simonkr/E+ via Getty Images

Main Thesis & Background

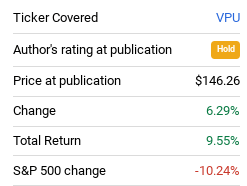

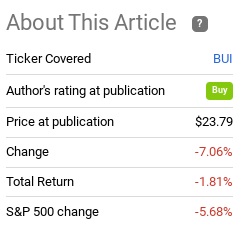

The purpose of this article is to discuss the Utilities sector as an investment option in 2023. This is an area I cover regularly and mostly focus on my two long-term holdings. These are the Vanguard Utilities ETF (VPU) and the BlackRock Utility & Infrastructure Trust (BUI). The timing of this review is relevant for readers who are thinking about if/when they should make portfolio changes this year – and especially for those who are considering an allocation to the Utilities sector.

VPU and BUI are both funds I covered at the beginning of 2022 and suggested them for core holdings. Since January, VPU has markedly out-performed the market and since March BUI has had a slight edge as well:

Fund Performance (Seeking Alpha) Fund Performance (Seeking Alpha)

It is due to this steady progress that I continue to hold each in my portfolio and I don’t see that changing at all this year. In fact, as I built up cash during market rebounds last year, I think I will beef up my positions in both of these funds on any upcoming down days in Q1.

I see quite a bit of merit to holding this sector: for income, dividend growth, as a broader equity market hedge, and relative stability. This is an often overlooked corner of the market but continues to be a space that investors can find both growth and safety in the current political and economic climate. I will describe why I feel this way in the following paragraphs.

A Top Notch Defensive Option

I am of the belief that most retail investors should use sector allocations to improve portfolio stability and for diversification. While buying the S&P 500 may give the illusion of diversification because it holds 500 companies, its market-cap attribute means that one holding that index is heavily exposed to a handful of names in the Tech sector. Even branching out into large-cap dividend or theme funds like “growth” or “value” offers investors little in terms of new exposure. In order to balance this out, I hold very specific dividend ETF (such as aristocrats) and also direct sector investing through the likes of VPU and BUI.

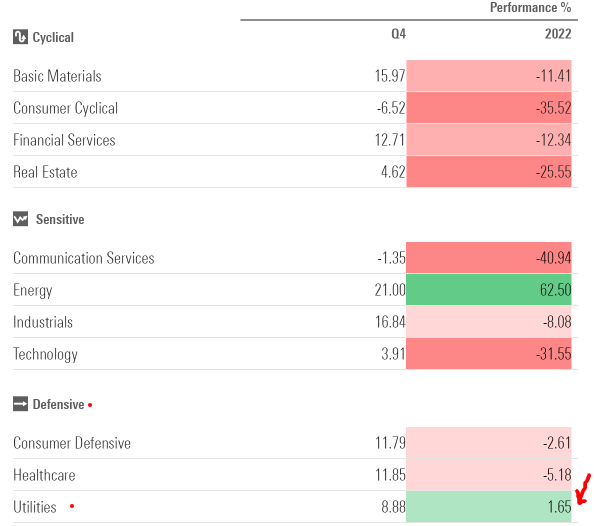

This strategy does not always work out as planned (i.e. in March 2020 when everything dropped!). But 2022 was a year where this strategy paid off handsomely. While my retail exposure suffered, my Energy holdings really delivered. Straddling the middle of the pack was Utilities, but that was a win in my view. While the sector only produced a modest gain, that compared extremely well with every other sector:

2022 Sector Performance (Morningstar)

A key takeaway for me was in particular how Utilities fared against other “defensive” sectors like Consumer Staples and Healthcare. Those sectors held up reasonably well, in fairness, but they still registered losses. Aside from Energy, Utilities was the only sector to end last year in the green and it had a nice spread over its defensive peers. This reiterates to me that the Utilities sector remains a classic way to “play defense” and should remain in my portfolio in 2023. I see growth challenges ahead and also a possible recession. So having this type of exposure will likely serve me and others well in the months to come.

Why Worry? Jobs, Earnings, Confidence

There is a lot of worry about these days. While not “good” for stocks as a whole, it could be a benefit for Utilities as investors look to shield themselves from further pain. The market could be due for a broad rebound given how poor last year was, and the first trading week did help us bounce off the lows. But I don’t think we are out of the woods just yet because some very fundamental problems remain.

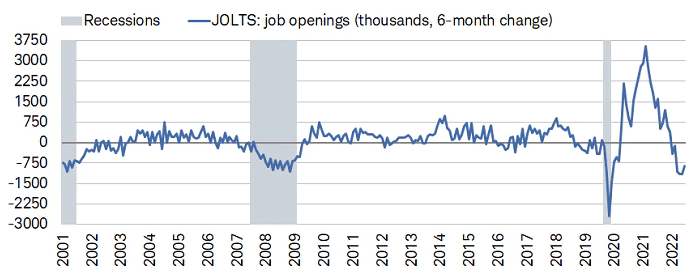

Taking them one at a time, let us first look at jobs. The challenge of hiring good employees remains ever present, but that backdrop is waning. Major layoff announcements have come out over the past few quarters and the excess labor pool is starting to balance out. A decline in job openings has often been correlated with recessions – so it is obvious to me one needs to be prepared for that in the near term:

Job Openings vs Recessions (Bureau of Labor Statistics)

The logic here is that as job openings slow, so do wage gains and purchasing power. This trickles down to discretionary sectors if sales and revenue slow along with household spending. After all, when one loses their job (or is unable to find a job) it is only natural to cut back on spending!

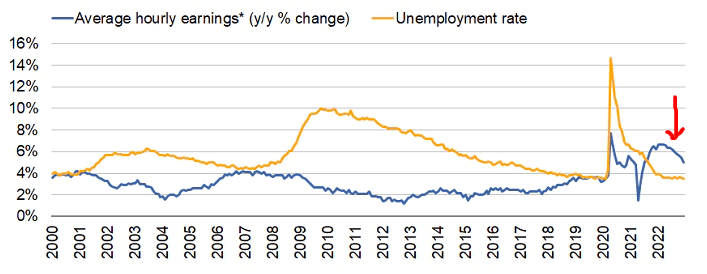

We are actually already starting to see this take place, albeit at a moderate pace. Wage gains are starting to reverse off their highs, although they are still in positive territory on a year-over-year basis:

Labor Stats (Charles Schwab)

This is not meant to be alarmist. The stubbornly low unemployment rate and general rise in labor force participation should prevent any recession from being too severe. There are still a lot of people earning a lot of money in the labor force. So I am not suggesting to sell-off all risk. But I am suggesting that the labor market is weakening and that means we should plan for some turbulence. The Utilities sector is unique in that it is fairly immune to economic conditions. Yes, people can stop paying their utility bills, but that is rarely a widespread trend – especially in winter!

The point of emphasis is that when I see macro-metrics rolling over – such as job figures or corporate earnings – then I see increased merit to owning the Utilities space. This is precisely the environment we are in at the moment.

I See Continued Government Support

Even with a changing Congressional make-up, I continue to believe that Utilities companies are going to enjoy federal, and possibly state, dollars on a sustainable basis. When we think of “renewable energy sources” being an emerging trend, we should realize that Utility companies play a key role in making this a widespread reality.

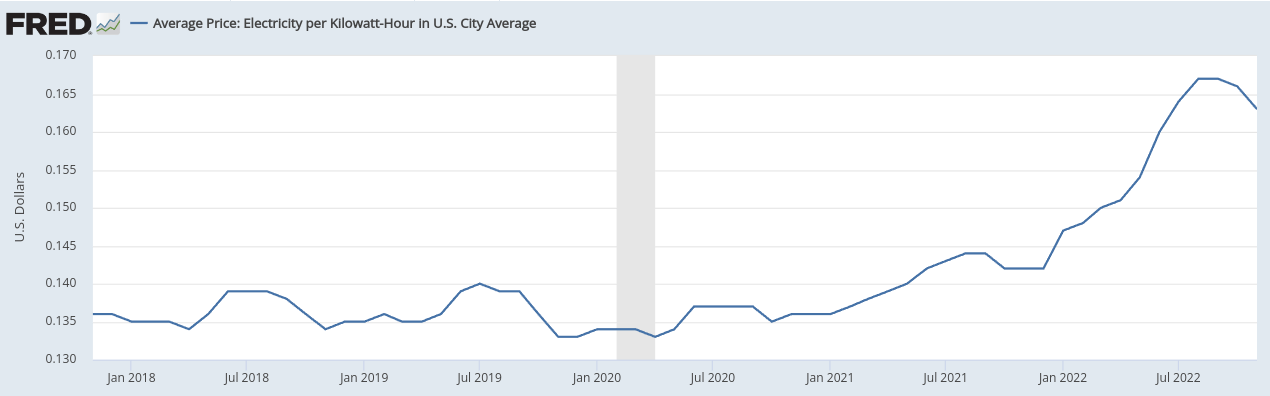

Generating power from renewable resources is now more economical than generating power from fossil fuels, so utility companies that adapt to this model are actually making more per share. This is coming at a time when utility rates continue their trend upward – so this is a win-win for investors:

Electricity Prices (US) (St. Louis Fed)

Another part of this story is that it is global. While the Inflation Reduction Act signed into law last year provided support to renewables, clean energy, and the Utilities sector more broadly, this was not the only action taken by developed governments. Major nations in Europe are increasing their budget’s allocations to utility companies at a fairly aggressive pace:

Government Support (EU) (ING)

I’m of the opinion that the Utilities sector will benefit from rising prices that they pass on to consumers, a willingness of the federal government to pump money in to the sector, and a backdrop of consumers and businesses who are seeking to reduce their carbon footprints in to higher margin renewables. While Utilities may have been “boring” in years past, they are anything but now, if you really focus on what is happening in the sector. This makes exposure to this area a no-brainer for me.

What About Interest Rates? I See A Peak Soon

One challenge for the sector to keep in mind is that it has historically been negatively correlated to interest rates. Over time, when rates go up, share prices go down in a similar fashion, and vice versa. However, 2022 bucked that trend. The Fed and other central banks were aggressively raising rates, but Utilities performed well anyway. This was due to a general risk-off mode, a search for reliable income, and government subsidies. All these outweighed the historical precedent we had seen for years.

But this trend may not last forever. Income-producing investors tend to decline when rates increase – just look at bonds. To suggest that Utilities can overcome this hurdle for years on end seems unrealistic. So that is a real risk.

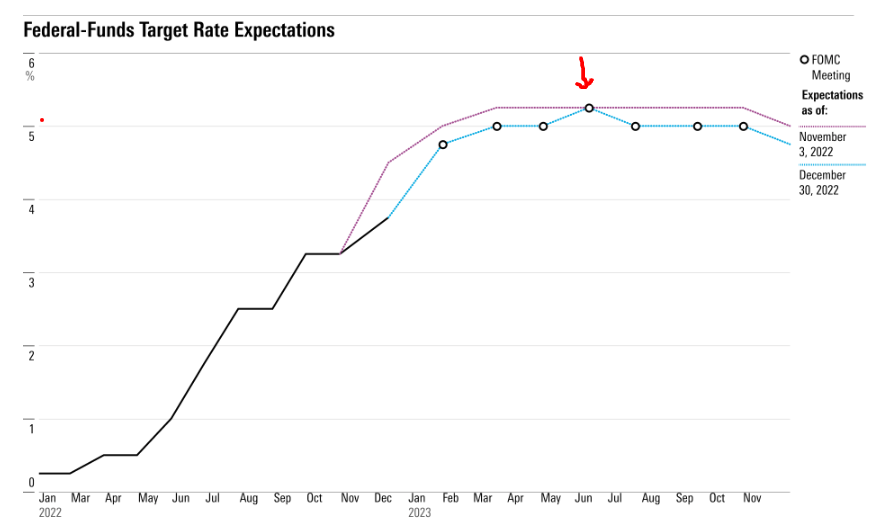

The good news is that rates may not be going up for much longer. This removes what I see as a critical headwind facing the sector. While the Fed is likely to keep raising rates in its next two meetings this year, that may be the end of it. Currently, the futures market expects the Fed to max out at around 5%, so that doesn’t leave much further to go:

Fed Rate Futures Outlook (CME Group)

The conclusion I draw here is that I am not too worried about rising rates anymore. The question really is how long with elevated rates be sustained. That is key to equity valuations across the board. But utility companies can adapt to that and higher inflation rates by passing on added costs (including higher borrowing costs) to end consumers. It is the prospect of rising rates that is really the headwind. As we near the end of that cycle, I see a stronger path ahead for the Utilities sector as a whole.

Don’t Be Blind To Higher Valuations

I have sounded fairly bullish on Utilities for this review and I do stand by that assessment. But I would caution readers not to get carried away. Do I see a path higher in 2023? Yes. Does that mean one should go “all in” at any price to get exposure? Absolutely not. We need to continue to be tactical about when we buy – this is not going to be a straight up across the board bull market.

The reason for this caution stems from the fact that the Utilities sector is by no means cheap. Its performance in 2022 resulted in the sector starting the year off at an elevated valuation level:

Historic Sector Valuation (Utilities) (Moody’s)

Has it traded higher in the past? Yes – but that doesn’t mean to be blind to this backdrop. Utilities could be ripe for a correction, especially if economic growth comes in ahead of expectations and the risk-on mode dominates equity markets again. In this case, investors will probably rotate away from Utilities and into sexier options. But this is not what I am anticipating and I continue to advocate increasing my allocation to VPU and BUI. But I will be tactical and patient and wait for weakness to add.

Bottom-line

There are a lot of options to bottom feed as we begin the new year. Most sectors ended 2022 in the red and many stocks were down by huge margins. This creates opportunity for those who want risk. I must admit, I am tempted by some relative value plays across a number of stocks and sectors. But that only accounts for a portion of my cash plans.

The other plan is to be defensive given the rising probability of a recession. This includes foreign stocks, muni bonds, and Utilities. This means I will be looking for opportune times to buy both VPU and BUI in the weeks and months ahead, and I encourage readers to give this idea some thought going forward.

Be the first to comment