BING-JHEN HONG/iStock Editorial via Getty Images

2Q22 recap and outlook

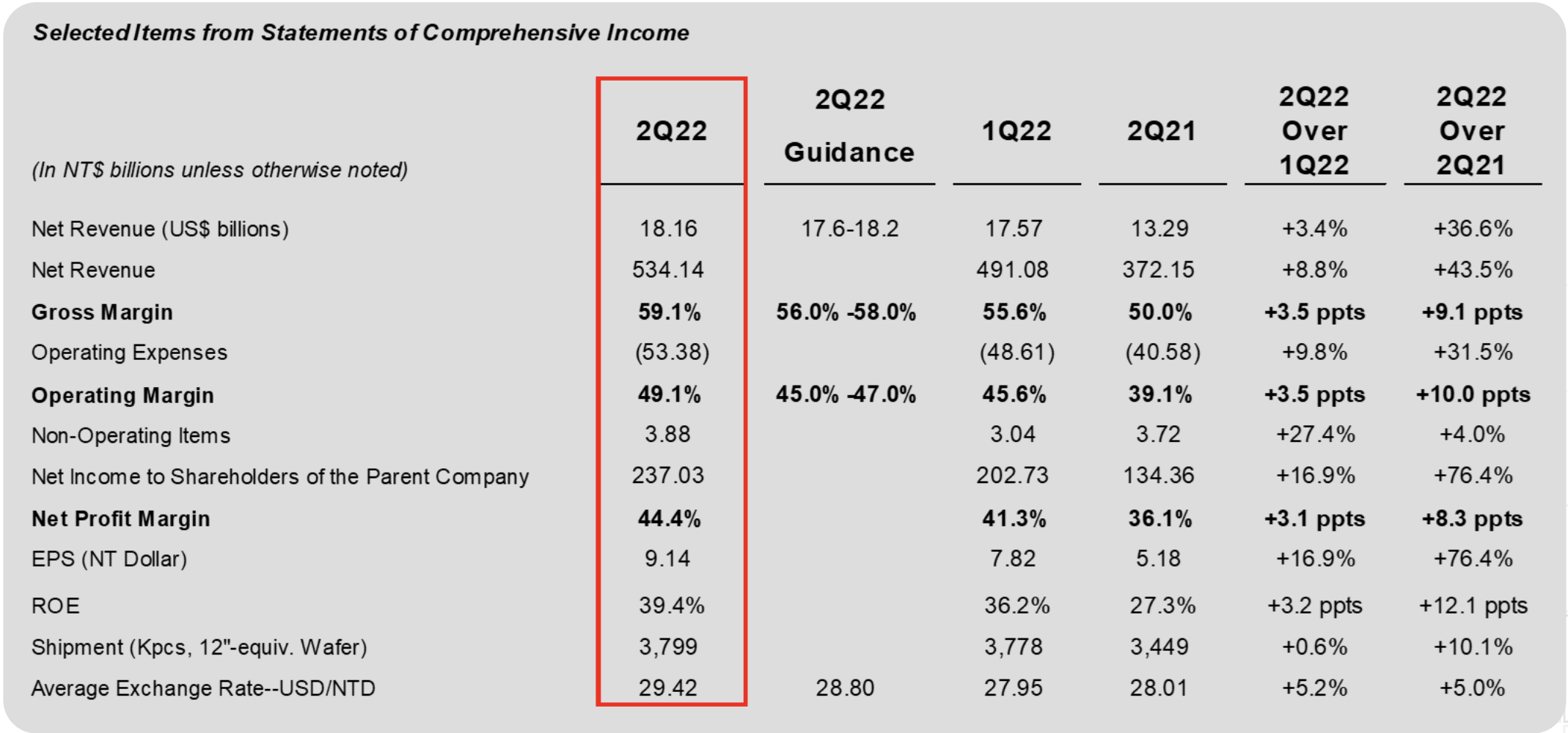

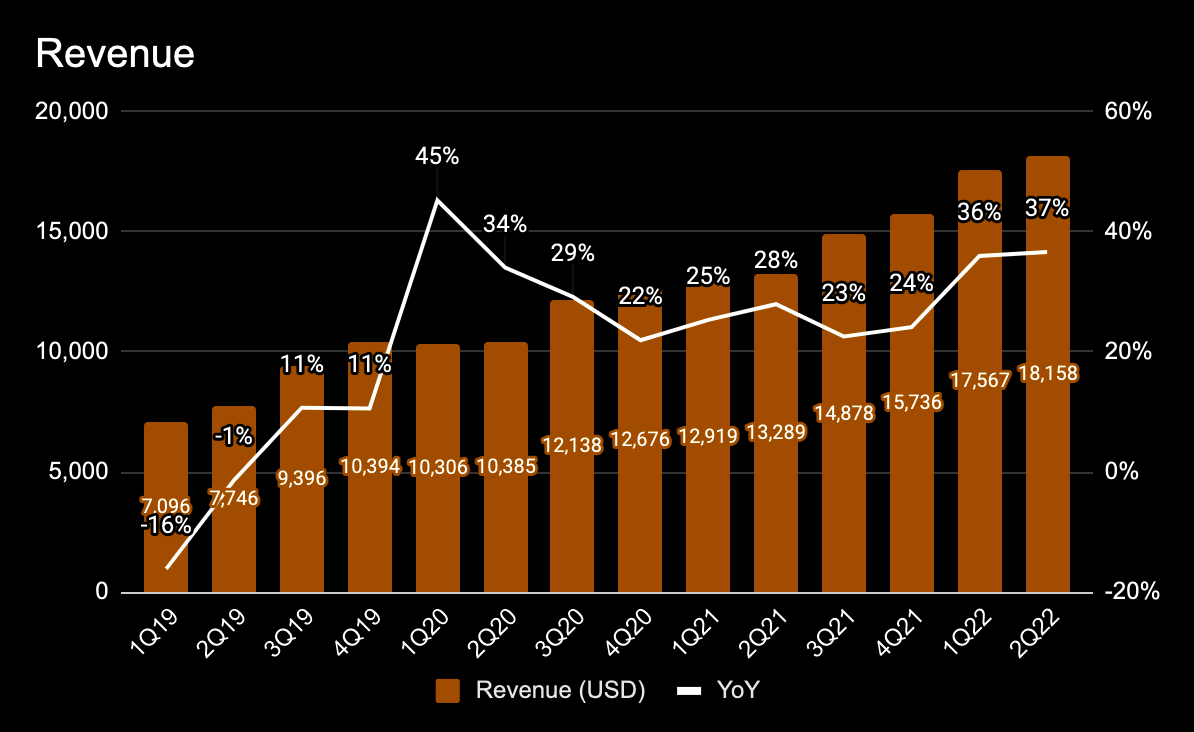

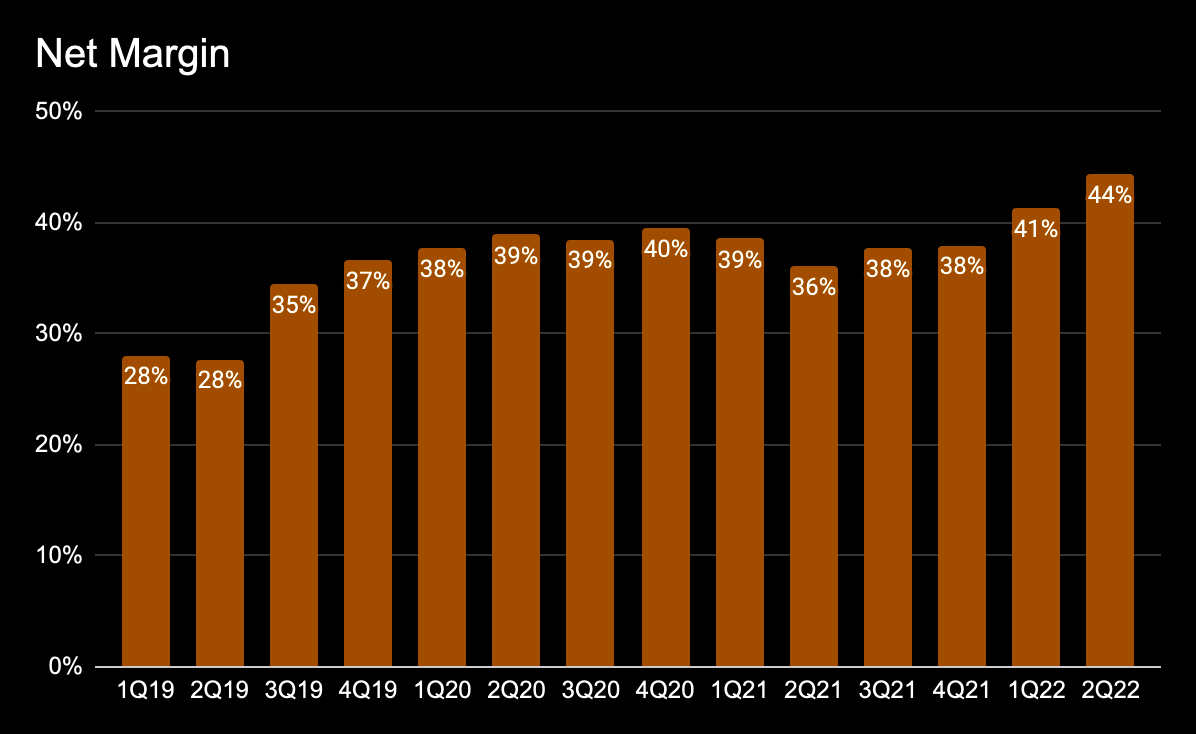

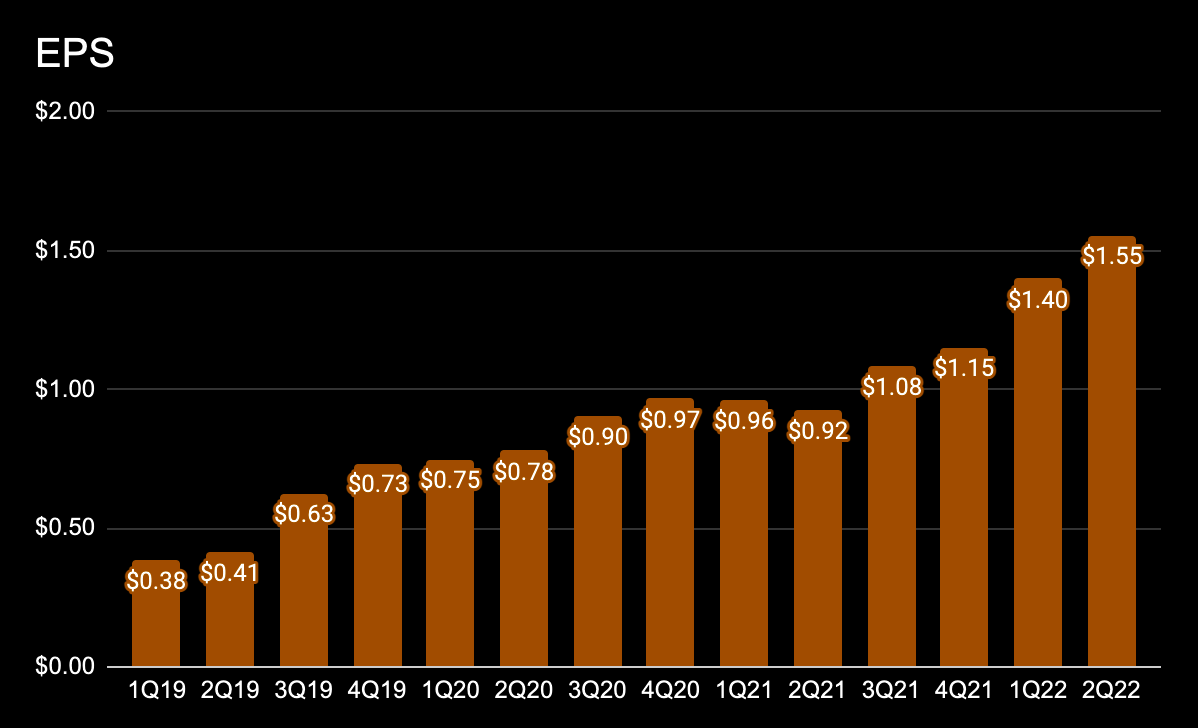

Taiwan Semiconductor (NYSE:TSM) delivered a stellar 2Q22 with revenue of $18.17 billion (+37% YoY) that beat estimates by $580 million and diluted ADR EPS of $1.55 against $1.5 consensus. Gross margin of 59% was above the previous guidance of 57%, driven by better pricing and favorable FX. Operating margin was also above 46% guided previously. Net margin saw a sequential 3 point expansion from 41% in 1Q22 to 44% in 2Q22. Looking at the numbers, management continues to execute with excellence (see below charts).

Company data

Company data

Company data

Company data

Company data

Company

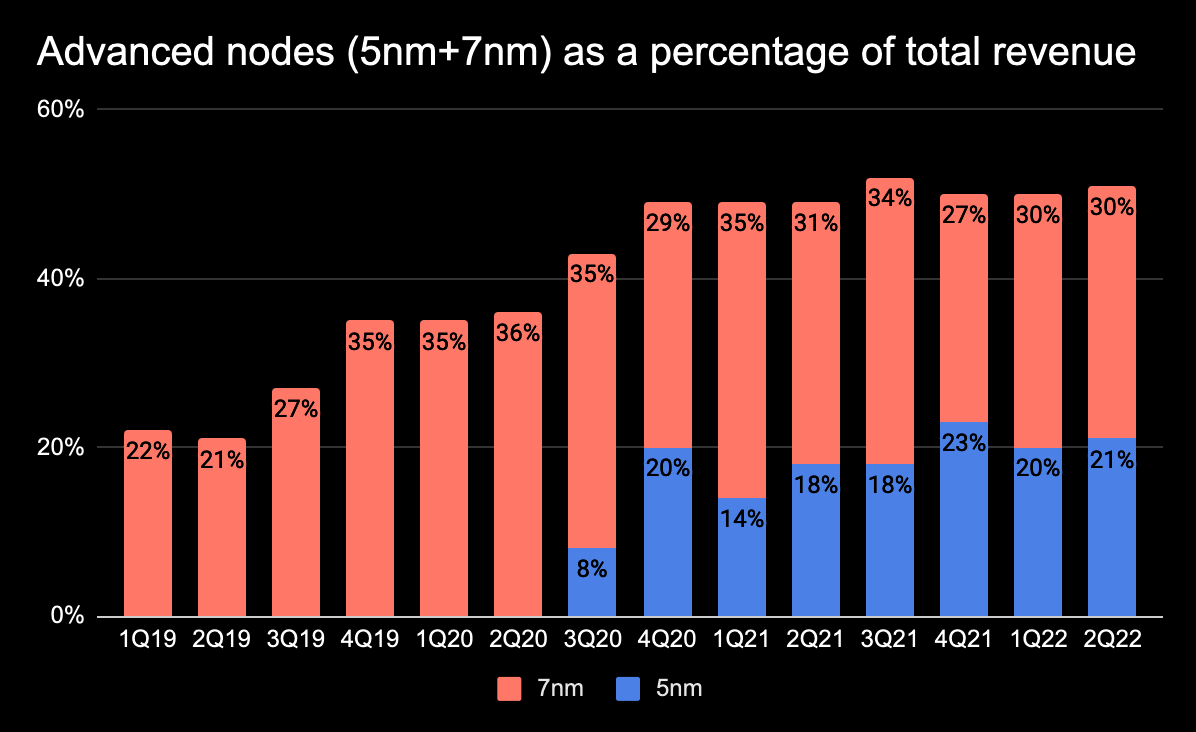

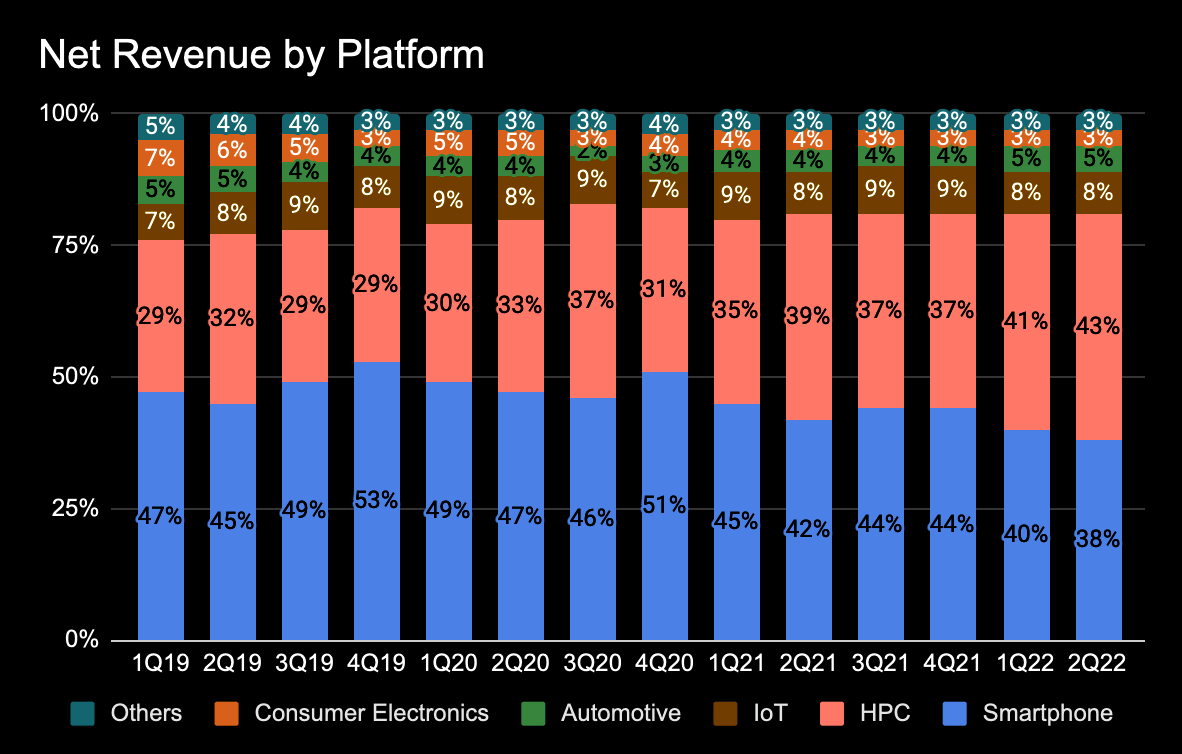

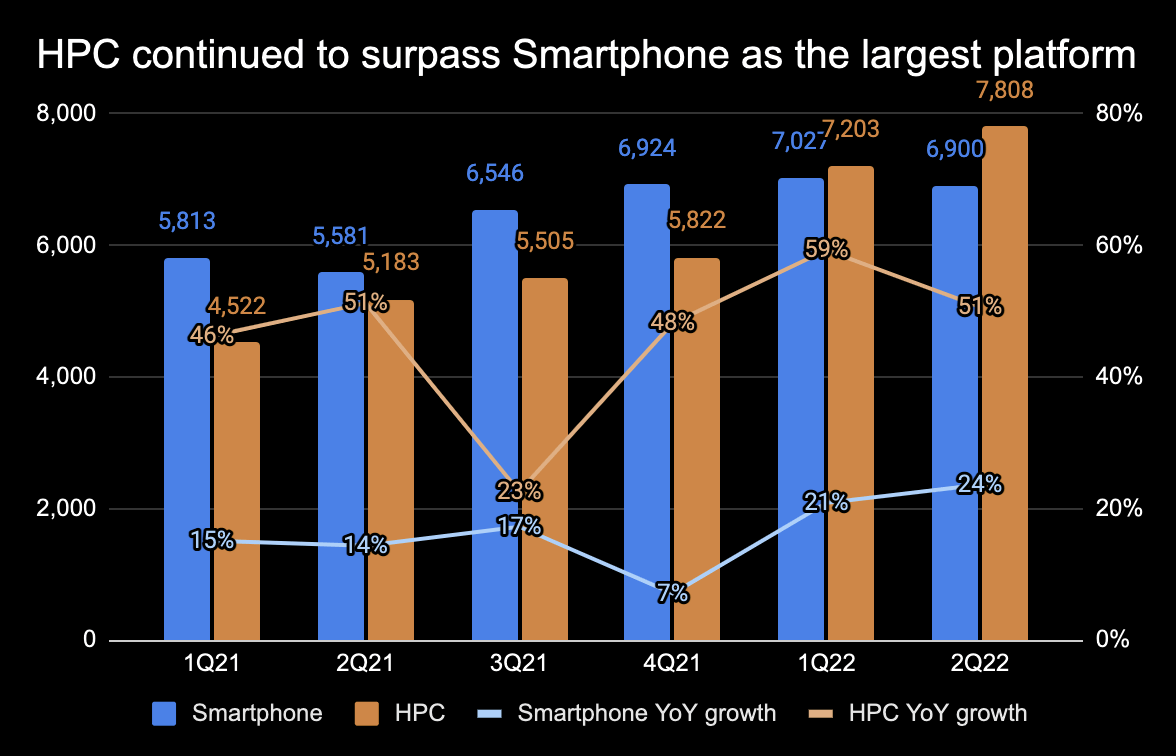

As a leader in advanced technology, TSMC’s leading-edge nodes (N5+N7) made up 51% of total wafer revenue in 2Q22. N5 capacity remains tight, with strong demand from Apple (AAPL) (iPhone 13/14, M2), QUALCOMM (QCOM), NVIDIA (NVDA), and Amazon (AMZN) (Graviton 3). In Q2, HPC continued to surpass Smartphone as the largest platform with $7.8 billion of revenue, up 51% YoY vs. +59% YoY in 1Q22. As a percentage of total revenue, HPC was 43% vs. Smartphone’s 38% in the quarter. The driving force behind HPC continues to be rising computing demand and in-house silicon designs amongst major players including Amazon, Microsoft (MSFT), Meta (META), Alphabet (GOOG) (GOOGL) and Chinese hyperscalers such as Alibaba (BABA) and Tencent (OTCPK:TCEHY).

Company data

Company data

Company data

J.P. Morgan

For 3Q22, TSMC provided the following guidance:

- Revenue of $19.8-$20.6 billion (+36% YoY) vs. $18.5 billion consensus.

- Gross margin of 57.5%-59.5% vs. 56% consensus. The slight QoQ decline was due to higher input costs (raw materials and electricity) but still above management’s long-term target of 53%+.

- Operating margin of 47%-49%. vs. 46% consensus.

For full year 2022, management increased its revenue outlook from mid to high 20% growth to +35%, and also reiterated its long-term revenue CAGR of 15%-20% over the next several years.

Inventory correction

It’s no surprise the demand for PC, smartphones and other consumer electronics such as TVs are slowing. TSMC management noted that customers are already reducing inventory levels in 2H22 following exceptional demand during the pandemic. Chinese smartphone leaders (Xiaomi, Vivo and Oppo) have collectively cut orders by 20%, causing Qualcomm and MediaTek to reduce 5G chip orders by another 30% in the second half of the year. AMD (AMD) is pulling back on products made using N7/N6, while Nvidia is looking to cut chip orders for RTX 40 series given the market is now flooded with GPUs thanks to the collapse of crypto prices. This trend applies to a number of other things like TV display drivers, 5G RF transceivers, power ICs, and SSD controllers.

TSMC management noted that inventory adjustments will take a few quarters and will likely last through 1H23. While there’s clear softness in consumer end markets, demand for data center and automotive is expected to remain strong and TSMC is able to allocate more capacity to support these higher growth segments as production remains tight throughout 2022.

Despite the negatives of inventory corrections throughout the industry, a number of positive developments for TSMC include:

- Qualcomm will be exclusively contracting TSMC for its flagship 5G chips (Snapdragon 8 Gen 2) in 2023/24 (Ming-Chi Kuo).

- Nvidia is shifting gaming orders from Samsung N8 to TSMC N4/5 in 1H23.

- Apple iPad will be using TSMC N3 in 1H23.

- AMD is releasing new Ryzen CPUs and Epyc server chips in 1H23.

N3 & N2 status

TSMC’s most advanced N3 node is on track to enter mass production in 2H22 with revenue contribution expected in 1H23. Apple will be the first customer, and Intel (INTC) is expected to join in later. In the past, new technology like N7/N5 represented 9%/8% of total sales in their first year of production in 2018 and 2020 respectively. As a result, 2023 will likely see minimal contribution from N3 and muted margins as higher depreciation expenses kick in.

Though Samsung Foundry (OTCPK:SSNLF) beat TSMC to N3 mass production using the Gate-All-Around (GAA) transistor architecture, process yield remains a major question. If Samsung struggles like it did with N4 and N5, TSMC will virtually have a monopoly in N3.

N2 development is on schedule, with risk production expected in 2024 and volume production in the second half or end of 2025. Made with the GAA transistor architecture (Nanosheet), N2 will provide 20%-30% power improvement and >20% higher density vs. N3E. TSMC expects to maintain its technology leadership upon N2 launch.

Conclusion

TSMC remains the most competitive foundry with undisputed process leadership, solid execution, and enviable margins despite massive capital expenditures. The broader-semiconductor sector has experienced a brutal selloff as investors digest the prospects of slowing end market demand and a potential recession that typically doesn’t bode well for chip stocks. However, TSMC is one of the most resilient names in the business, and robust HPC and automotive demand should offset some of the inventory concerns in consumer markets in the short term. All told, I believe TSMC remains a buy for any long-term investors.

Be the first to comment