Sundry Photography

Uber Technologies, Inc. (NYSE:UBER) has recovered from its June/July lows, as we urged investors to ignore the pessimism.

However, UBER has failed to make sustained gains since forming its September highs, which subsequently saw UBER pulling back nearly 35% to its October lows. It’s a stark reminder for new UBER investors to abstain from chasing momentum spikes, often “disguised” as opportunities for astute market operators to take profits/cut exposure.

Notwithstanding, we believe the market environment has continued to improve for Uber since its Q3 earnings card.

Management highlighted its confidence in its Q3 commentary that consumer spending remained robust. In addition, the recent earnings commentary from the leading US banks has continued to corroborate strong consumer spending, despite the prospects of a downturn later this year.

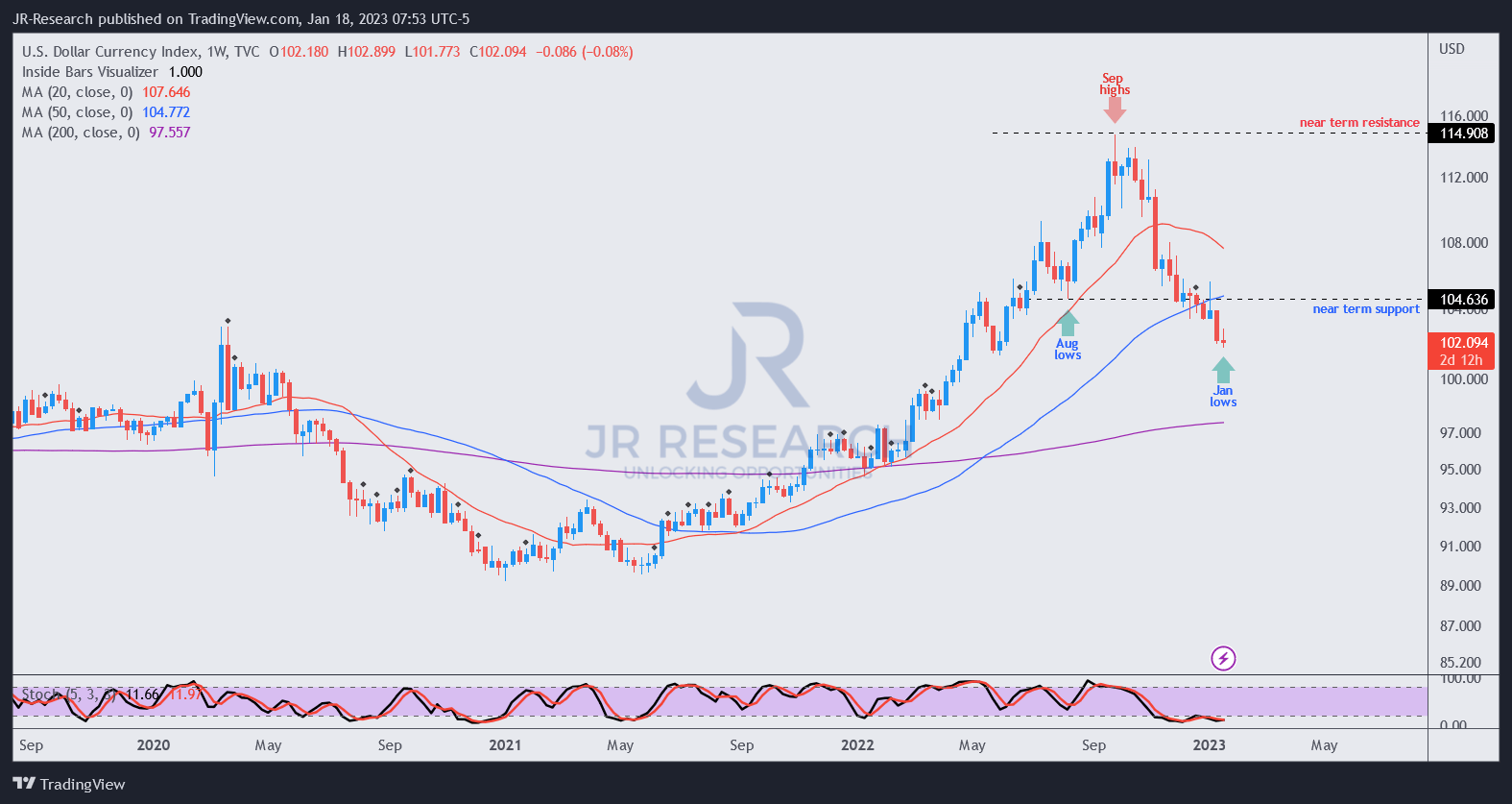

DXY price chart (weekly) (TradingView)

Moreover, the forex headwinds that hampered Uber significantly in 2022 have abated markedly. The Dollar Index (DXY) has declined more than 11% from its September highs, as market operators anticipate a less hawkish Fed in 2023.

Notably, DXY bulls failed to support its price action above its pivotal 50-week moving average or MA (blue line), suggesting that DXY’s medium-term bullish bias is likely over. Hence, we believe it forebodes well for Uber, given the impact on its Q4 outlook it promulgated previously. Accordingly, management indicated an “expected 7 percentage point YoY currency headwind” to its gross bookings guidance.

With the DXY dropping to lows last seen in June 2022, it should provide a welcome uplift for Uber’s Q4 and FY23 outlook.

Despite that, the company is still mired in a recent lawsuit with New York City’s Taxi and Limousine Commission (TLC). However, Uber prevented the TLC from instituting a price hike as it argued the commission’s methodology was “flawed.” However, the judge overseeing the case encouraged the TLC to return with an improved basis to justify its hikes appropriately. Hence, investors should continue to pay close attention to the developments.

Uber isn’t new to such regulatory challenges, with the most recent ones involving the classification of gig economy workers, as discussed in its Q3 earnings commentary.

As such, investors need to assess whether the regulatory landscape could favor Uber’s ability to continue scaling constructively toward its FY24 adjusted EBITDA target of $5B.

The impetus for the company to continue scaling up shouldn’t be understated. Accordingly, UBER last traded at an NTM EBITDA multiple of nearly 23x or an NTM P/E of 87x. Therefore, it should be clear that a significant level of forward operating leverage has been baked into its valuation.

Despite the ongoing regulatory challenges, we believe investor focus remains on the company’s ability to navigate a challenging macro landscape. We believe Uber’s leadership in the ride-hailing space should continue to help it gain market share in the delivery segment as it penetrates further with its Uber One membership program.

As a result, we believe the company’s confidence in its ability to continue expanding its 10M membership base is well-placed. Moreover, its smaller delivery competitors have been hampered by cost rationalization initiatives as funding campaigns dried up due to the hawkish Fed and market volatility.

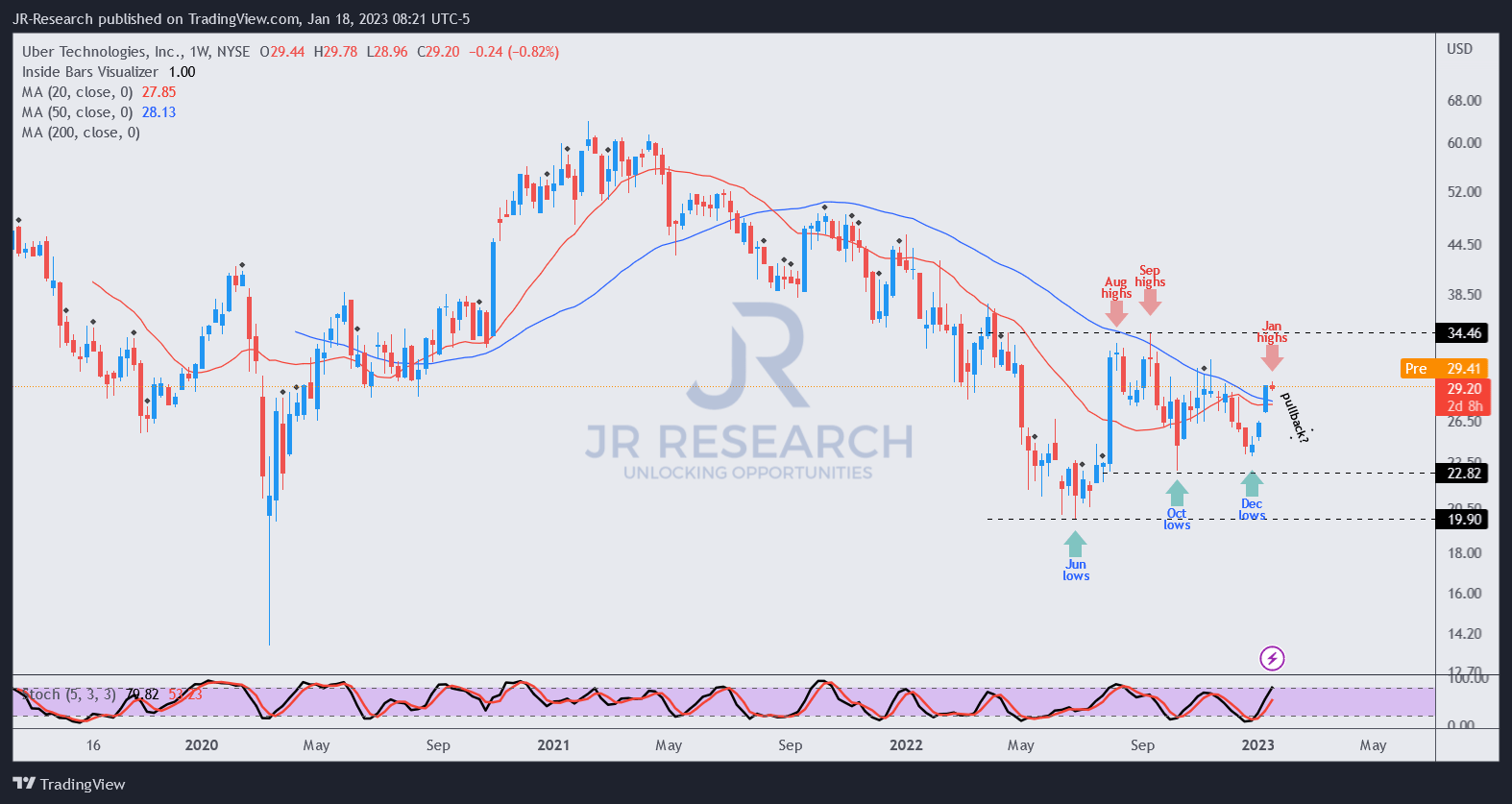

UBER price chart (weekly) (TradingView)

UBER remains mired in a medium-term downtrend, but green shoots of recovery have continued to form.

We believe its June lows will not likely be retaken, as critical headwinds (macro, forex, consumer spending) that impacted its operating performance are expected to weaken further. While regulatory challenges remain a tail risk, we are constructive over UBER’s price action.

Despite that, UBER has already recovered markedly from its December lows, resembling another momentum spike we cautioned about earlier.

Investors considering adding exposure should remain patient and wait for another pullback first.

Rating: Hold (Reiterated).

Be the first to comment