RichVintage

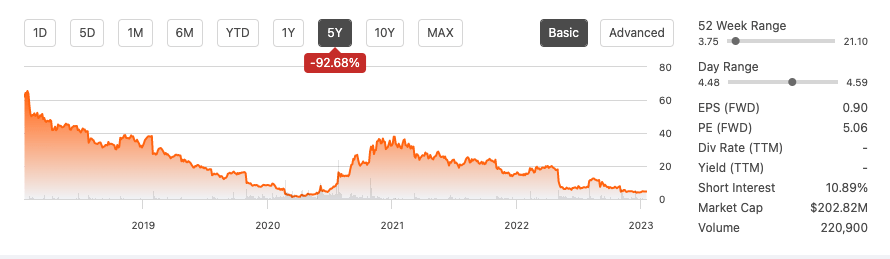

Tupperware Brands Corporation (NYSE:TUP) has seen its stock price plunge by 68.95% over the last year and by 92.68% over the previous five years. The top and bottom line results have been deteriorating annually. The previous quarter’s sales dropped 20% YoY. With high debt, negative cash from operations and performance concerns from management, there is a lot to be concerned about.

Five-year stock trend (SeekingAlpha.com)

In 2021 TUP set up a three-year turnaround plan to improve sales run by CEO Miguel Fernandez brought on in 2020 with a background in supply chain management. The goal is to increase distribution from a direct seller model to a multi-distribution channel. Partnering with Target (TGT) is part of this strategy. It is also broadening its range into environmentally conscious offerings. While TUP has cultural icon status, it has not won over the same admiration from Gen Zers and Millennials. As the company heads into bankruptcy waters and with few concrete growth channels in sight, I recommend something other than buying the stock.

Overview

TUP has been making plastic storage containers for seventy-six-year. Its mission was and is to help customers save money on food waste. Its fame exploded in the 1950s after it took on a direct selling approach through Tupperware parties aimed at women.

Tupperware party in The Marvelous Mrs. Maisel (businessinsider.in)

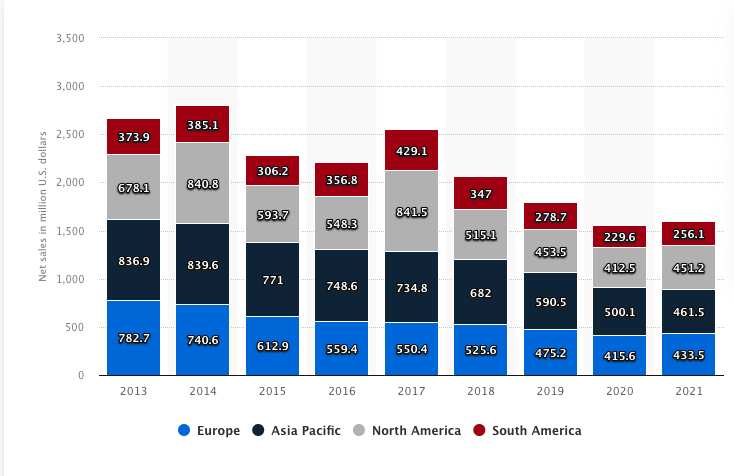

The products and distribution model has undergone a few changes, although it has been for sale on its website and other e-commerce channels. This year the company wants to push a broader distribution channel, partnering with TGT to increase sales. Its offerings are available in over 70 countries, and revenues are still over one billion. However, sales have declined across all four of the company’s geographic sectors since 2017 and produced negative cash flow from operations.

Net sales by geographic segments (statista.com)

TUP admits it has become dated and needs to increase its consumer scope with a focus on distribution and an environmentally conscious product range to reach out to Gen Z and Millennials who still need to grow up with TUP.

There are a few critical indicators that things are going south beyond repair. Firstly, the company publicly announced a turnaround plan in 2021, but we are a year further with no better revenue prospects. The management has revealed uncertainty about its ability to perform in its Q3 earnings call and concerningly withdrew its outlook for 2023. There have also been many managerial changes to the business recently, such as a new CFO this year, replacing the previous CFO after only three years in the position. It has also newly promoted Hector Lezama to CCO.

Financials and Valuation

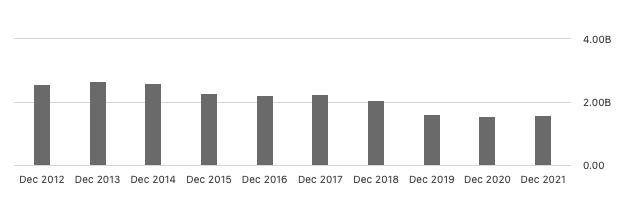

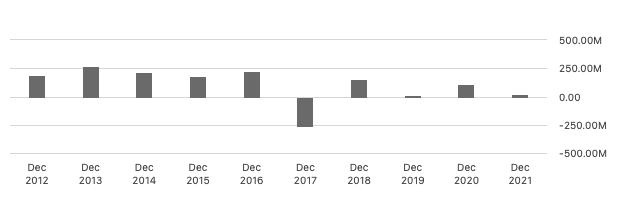

TUP is facing significant financial problems as sales decrease at double-digit rates. Annual revenues have been downward trending since 2013. In the most recent third-quarter results, quarterly revenue dropped by 20% YoY to reach $302.80 million. Yearly sales results have remained above the one billion mark. The gross margin is 63.50% TTM, slightly decreasing from 67.16% in 2017. Furthermore, if we look at net income, we see FY21 end at $18.6 million.

Annual revenue (SeekingAlpha.com) Annual net income (SeekingAlpha.com)

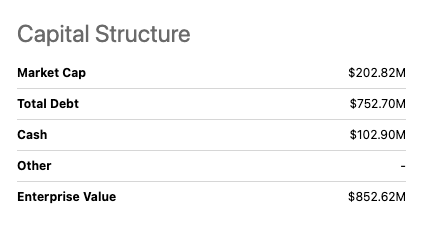

The company’s capital structure has a total debt of $752.70 million which is high relative to their cash of $102.90 million. Cash from operations has been damaging the last two quarters at negative $41.3 million for Q2 and negative $8.2 million. It has a current ratio of 1.29 and a low quick ratio of 0.53, which looks risky under the current downward-performing trends as it may not have enough quick assets in the short term to meet obligations. Its levered TTM cash flow is negative $1.15 million.

Capital structure (SeekingAlpha.com)

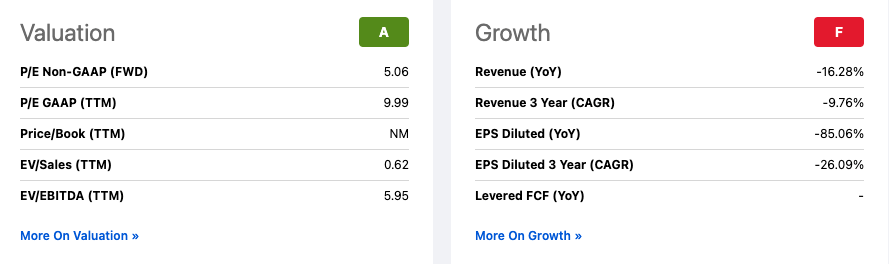

The stock has a high short interest of 10.89%, indicating that investors expect negative performance in the future. The stock has an attractive forward price-to-earnings ratio is 5.06; however, we can see that the company’s growth rate is decreasing in the double digits and has been on the decline for years. While TUP has a turnaround plan to increase sales, six months into the action plan and with TUP distributed at Target stores, we have yet to see positive results, which is very worrisome.

Quant Valuation and Growth (SeekingAlpha.com)

Final thoughts

TUP was a much-loved brand for many years. However, plastic has lost its charm. The industry has been flooded with cheaper competitors. Many alternative solutions are often described as healthier and more environmentally conscious. Furthermore, it wants to tap into a younger market with little affinity with the brand that grew through its original sales party methods in the 50s. Although the company has discussed a turnaround plan, we have not seen any results. On the contrary, management has given little confidence in the stock during their earning calls. For this reason, I recommend that investors stay away from this stock.

Be the first to comment