David Dee Delgado/Getty Images News

I first wrote about Ulta (NASDAQ:ULTA) back at the end of 2019. If you had told me then what was coming, I may not have been as bullish in the short term as I was. However, I still would not have doubted the long-term power of the business. Needless to say, the thesis worked out:

Seeking Alpha Company presentation

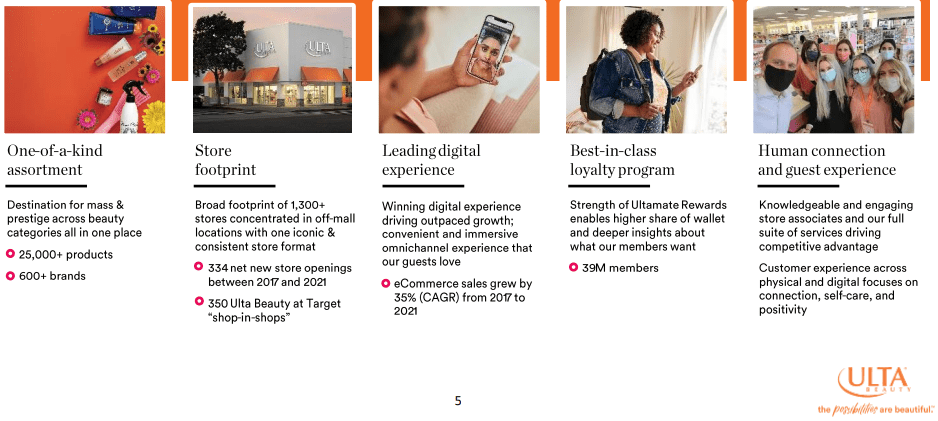

Ulta’s brand power has really changed the face of beauty retail in America. The company remains entirely US-based, for now, despite plans for a Canadian expansion scrapped just before the pandemic. The company’s loyalty program is among the best in the business, which is a common them among the market-leading retailers I cover. At 39M members as of last update, membership grew 9% YOY and covers in the ballpark of a quarter of all women in American. This cohort drives 95% of sales and averages $200 of spend per year. The data and marketing advantage this program drives are invaluable to the company and yield a competitive advantage.

Based on the way beauty product sales work, the nicest brands have the power, and choose where their products are sold. These prestige brands are selective, and the relationships built over time prevent upstarts and some e-commerce companies from gaining access to sell the brand. At first blush, this doesn’t make economic sense. However, for luxury products, image is everything. This give Ulta the closest thing to a moat many retailers can build.

Company presentation

Although Ulta can be considered an omni-channel company, the brick-and-mortar stores remain the ultimate focus. The average customer wants to see the products, sample them, and discuss their purchases with a sales associate. The company derives around 24% of its revenues from e-commerce today.

With that, management has pushed initiatives to improve online product discovery, like being able to search by style, scent profile, etc. However, it’s difficult to see online-native retailers ever fully taking over Ulta’s position. After the washout of the last decade among much of retail, the remaining successful companies share some insulation from e-commerce. In Ulta’s case, it’s that customers don’t want to play trial-and-error with $70 bottles of makeup and skincare products.

The company’s store footprint sits at around 1350 today. In 2021, 44 new stores were opened, 7 were relocated, and 9 were remodeled. There was a period of rapid store growth, which is likely behind the company. Most markets in America have some access to an Ulta, so future growth will likely come from newer store formats, new market entries, and fewer of the existing store format openings. It appears the company is making the right moves to keep its store formats fresh for shifting consumer demand, as most recently skincare was moved to the front of new stores based on its higher growth compared to the other segments.

Part of what sets Ulta apart from the other physical retailers is the size of the store. The footprint is much larger (generally at least twice as big), giving Ulta considerable flexibility to maintain large inventories, a superior selection, and shift product mix around based on demand. With that, the company does operate salons in many stores. They only bring in 3% of revenues with 8,000 stylists on the payroll, but the customers who get their hair done at Ulta visit the store more frequently, buy something 50% of the time, and spend on average 3X as much. Management is leveraging its CRM capabilities to maintain brand loyalty among these customers, and is making efforts to retain top stylist talent.

One newer initiative to watch for investors is the launch of the Target (NYSE:TGT) locations. These are smaller, and built inside Target, similar to what Sephora is doing with Kohl’s (KSS). So far, most management discussions have centered around the benefits Ulta gains from new memberships in these stores, with the ultimate goal of bringing those members to a full-sized location. However, I remain skeptical about the new format’s operating metrics, based partly on the discussion above concerning Ulta’s advantages in their larger formats.

Company presentation

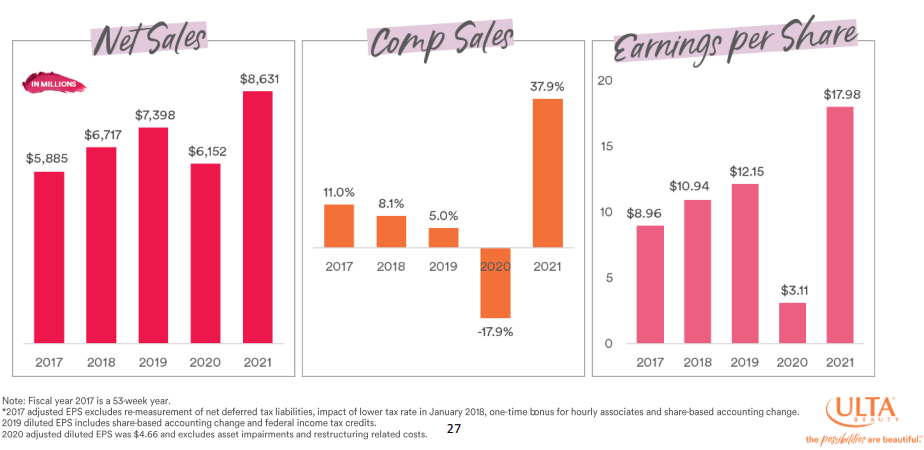

Looking at key financial metrics, Ulta broke a 20 year streak of same store sales growth due to Covid. However, the next year’s bounceback put overall growth over those 2 years to around 13%. They lapped it with an additional 14.6% in the most recent quarter. Key points inside that metric were 5% from price increases and 3.5% from ticket growth.

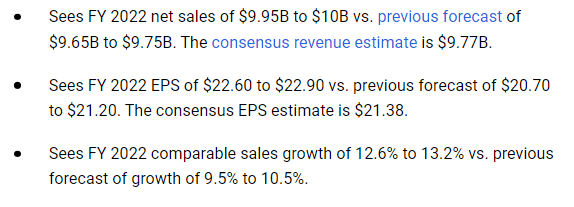

In the most recent quarter, revenues were up 17.2%, operating margin was relatively stable at 15.5%, and earnings per share shot up 35.5%. As mentioned above, skincare was especially strong, but the company drove growth across the board. Management raised guidance for full FY 2022 across the board, which is great to see:

Seeking Alpha

However, guidance remains about the same at 5-7% sales growth and low double digit EPS growth over the next couple of years. Here’s some perspective from the December 1st earnings call:

So again, big picture, let me just lay out a couple of the bigger variables here as we’re thinking about modeling for next year. So again, back to what we referenced in the script, we do expect we can grow sales next year in line with our longer-term 3% to 5% comp target. So on the top line, merchants have done an outstanding job. We feel good about the queue for newness next year. We’ve got some great things lined up. But we’re going to be lapping over some extraordinary newness this year, right, with these leading brands in each of our key categories, Fenty and makeup, Drunk Elephant in skincare and Olaplex in haircare, all right?

Price increase is another major lever. So we’re kind of in uncharted territory right now, right? The percentage of our assortment where we’ve seen increases and the depth of those increases is something we’ve never experienced in all the years here at Ulta Beauty. So we’re going to be cycling over some of that next year, and it’s kind of yet to be seen how the consumer is going to react to that over the longer period of time. So elasticity and resilient, while it’s been resilient so far, there’s a question of how far we’re able to push this without seeing some kind of impact.

There is always a concern for comps on the company’s revenue growth, considering Ulta gets about 20-30% of revenues each year from new products. However, over time, there has been enough shift in the product mix that the company has kept up with their targets.

The main risk to consider here over the longer term is the general lack of switching costs in retail. Despite the loyalty program, management projects only about 30% of a customer’s beauty spend goes to Ulta. Retail can be very price or brand-driven, and if a customer finds a product they like, there is zero friction for them to shop around and find it elsewhere.

Company presentation

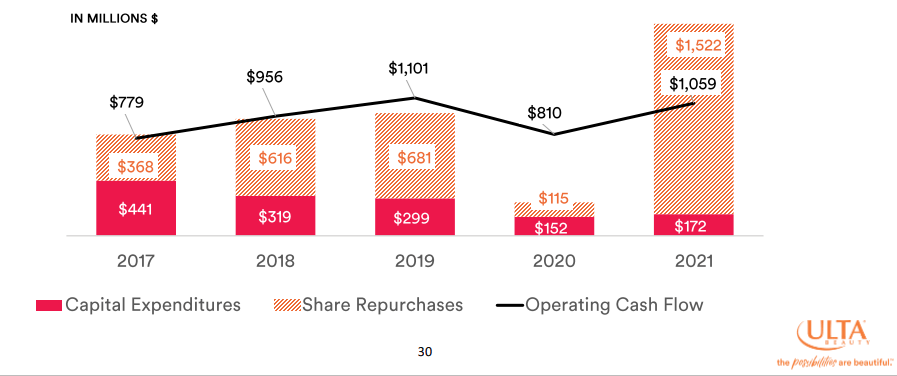

The company has reduced its share count by about 15% over the past decade. Based on some of the valuations Ulta has seen over time, I’d rather they initiated a dividend, but that doesn’t appear to be in the cards. Capex has consisted of mostly store remodeling, supply chain investments, and new store openings, and has gone down during the post-pandemic era. I wouldn’t be surprised to see it normalize back to a higher level over the medium term, but outside of international expansion, the era of significant new store adds is past for Ulta.

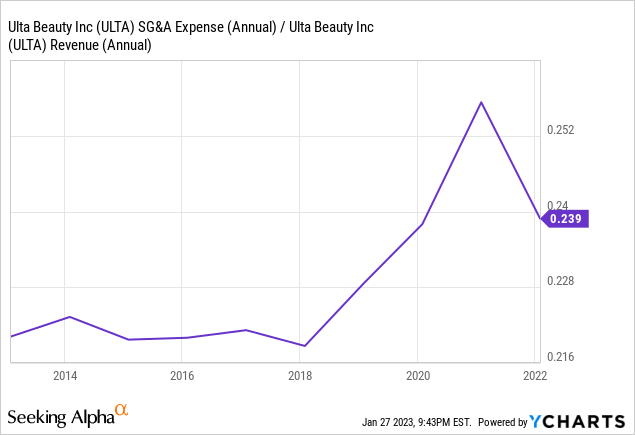

SG&A as a percentage of revenue spiked through the pandemic, and settled out during the most recent results. 24% isn’t a terrible spot to model SG&A going forward, as some of the expenses the company is dealing with are likely here to stay. Here’s some perspective from the call:

In SG&A, we got store payroll upward pressure on wages, which we expect to continue, maybe not to the same rate we’ve seen here this year, but certainly will continue upward. Variable cost, inflationary pressures, again, credit card fees, I mean, we’re seeing it in every part of our business right now. We’ve been able to mitigate a lot of that. And super high sales increases help camouflage that a bit as well. And then, of course, our strategic investments, as we mentioned in the script, we plan to ramp those up, and that’s coming in 2023, so other digital investments and UBN and target as well.

This is an important metric to look at as the company launches its new store format, and potentially international store rollouts in the future. If SG&A creeps up and outpaces revenue growth, it’s a solid sign of worse operating characteristics.

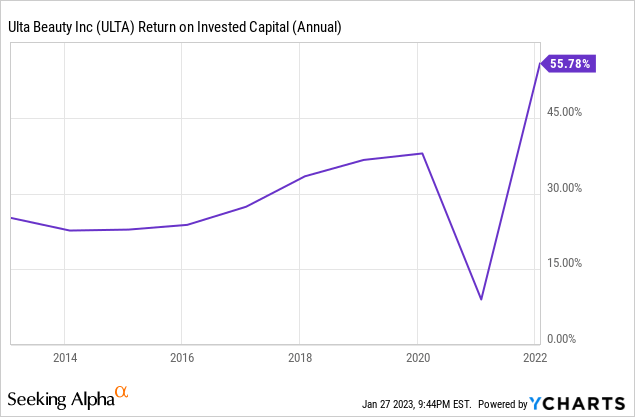

Looking at returns on invested capital, the dip was expected, and it most certainly returned to form. I’ve seen figures of 10% for the weighted average cost of capital, so Ulta definitely checks the box here for profitable growth and shareholder value creation.

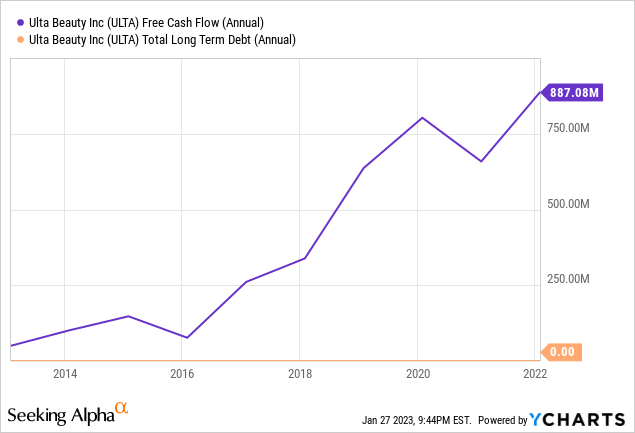

Looking at the balance sheet, it couldn’t be a lot better than this. The company carries no long-term debt, and has consistently driven higher free cash flow. Again, it’s a shame they don’t pay a dividend.

FAST Graphs

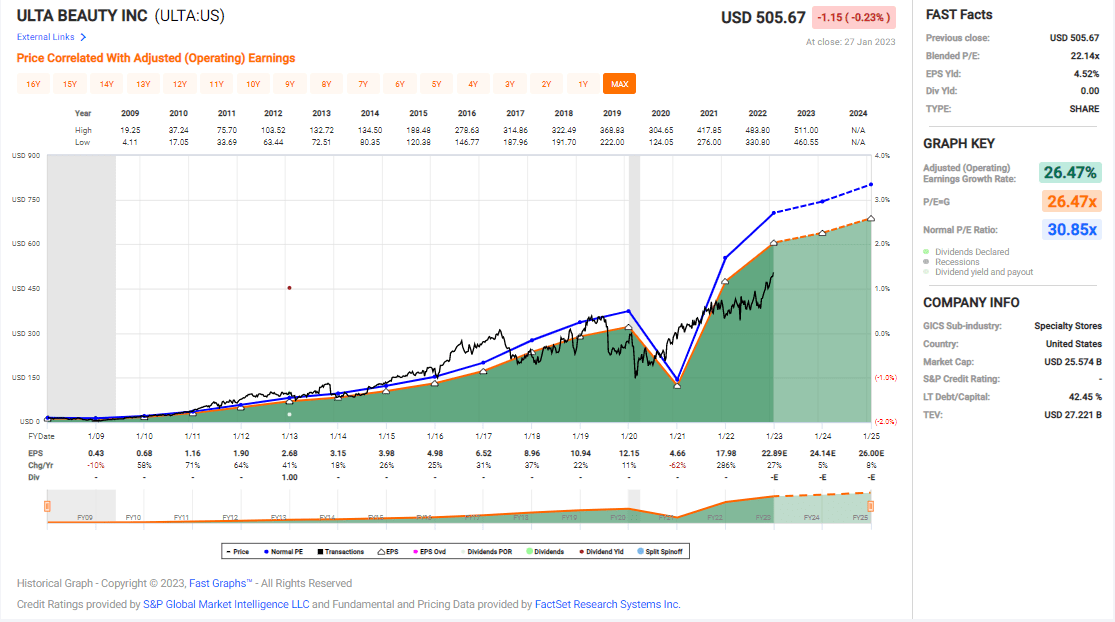

Ulta is trading near all-time highs currently. Looking at the bounce-back in earnings, that’s no surprise. Despite the elevated share price, it doesn’t appear to be nearly as rich as it could be at first blush.

FAST Graphs

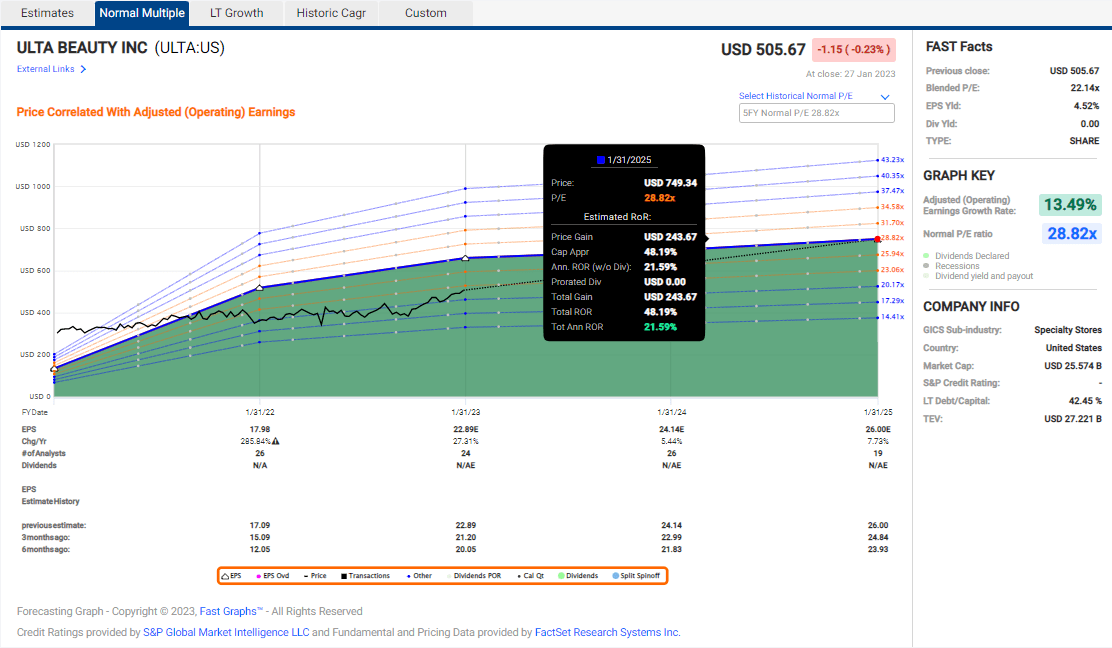

Based on analyst estimates for earnings growth, returns over the next few years could be as high as the low 20’s% annualized. A couple of disclaimers here. That assumes a 28X earnings multiple, which is historically what Ulta has garnered, but there’s no guarantees of that going forward. Additionally, nothing is guaranteed, and there’s a huge number of factors, including the overall economy, that could throw a wrench in this. I’d anticipate the company’s P/E ratio to come down somewhat. The easy store growth in the US market is likely behind the company. I remain skeptical of the Target store formats, and don’t see them driving the same returns as Ulta’s main stores. However, I won’t bet against Ulta’s ability to continue driving meaningful earnings growth, just maybe not quite as high as it has over the past decade. Currently, the company is firing on all cylinders, and full economic recession is the most likely thing in the way of that continuing.

With that, Ulta is a buy. It has a leading market share, strong returns on capital, has carved a moat in its industry, and carries a pristine balance sheet. Ulta is a best-in-class retailer.

Be the first to comment