spin-off when calculating historical performance. VFC has been a better bet than you might realize.

Not saying the sub $12B market cap is good, but it looks almost 20% worse than actual, because you need to add in the value of Kontoor.

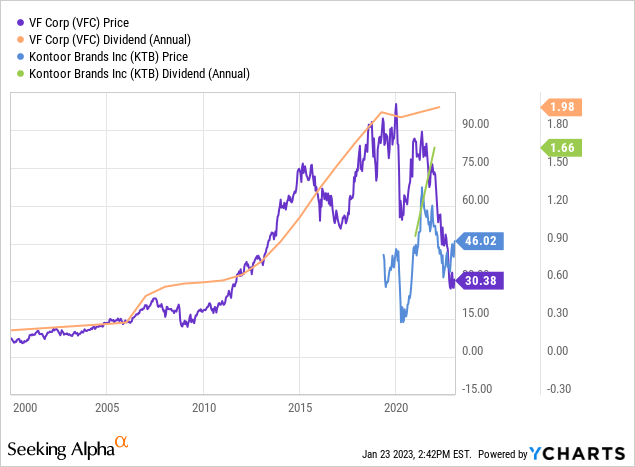

Furthermore, the fat yield. Consider the returns this century when you add in the dividends:

The orange line looks a bit wonky in 2019/2020 due to the spin-off but rest assured, VFC did not cut their dividend then. It has been growing for 49 years and counting.

YCharts does not allow me to chart what the returns look like with dividends. From another source, here’s what would have happened with a $10k investment on a DRIP:

DQYDJ

That $10,000 investment on the first trading day of January 2000 would now be worth $77,000. Reality is even better though because once again, this excludes the KTB spinoff. It’s no NKE (that would be worth $286k). The point here is that VFC has been a modest yet consistent compounder if you look across longer time frames.

Today’s valuation vs. historical

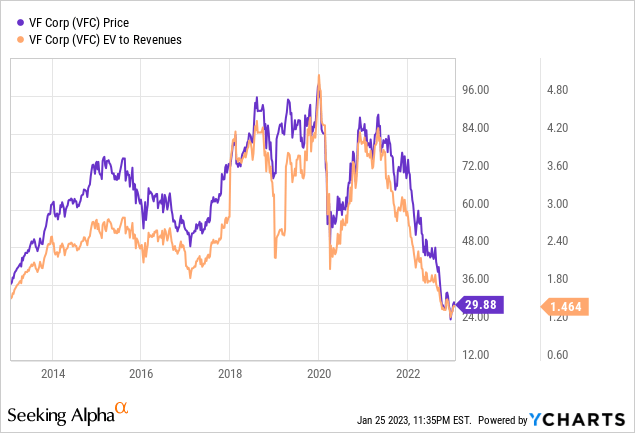

Let’s start with enterprise value to revenues. Here’s why:

- EV includes debt, which admittedly is on the higher end of historical.

- Margins have been thrown out of whack from Covid’s boom and bust of apparel demand, and even more so by supply chain issues. With those resolving, VFC should be returning to normalized margins.

- Once their profit margins normalize, since their EV/revenues is at a 10-year low, in theory, it also implies their PE will be at a 10-year low. Of course that’s assuming their share price remains the same as it is today. I don’t think it will.

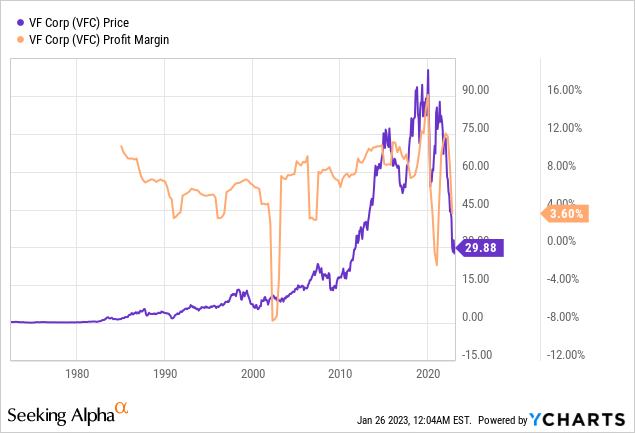

The next chart demonstrates this:

As far back as the data goes – 1985 – you can see the net margin averages around 6%. If you look at just the past 10 years, it’s averaged around 8%.

Because of Covid, it suddenly became less than half that, now sitting at 3.6%. Do you really think that will be permanent?

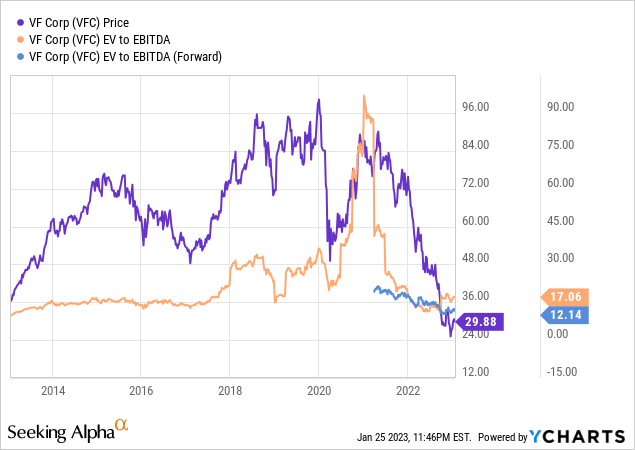

Let’s look at EBITDA next:

Even with the Covid hangover, you can see their EV to EBITDA is 17x right now and the forward multiple is just 12x.

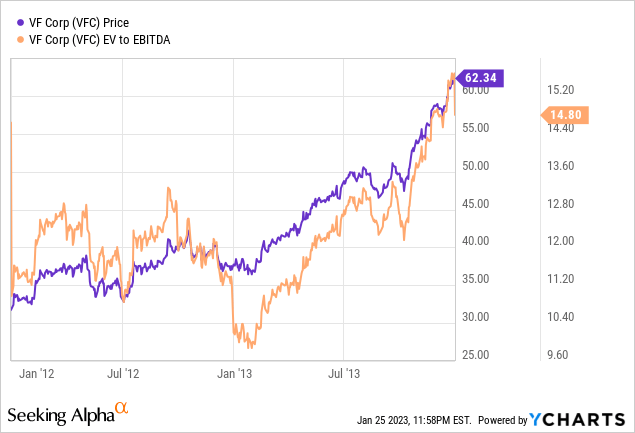

During the past 10 years when it has been at 17x, it’s a trough in valuation. If the forward multiple of 12x comes to fruition, it will only be beat by the multiple seen in early 2013. Here’s what happened after that:

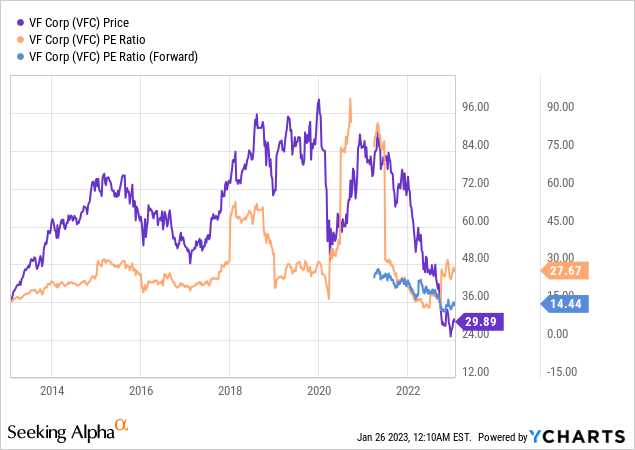

As you see, it didn’t stay long at sub 12x. Last, let’s look at PE:

The forward PE is 14x. If that materializes, it will mark a 10-year low. Do you think it will stay there?

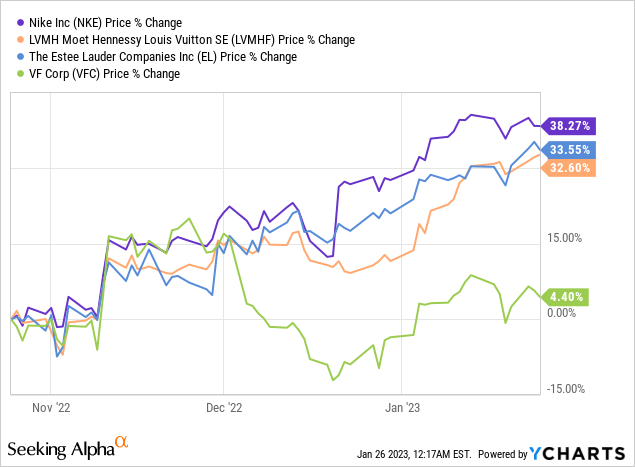

Then there’s China…

Since China did an about-face in December on the zero-Covid policy, luxury and apparel names have surged:

Well, most have surged. One of the few exceptions is VFC. That’s really not fair. I’m not saying any American apparel brand can compare to Nike’s popularity in China, but VFC isn’t doing too shabby over there:

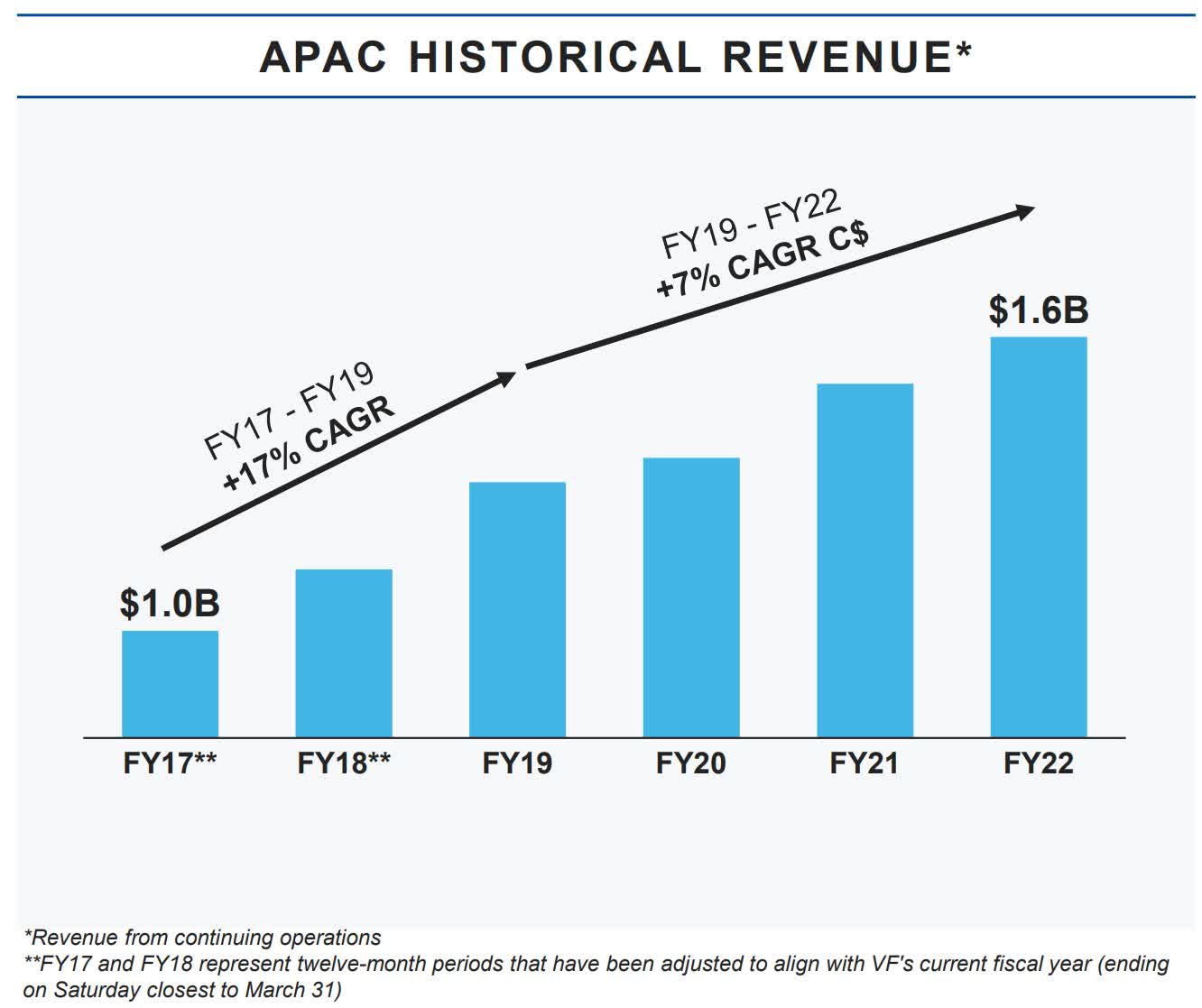

VFC Investor Day (Sept 2022)

The largest Asia-Pacific (APAC) constituent is China and as you see, growth there has been strong. Even though APAC represents less than 1/4th of the company’s total sales, it may once again become the fastest growing segment. As you see above, before Covid it was growing at a 17% CAGR.

Just 2 months ago they launched Supreme in China, which is almost certain to boost growth there.

The takeaway

With 49 years of dividend increases, a nearly 7% yield is a red flag for a company with such a stellar dividend history. While the payout ratio of 1.85 and other metrics suggest a cut is inevitable, I believe margins will normalize and we will see an increase at year 50 and beyond.

Be the first to comment