We’re just a few trading days away from 2023, so it’s time I give you one of my favorite stocks. Given my view on economic growth developments, the Federal Reserve, and the stock market, I believe that we’ll get the opportunity to buy some terrific stocks at great valuations in the next year. One of the companies I want to invest much more money in is Union Pacific (NYSE:UNP). America’s largest public railroad has recently enjoyed much coverage as people have finally figured out how much value there is in good old railroads. The company used to be a top 2 position of mine. Now, it’s number 5, as a result of outperforming defense and energy stocks – two sectors I have invested heavily in.

It also does not help that economic conditions are deteriorating. I would make the case that a recession is a done deal, with more weakness ahead, as the Fed seems eager to tighten into a slowing economy.

While that’s bad news for my net worth (at least temporary), I’m quite happy that I might get a realistic shot at buying more UNP shares with a yield close to 3%.

So, let me give you the details!

More Weakness In 2023(?)

I just wrote my 2023 outlook, which includes my macro view and investing strategy.

As it’s a long one, let me share one of the most important parts with you where I explain why I believe that an aggressive Fed will be a driver of significant economic weakness in the first quarters of the upcoming year:

– The Fed is feeling tremendous pressure to control inflation. That makes sense as the US economy is consumer-driven. Also, high inflation can quickly turn into lasting above-average inflation once wages and spending habits adjust. That’s a no-go!

– Hence, I believe that the Fed will not be scared to do damage to the US economy to achieve its target of lower inflation. This includes hurting housing demand/prices, unemployment, and consumer spending.

– Once the Fed pivots (I still believe it will happen in 2023), the economy will slowly adjust to lower rates. Demand will come back. So will inflation.

– Given the aforementioned secular factors, I believe we are in a prolonged period of Fed hikes and cuts at above-average rates (versus 2009-2021).

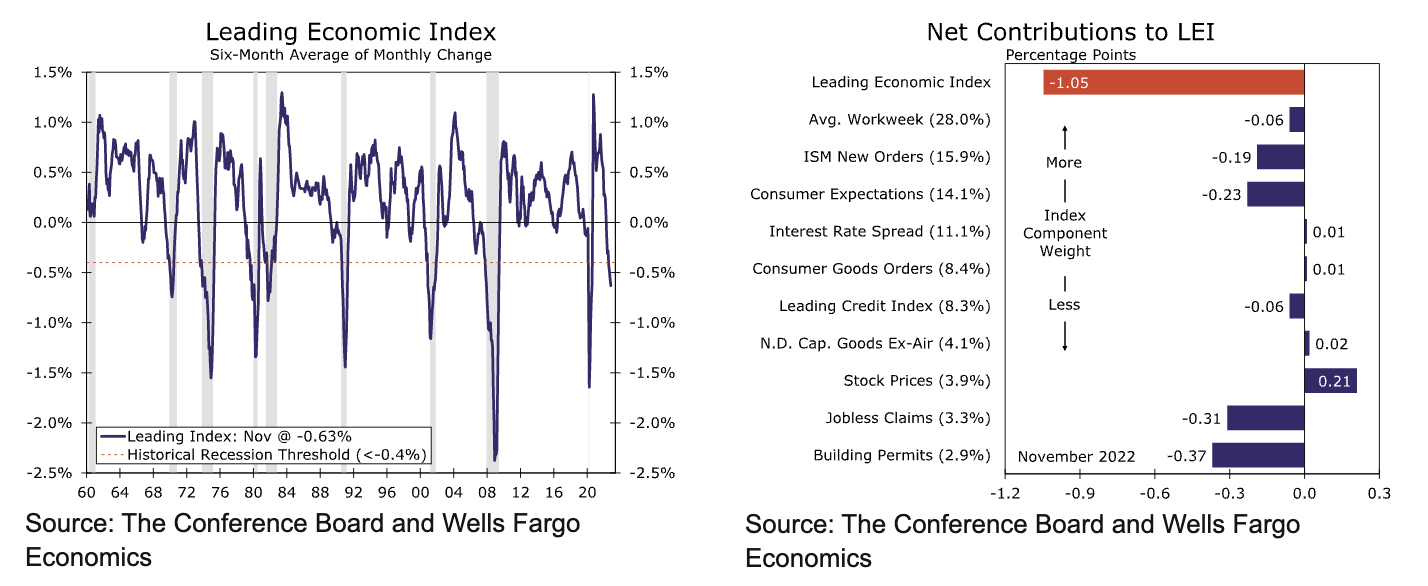

While I am writing this, an increasing stream of bad economic news is coming in. The LEI – leading economic index – is now at one of the lowest points since the Great Financial Crisis, as a result of weakness in consumer and manufacturing expectations impacting jobs and housing.

Wells Fargo

As I wrote in my outlook article:

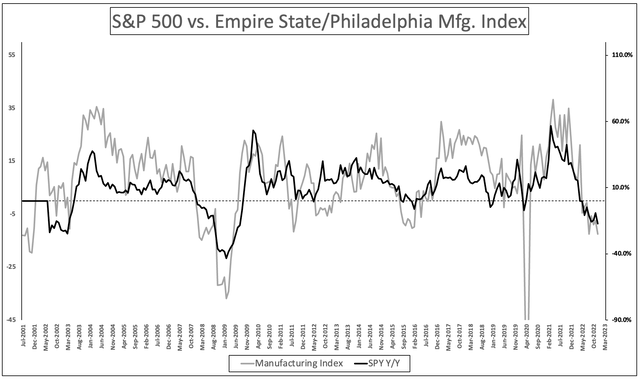

[…] the market is still driven by economic expectations. The S&P 500 continues to follow leading indicators like the Empire State and Philadelphia manufacturing surveys. And, for now, it looks like the economic downtrend is going to continue in the first months of 2023.

Author

Moreover, unlike during the manufacturing recession of 2014/2015, we’re now dealing with broad weakness. This is what Wells Fargo said after digesting the aforementioned LEI indicator:

Consumer expectations continue to be a major source of weakness on the overall index, but the ‘largest drag’ title goes to building permits in November. The 0.37 percentage point drag in this component marks the largest since the depth of lockdowns in April 2020, consistent with the pullback in housing activity more generally.

However, one thing is different. Unlike in 2014/2015, we’re now in a situation where commodity prices are strong. Inflation is much higher. This benefits cyclical value stocks like industrials (Union Pacific is also an industrial company).

Despite investors pricing in a recession, industrial stocks have erased the entire underperformance versus the S&P 500 that occurred after the first wave of lockdowns. When including dividends, industrial stocks are now outperforming the market since late 2019.

TradingView (XLI/SPY Ratio)

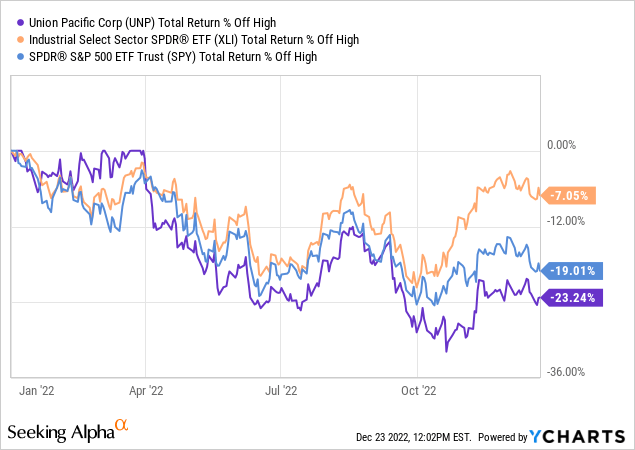

Unfortunately, relative strength can still mean weakness. While industrial stocks are down 7% from their 2022 highs, Union Pacific is down 23%.

However, it offers opportunities that investors like me need. As a long-term investor with an owner mindset, I love a good bargain.

Union Pacific Offers Value & Growth

In October of this year, I wrote a bullish Union Pacific article. Back then, the market had tanked, offering investors great opportunities. Because I had added to my other rail holding Norfolk Southern (NSC) at that time, I did not buy more Union Pacific shares. The stock is up 13% since then.

I’m not saying that to brag (it’s hardly something to brag about), but because it seems that the rebound was purely short covering and pricing in a lower Federal Reserve terminal rate. Back then, the terminal rate was expected to be 5.25%. Now it’s 5.00%.

Moreover, the market priced in the news that labor strikes have been avoided as railroads and unions – with support from the White House.

With that said, one of the many reasons I like Union Pacific is because of its terrific performance. Past performances do not guarantee any future results, but if we research why these results happened, it gives us an edge.

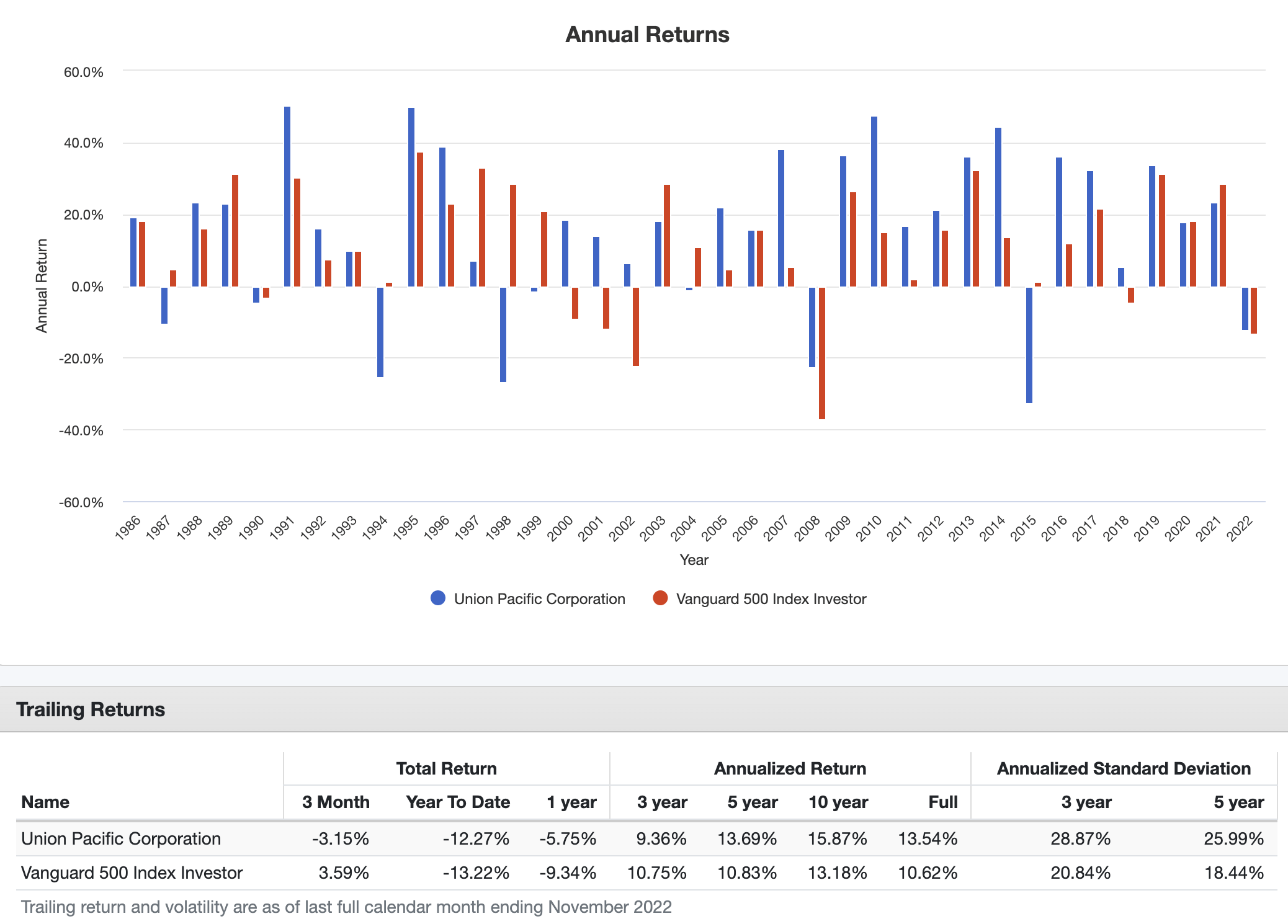

Since 1986, UNP shares have returned 13.5% per year, including dividends. During this period, the stock had a standard deviation of 23.8%, which is a decent number for a cyclical stock. Moreover, while UNP struggled to keep up with the market over the past three years due to the pandemic, it has consistently outperformed the market with a standard deviation of roughly 800 basis points higher than the market standard deviation.

Portfolio Visualizer

What makes UNP so powerful is the fact that it’s a perfect mix between value and growth.

Union Pacific is a company whose history goes back to 1862. Yet, it’s still a dividend growth stock.

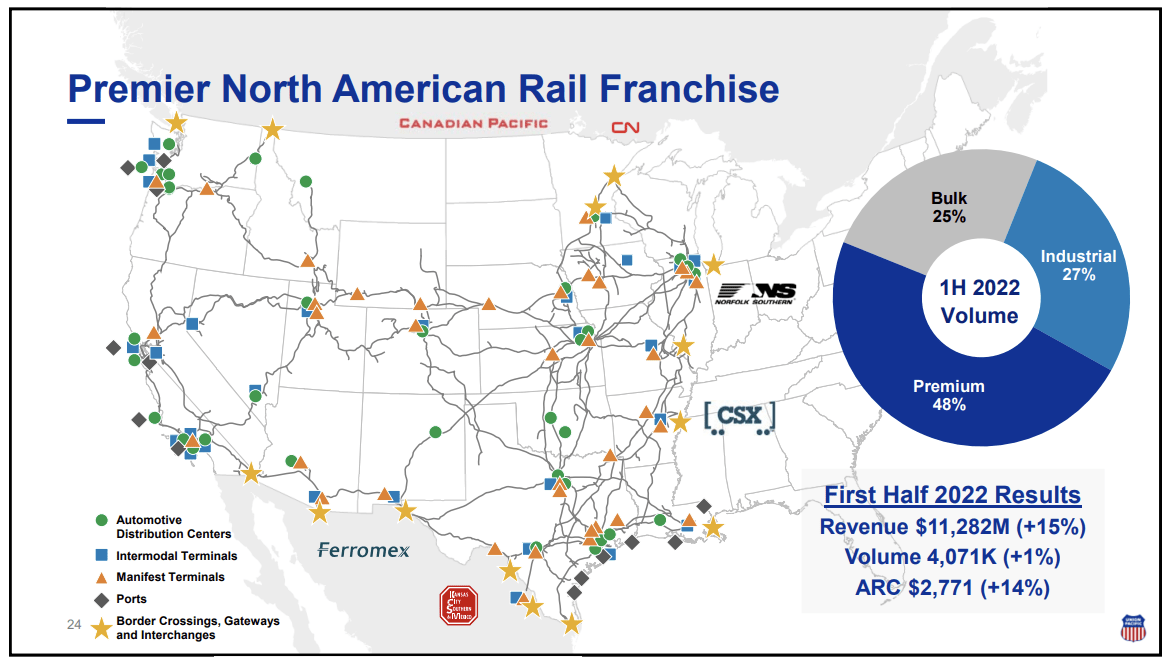

Union Pacific

Combining all major economic hubs, ports, and borders in the East, Union Pacific has become the backbone of the economy. As the map and data above show, the company has a large footprint in industrial goods, premium like intermodal and cars, and bulk products including grains, fertilizers, and coal.

One of the reasons why an old railroad like UNP was able to do so well is its focus on efficiency. Thanks to precision railroading, trains have become longer, allowing railroads to get more done with lower employee and equipment numbers.

[…] shifts the focus from older practices, such as unit trains, hub and spoke operations, and individual car switching at hump yards, to emphasize point-to-point freight car movements on simplified routing networks. Under PSR, freight trains operate on fixed schedules, much like passenger trains, instead of being dispatched whenever a sufficient number of loaded cars are available.

This year, however, PSR has run into some issues. Railroads had to deal with the return of volumes after the pandemic. However, almost all railroads had cut staffing and equipment expenditures, which resulted in delayed freights, unhappy customers, and a lot of complaints.

Hence, this year, the operating ratio (how much it costs as a % of total revenues to operate the railroad) is expected to end the year at 60%. Going into this year, Union Pacific expected that number to be 55.5%. That’s a huge deal! For example, this year, the railroad is expected to do $25.1 billion in sales. A 55.5% operating ratio would have resulted in $11.2 billion in operating income. A 60% OR will lower that number to $10.0 billion – a 10.4% difference.

The good news is that UNP is making good progress in hiring new employees, which will make it possible to push the OR to the mid-55% range in 2023.

That’s not an official company estimate for 2023. Union Pacific is not yet commenting on its 2023 outlook. However, it believes there are opportunities to lower the ratio to its 55% target.

So we are still very confident that we can get back to that 55 target. We’ve not set a date on that, but we would look to make progress, obviously, starting next year. In terms of the levers that help us achieve that, it’s the same levers that have gotten us to this point. It’s volume, it’s price and it’s productivity.

This brings me to another reason why UNP is so powerful. Thanks to its balanced product portfolio and contract structure, it has strong pricing power. Roughly a third of its contracts are shorter than one year. 45% of contracts are long-term contracts. 25% are tariffs.

When adding fuel surcharges, the company has consistently achieved pricing dollars in excess of inflation dollars.

Moreover, the company is keeping capital investments in check. Between 2018 and 2022E, the company is consistently spending close to $3.2 billion in CapEx. 2022 is expected to be $3.4 billion as a result of bringing operating efficiencies back on track.

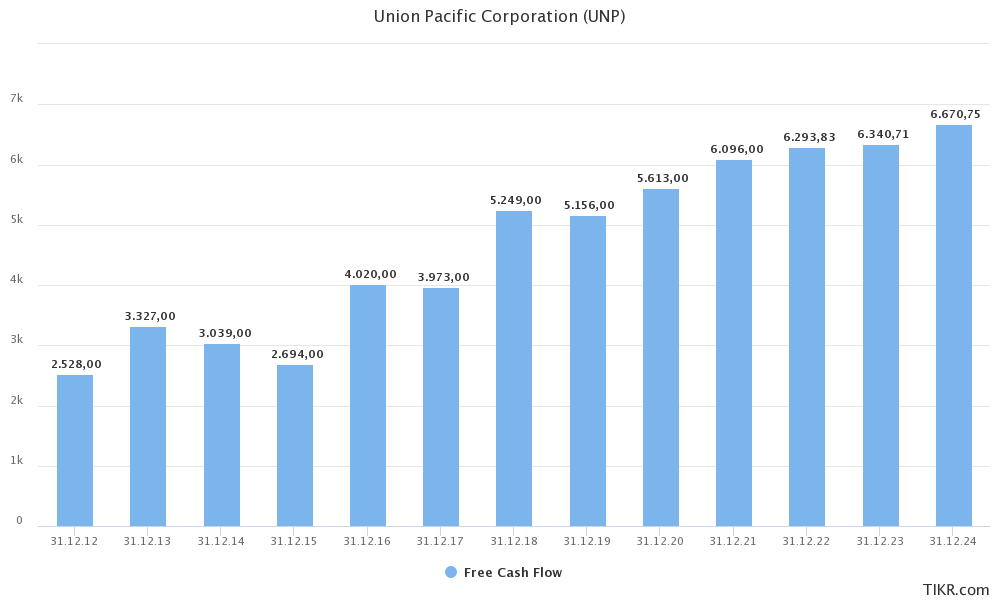

As a result, the company is growing free cash flow by 8.4% per year (compounded annual growth rate) in the 2012-2024E period. That is a lot for a mature company like UNP.

TIKR.com

It’s also terrific news for the dividend.

The UNP Dividend

UNP’s dividend policy is straightforward. It engages in consistently rising quarterly dividends and buybacks to distribute excess cash.

Our next priority is our dividend. And so we have a dividend target of 45% that we think is appropriate for our business. We want to be able to give our shareholders that you know, more certain return on cash. And then the excess cash is where we use it for share repurchases. And what that has historically meant is not only use of excess cash from operations but also using our balance sheet.

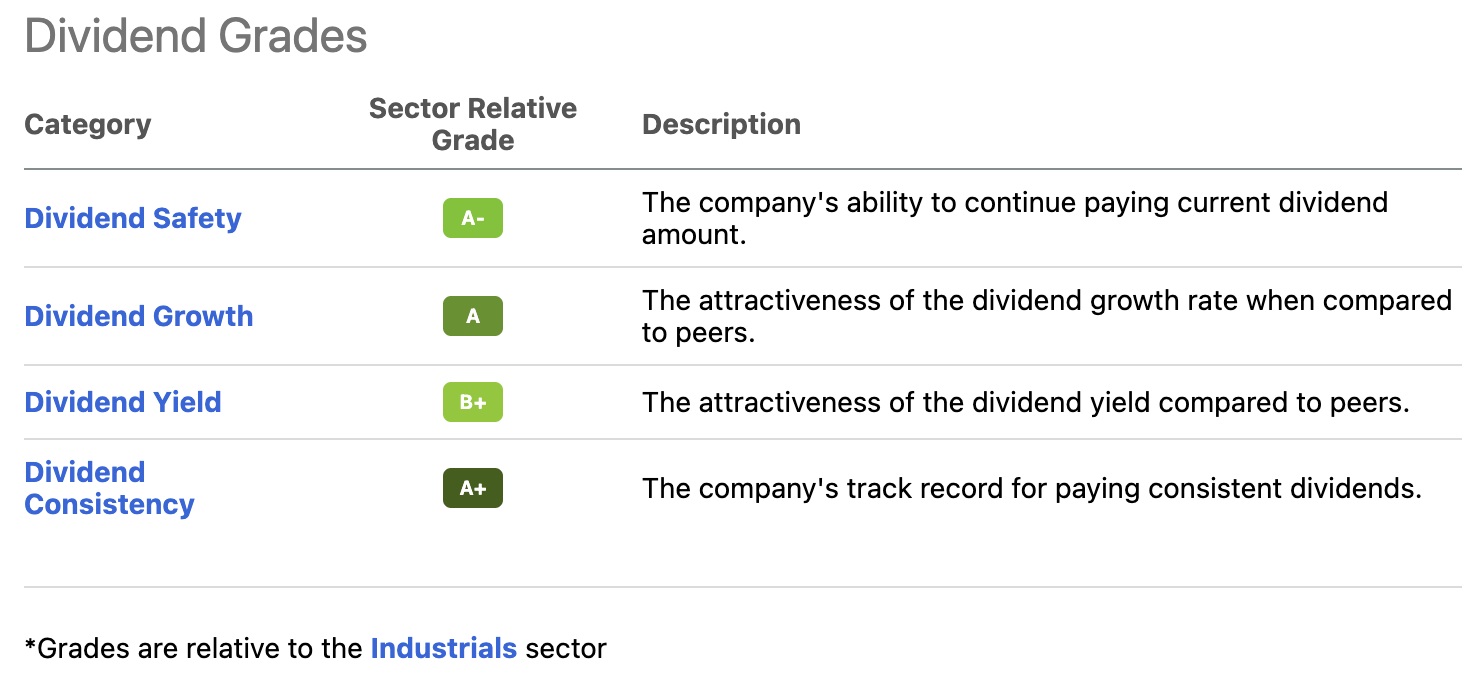

When looking at the Seeking Alpha dividend scorecard, we see that UNP scores high on safety, growth, yield, and consistency.

Seeking Alpha

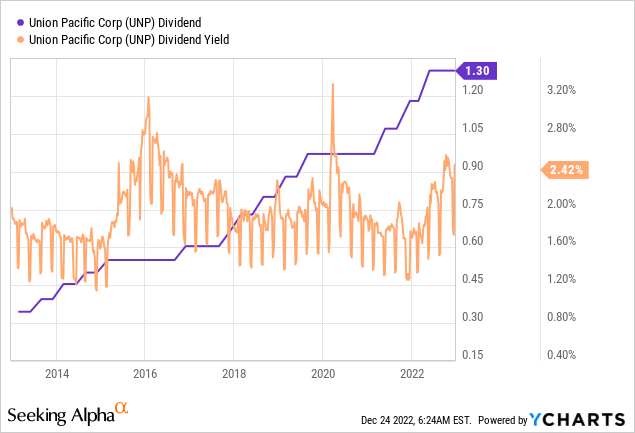

The company’s current yield is 2.50%, which is based on a $1.30 per share per quarter dividend. This yield is now close to the upper bound of the 10-year range if we ignore the outliers during the 2015 manufacturing recession and the COVID sell-off. Both share price declines pushed the yield to more than 3.0%.

This dividend has grown by 15.1% per year over the past ten years. Over the past five years, that number is 15.4%, indicating that we’re not dealing with a slowdown. However, I do expect the dividend to slow a bit in 2023 (and maybe 2024), depending on the severity of the recession.

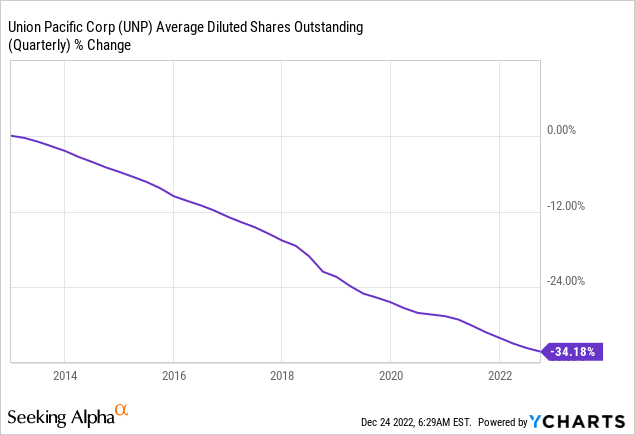

Moreover, since 2012, the company has repurchased more than a third of its shares outstanding, which has helped to beat the market.

While I understand that some investors require a higher yield, I believe that the UNP yield is attractive.

Moreover, if we assume that the company hikes by another 10% in 2023 and that economic weakness could further hurt the outlook, I think the odds are in our favor when it comes to buying UNP with a 3.0% yield again.

Valuation/Balance Sheet

In the UNP dividend quote I shared in this article, the company admits to using its balance sheet to buy back shares. The quote below shows what was said after that:

And so we have since 2018, you know, we put forth a new target that we were going to increase the leverage on our balance sheet, and that has been a big sustainer of some of those share repurchases.

So we’re at a point today where I would say the balance sheet is largely optimized. So as we generate EBITDA, that generates additional capacity on the balance sheet and obviously, generating EBITDA, generating more operating income and cash. So those are the levers that we look to and the priorities that we put to it.

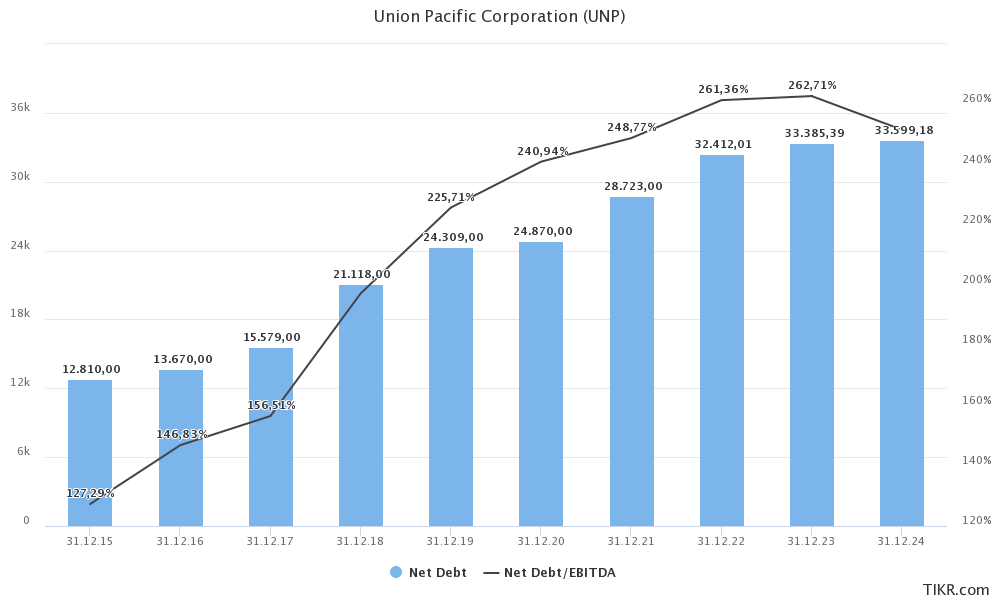

Prior to 2018, the company had a leverage ratio of less than 2.0x EBITDA. That number is set to increase to 2.6x in 2022, which is still sustainable.

TIKR.com

The company has an A3/A- balance sheet.

In early 2023, the company will work on its outlook, which includes setting targets for buybacks.

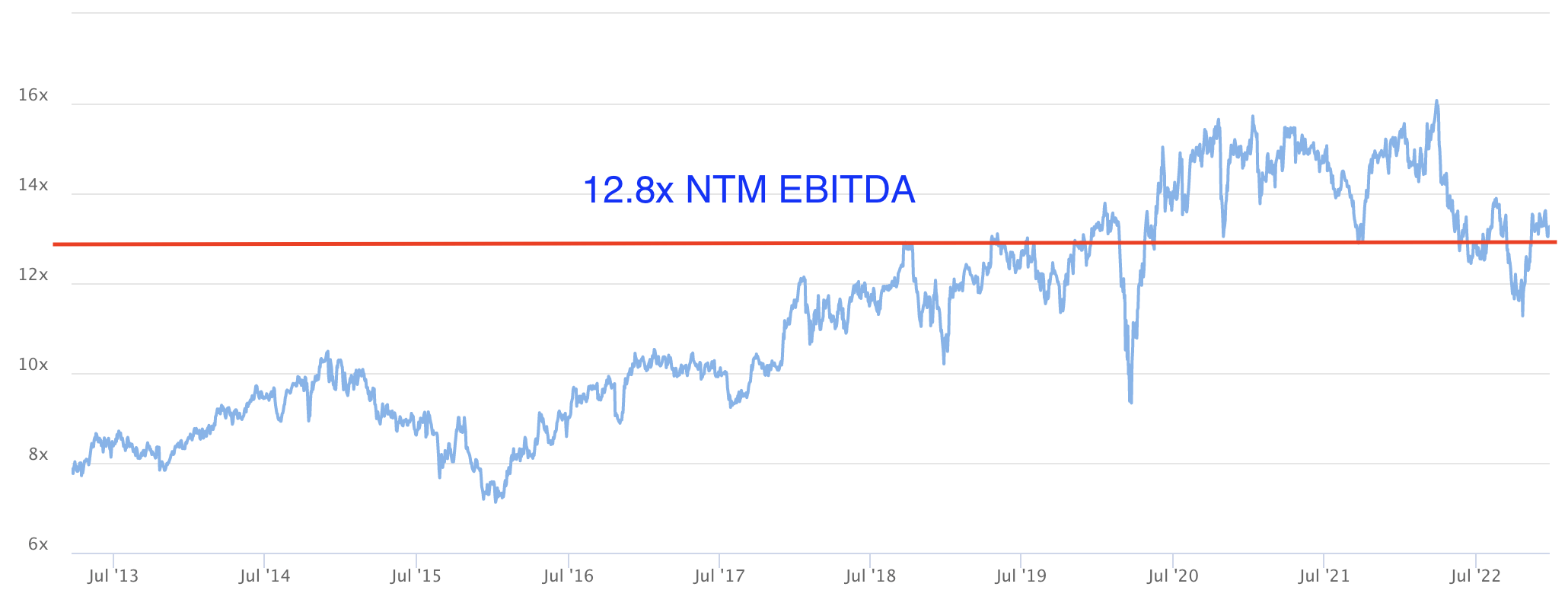

With that said, UNP has an enterprise value of $163.0 billion. That is 12.8x its 2023E EBITDA of $12.7 billion. This valuation has increased from 11.5x in October due to the stock price surge and lower EBITDA expectations. 2023 EBITDA estimates are down from $13.1 billion.

TIKR.com

That valuation is fair, but I have a strong feeling (based on everything we discussed so far) that we might get a better valuation.

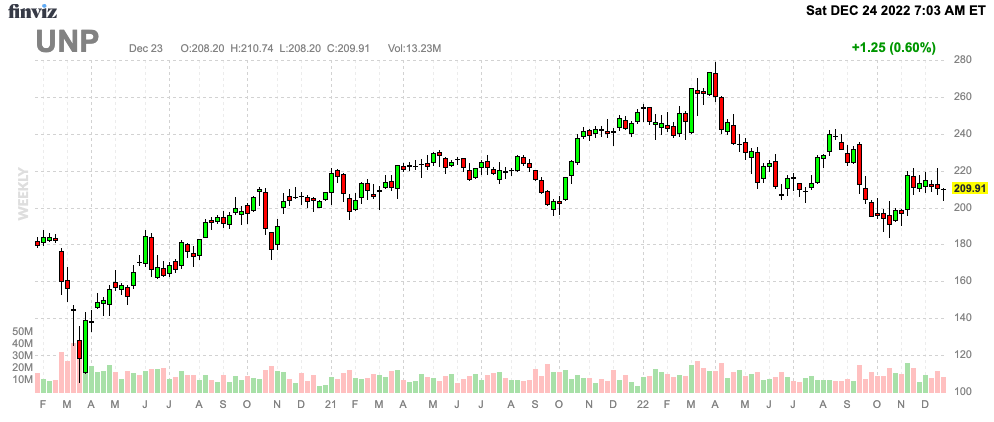

I will likely buy more aggressively if the stock falls to the $180-$190 range. The only reason I didn’t buy more UNP shares in October is the fact that UNP is already a large part of my portfolio, which required some diversification.

FINVIZ

However, given the company’s qualities as a dividend stock and the high likelihood of more economic weakness, I’m quite excited to buy more in 2023.

Takeaway

In this article, we discussed the high likelihood of more economic weakness in 2023. The Fed will have to keep fighting inflation, even as we have already entered an economic downswing with an almost certain recession.

While that won’t be a lot of fun for my portfolio, it is great news for long-term investors looking to buy value in 2023.

One of my all-time favorite dividend stocks is Union Pacific. The company offers a decent yield of 2.5%, fantastic (historic) dividend growth, and the ability to protect investors against high inflation.

While challenges persist, I have no doubt that buying share price weakness will continue to be a winning strategy.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment