fatido/iStock via Getty Images![]()

Investment Thesis

Uranium Energy Corporation (NYSE:UEC) is an incredibly attractive investment opportunity.

Here’s the one-line summary of the uranium case. Presently, uranium out of the ground is being produced at about 130 million lbs. in 2022, while the world consumed 180 million lbs.

Alongside this one-line summary, I must address why UEC out of all the potential investment options.

Because this US company is a pure-play miner that is fully unhedged. And as soon as uranium prices stay at $60 per lbs, this business will be restarted, and we’ll see its operating leverage sizzle, with strong free cash flows.

Why Uranium?

Uranium is a very exciting energy opportunity. This same sentence I could have written at any point in the past 5 years and at every point, at that time it would have sounded on point and insightful. And yet, that comment would have been proven false with time.

But I believe that now, in 2023, the landscape is different and the fundamentals are meaningfully improved.

Energy security in 2023 is a huge risk. It’s not just a buzzword. The geopolitical tensions of 2022 brought this crisis to the foreground. It may have been brewing in the past in the background, but now, energy demand is of the utmost concern.

Countries around the world are reassessing their energy requirements. These energy requirements need to fit 4 characteristics:

- Low-cost

- Highly scalable

- Flexible

- Reliable

Asides from fossil fuels, at this moment no other energy source apart from nuclear energy fits this framework.

The advantage of uranium is that it emits no carbon. The disadvantage of uranium is that it’s perceived to be dangerous. The problem with uranium is getting rid of the waste of uranium after it’s been used.

Even though the emission of used uranium is contained within the fuel rod, getting rid of the used uranium causes problems.

That being said, the advantages are tremendous. For example, uranium the size of your finger could power all your energy requirements for the whole of your life. That’s just such a huge untapped power source. Can you imagine the power?

Having described to you the need for energy, plus the appeal that uranium has over carbonizing fossil fuels, allow me to put forth why right now is the time to invest in uranium.

What’s Happening in the Nuclear Market Right Now?

Regarding uranium as a source of energy, attitudes have changed all across the world. Three nations from distinct continents are highlighted here.

- Japan is one example, given the population’s stigma post-Fukushima meltdown. Japan is restarting 3 of its reactors by the summer of 2023. With a possible 7 coming back online towards the end of 2023.

- The UK funded £50 million towards nuclear fuel projects. Even though it’s little, this represents a clear step in the right direction.

- The US has recently awarded funding to some companies to increase its reserve of strategic nuclear fuel.

I could go through all 3 case studies in more detail, but I believe that dissecting Japan is perhaps the most critical. Why?

Because Japan has made a 180-degree decision to restart its snowballed uranium reactors. This is a huge political movement to recognize that the stigma towards uranium post-Fukushima is overdone.

For me, Japan will be the poster child that European and North American countries will come to recognize realizing the benefits of uranium.

All that being said, Japan might be emblematic. But near term, the real bull cases lie with China. China is intent on running 3 new small nuclear reactors in 2023. With another 120 up and running by 2025. Put another way, China had nearly 23 GW of nuclear capacity under construction and 194 GW under development.

All in all, you can see that demand for uranium is going to go massively this year.

Why UEC in Particular?

There are 3 reasons why I’m bullish on UEC:

Firstly, the business carries no debt and $110 million of cash. However, keep in mind that this business has survived a nearly 10-year-long nuclear winter. There’s no ambiguity, to survive this long a bear market, you need significant business acumen. This long and challenging period has only allowed for the survival of the fittest.

Secondly, UEC has fully unhedged production. This consideration is different from Cameco (CCJ). While Cameco has a strong appeal, given Cameco’s size and widespread integration in the nuclear field (together with the 50% ownership of Westinghouse), Cameco is nearly all hedged out.

If you believe that nuclear energy has a promise alongside fossil fuels and renewables, then you don’t want to be hedged on nuclear. Or better said, I don’t want to be hedged. I want a fully committed pure play on uranium and that’s UEC.

Thirdly, the shareholders of UEC.

UEC SEC filings

Not only does management hold 3.7% of the company, but Rio Tinto (RIO) also owns approximately 4.2% of UEC. Rio Tinto is one of the biggest metals and mining businesses in the world. They would know a quality asset when they see one. In fact, Rio Tinto actually sold Roughrider to UEC.

Furthermore, Roughrider deposits hold around 4.5% grade. This compares with grades of around 1% to 2% around the world. By far, some of the best uranium deposits around the world. Essentially, enriched uranium will mean higher profits.

The Bottom Line

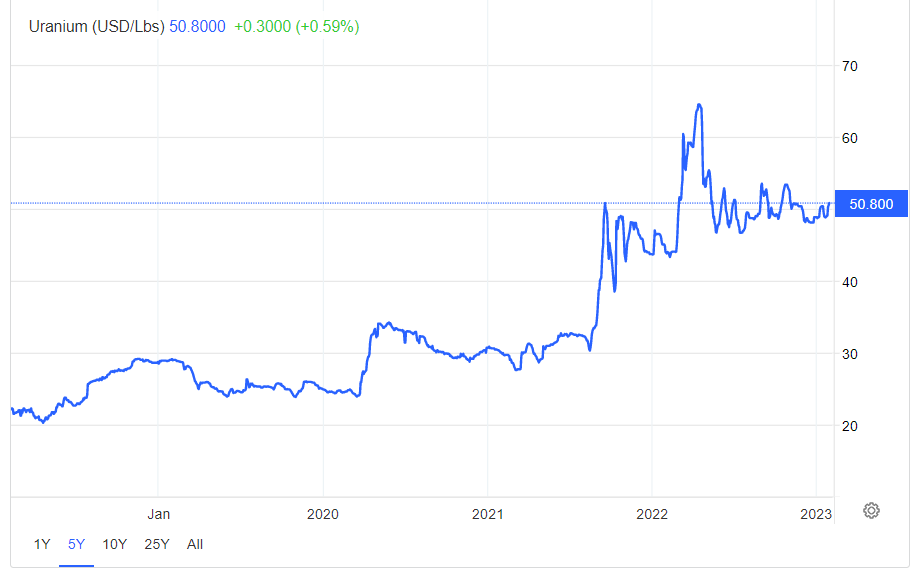

UEC right now has snowballed its operations and is waiting for uranium prices to stabilize at $60 per lbs. Presently, uranium is at $50. But as the graph below shows, it’s only an amount of time until uranium prices reach $60.

Trading Economics

I strongly believe that anyone reading this should seek out a small proportion of their portfolio towards uranium. You don’t have to go with UEC. The Sprott Physical Uranium Trust (OTCPK:SRUUF) could also be attractive for investors that want to sleep well at night.

In conclusion, uranium will be essential for meeting the world’s energy needs. And UEC is in a fantastic position to meet this demand.

Be the first to comment