Drepicter

My newsletter subscribers had early access to this article.

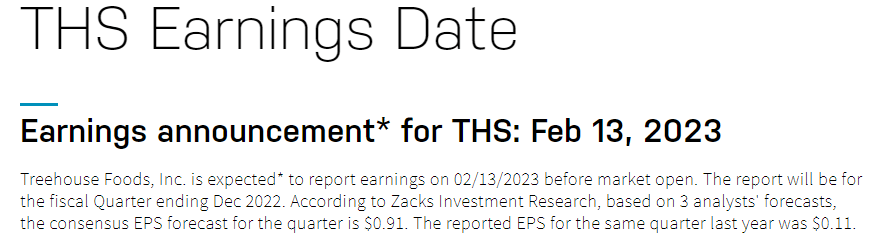

Today we look at a long position on TreeHouse Foods (NYSE:THS) over the company’s Q4 earnings:

Nasdaq

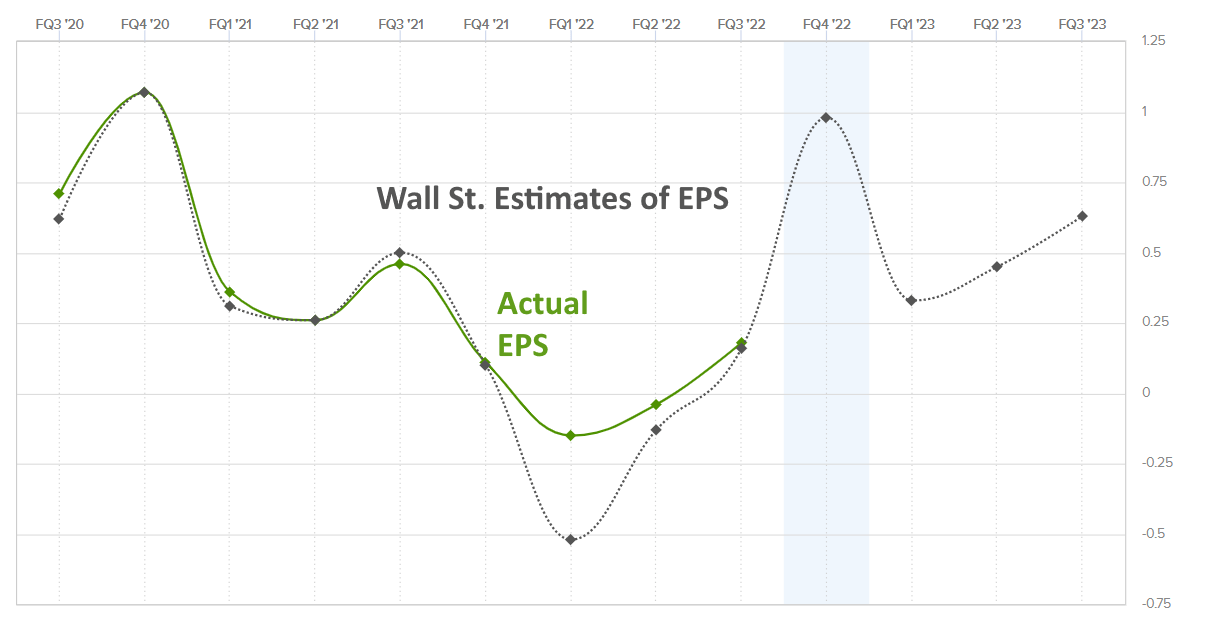

In buying a stock before earnings, we look for factors that hint at a discrepancy between market expectations and reality. On the long side, lesser known (non-glamour) stocks tend to rally more often and more strongly on earnings than big-boy, glamour stocks. Moreover, we can see how analyst expectations work against reality by plotting the consensus estimates against the actual reported EPS, and we might find that – such as in the case of THS – when analysts are wrong, they are more often underestimating than overestimating, allowing for more rallies than selloffs on the actual report:

Estimize

Notice how EPS is set to go from nearly zero to $1. That’s a large jump in profitability and represents an important quarter. A beat, which isn’t all that uncommon for this stock, could lead to a rally, as could improved guidance.

Still, a miss can lead to a selloff, which is why we want to hedge risk via either using options or selecting a stock that is attached to a financially healthy company. A company that is not distressed typically sees smaller selloffs in the event of a bad earnings report. THS is of this type, as it has sufficient cash runway to last through the next three years before debt becomes an issue.

In addition, my backtests on THS shows that the “investor profile,” or the behavioral patterns of investors relative to this stock over novel information dissemination (e.g., earnings reports or news reports) is generally bullish for THS over its earnings report period. For one, THS investors tend to buy more stock on good news events, which sounds like common sense but is actually not as common as you’d think in the investing world. Actually, looking at THS’s action over news events, segmenting the news by “negative,” “neutral,” and “positive,” we find that THS acts as expected, with investors buying more than expected on positive news; investors holding on neutral news; and investors selling off on bad news. Of course, ideally we want our targeted stock to underreact on negative news (e.g., investors holding instead of selling), but we cannot always have that, which is why we use options to hedge the downside risk.

In any case, the timing for this play is quite good, even though we are a couple weeks out from earnings. THS is set to undergo 12% upward mean reversion relative to the market. And we have a down gap, which is most likely an area gap and should fill within a couple weeks, statistically, thereby bolstering the long side of this play from a technical level:

E-Trade Pro

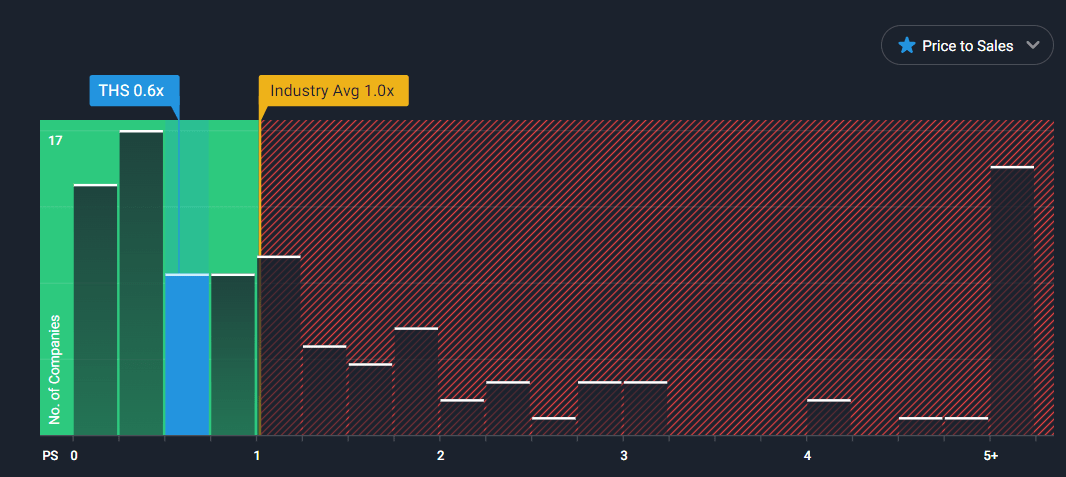

We also wish to know whether a fundamental look at this stock is in line with our bullish thesis, which was primarily built upon seasonal patterns, statistics, and technicals. Essentially, we choose our stock so that these parameters meet our standards, and then we check whether the fundamental and macro picture also makes sense. From a valuation perspective, THS has much room to run before it becomes priced around the industry average. For instance, THS falls below the average in both price-to-sales and price-to-book:

Simply Wall St.

Simply Wall St.

From a discounted cash flow, too, THS is undervalued, and the mean-reversion target of a 12% increase, leading to a trading price of over $53 seems reasonable.

A movement up is also more likely than a selloff. Over its Q4 earnings reports, THS has moved up 76% of the time. The average upward movement is about $4, again justifying our $53 short-term price target.

So, from a probabilistic perspective, we have a very good target for an earnings trade on the long side. Again, the fundamentals justify a likely movement upward. According to its last earnings call, the company’s management has been focusing on increasing revenue and earnings by more aggressive pricing, and thus growth should continue despite the current economic downturn and inflation issues. Management expects this quarter’s volume to be flat due to supply chain issues, but other companies have been seeing improvement in this category, meaning the flat volume estimate might be overly conservative, leading to an EPS beat.

Moreover, THS expects a new form of income (transition services), which will be first reported in the upcoming earnings report. According to management, “The income will offset the related expenses for things like IT, HR and customer service, giving the domestic business time to establish its infrastructure.” This should lead to a nearly 20% increase in EBITDA margin.

Overall, we have a non-glamour stock suited for an earnings trade and supported by statistical, seasonal, and fundamental factors. Here’s how to play it:

Selling puts will give you extra income via time decay and volatility crush but does not hedge risk; you are just as at-risk as an investors holding long stock:

Sell Mar17 $45 puts.

If you want to hedge risk but don’t mind the volatility crush and time decay working against you (i.e., you’ll probably lose money even if THS barely moves on earnings due to these factors), just buy calls. We can alleviate the time decay by using further-out expiration dates:

Buy Aug18 $50 calls.

Close after earnings. Let me know if you have any questions.

Be the first to comment