kevinjeon00/E+ via Getty Images

United Rentals (NYSE:URI) has been a solid performer over the long-term. The stock is up over 400% since I first covered it back in 2014. I expect the company to continue its market outperformance over the long-term. The valuation remains attractive and the future growth looks promising. The reinstated stock repurchase program is icing on the cake to help drive the stock’s performance.

Strong Q4 and Full Year Performance

United Rentals’ recent performance demonstrates how the company is performing well in an economy that could see a recession this year. The stock itself increased 36% over the past 12 months while the S&P 500 (SPY) declined 7% over the same time period. The company’s Q4 results show United Rentals’ ability to be resilient in this economy.

United Rentals reported the best full-year financial performance in its history in 2022. Revenue increased 19.8%, gross profit increased 29.7%, and net income increased 52% in 2022 over 2021. The results for Q4 were also strong with a revenue increase of 18.7%, gross profit increase of 28%, and net income increase of 33%.

The company attributes its success on giving priority to customers’ needs. At the same time, United Rentals focused on leveraging its growth while maintaining cost discipline. This combination allowed gross margin [GM] to increase from 40% in 2021 to 43% in 2022. The GM increase was achieved even during a period of high inflation, which was impressive. The company also achieved a record return on invested capital [ROIC] of 12.7% at year end.

United Rentals decided to reactivate its share buyback program. URI plans to repurchase $1 billion worth of stock in 2023. The company also plans on paying $5.92 per share in dividends this year. That’s about a 1.4% yield based on the current share price.

Future Growth Catalysts

United Rentals has multiple tailwinds that are likely to act as growth catalysts for continued positive momentum. One positive is the growing contractor backlog that the company is experiencing. Employment reports indicate that contractors are in expansion mode and are hiring. The company is seeing strength in commercial construction. This includes new plant construction in automotive, batteries, petrochemicals, and semiconductors. There are also multi-year projects in healthcare and education.

Another potential growth catalyst is the Ahern acquisition. United Rentals completed the Ahern acquisition on December 7, 2022. Therefore, the company will benefit from a full year of accretive growth in 2023 from Ahern.

The acquisition gives United Rentals an additional 60,000 rental assets, 106 locations, and 2,100 employees. Ahern gives increased capacity for United Rentals to better serve its customers. United Rentals had 1,020,000 total equipment units and 1521 rental locations at the end of 2022. United Rentals is the largest equipment rental company in the industry with a 17% market share (which includes the Ahern acquisition).

United Rentals has a solid track record of acquisitions for increased capacity and add-on growth. I expect this to continue over the long-term as the company continues its growth strategy.

Valuation & Expected Growth

United Rentals is trading with a forward PE of 11.2 based on expected EPS of $38.85 for 2023. It is also trading at 10x expected EPS of $43.74 for FY24. The company is expected to grow earnings at a strong pace of 19% to 20% in 2023 and 12% to 13% in 2024.

The PEG ratio which accounts for the expected average annual EPS growth of about 20% over the next 3 to 5 years is 0.76. This is an attractive level as it sits below one. Usually, the growth stocks that I cover trade with a PEG between one and two which is considered a reasonable valuation. To see a strong growth company like United Rentals with a PEG below one, is a beautiful thing.

It’s important to note that analysts’ earnings estimates have been upgraded over the past 3 months for both 2023 and 2024 for United Rentals. The current estimate for 2023 is about 14% higher than 3 months ago. The current 2024 estimate is 12.6% higher than 3 months ago. This should act as a positive catalyst heading into the next quarterly report.

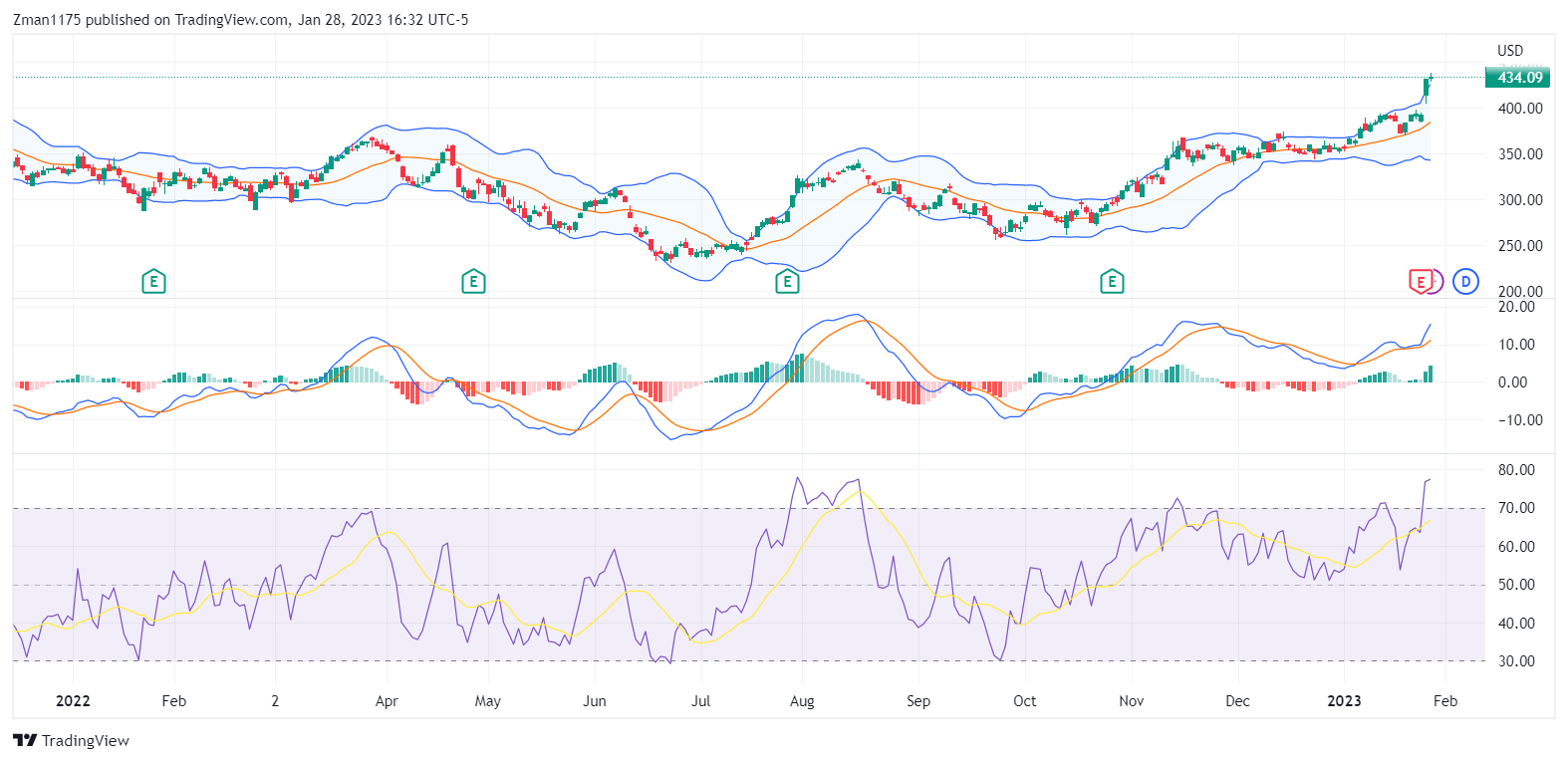

Technical Perspective

tradingview.com

The main issue that I see with United Rentals is that the stock is currently overbought on the daily chart according to the purple RSI indicator at the bottom. With the RSI level above 70, the stock could pullback due to profit taking. Personally, I would wait for a more attractive technical entry point before starting a position. The Federal Reserve meeting on 1/31 to 2/1 could lead to a market selloff depending on what actions are taken and what is said about future interest rate hikes.

Balance Sheet

The good aspect of the balance sheet is that URI has 1.1x more current assets than current liabilities and 1.4x more total assets than total liabilities for shareholders’ equity of $7 billion.

The negative aspect of the balance sheet is the company’s ratio of total cash vs. total debt. URI has $106 million in total cash and $12.2 billion in total debt. The company’s equipment is expensive. So, URI tends to run with a high amount of debt. This would be a risk if the company ran into a significant business decline. However, the company’s current outlook has been positive with a strong backlog.

URI’s strong operating cash flow of $4.4 billion helps in handling the high amount of debt. It is important to point out that the company issues new debt on an annual basis that is sometimes more than the amount of debt that is paid off. That was the case in 2022 when URI issued $9.8 billion in new debt and paid off $8.2 billion of debt. The high amount of debt is United Rentals’ biggest weak point and risk in my opinion.

United Rentals Long-Term Outlook

URI has an attractive low valuation with strong, above-average expected growth for the next 3 to 5 years. United Rentals has positive business momentum for its rentals for the foreseeable future from what the company stated in the Q4 conference call. This evidence points to the likelihood that the stock can outperform in 2023 and beyond.

The main risk for the company is that a significant recession could lead to delays and/or cancellations of major construction projects. If this were to happen, URI’s high debt could become a burden. United Rentals should be able to weather a recession well due to the diverse industries that it serves, some of which are not highly economically sensitive.

Given the overbought level of where the stock is trading, I would wait for a better entry point on a market pullback before starting or adding to a position.

Be the first to comment