CRobertson/iStock Editorial via Getty Images

Introduction

There are companies that can weather the storm. Literally. In fact, Tractor Supply (NASDAQ:TSCO) was among the December storm winners, as customers flocked to buy the necessary items to secure livestock and animals as well as vehicles. Helping customers enhance storm preparedness for their farms made the company see an extra 2 percentage points for comparable store sales in the quarter.

In this article, I would like to go over Tractor Supply’s Q4 and fiscal year 2022 report.

I already pointed out how Tractor Supply is one of my favorite retailers because I like the way it is focusing on growing comparable sales by rethinking their stores and earning more revenue per sq ft. As the company writes in its report:

In just over two years since introducing our Life Out Here strategy, we have executed Project Fusion in nearly 30% of our store base, built more than 300 garden centers, expanded our digital and supply chain capabilities and grown our Neighbor’s Club membership 47% to more than 28 million members.

Moreover, the company address a customer niche made up of home, land, pet and livestock owners who usually have above average income and below average cost of living. Keep in mind, most of its customers are hobby farmers and people who enjoy a rural lifestyle. Therefore, this company should not be looked at through the lens of corn and wheat futures or other metrics we use for agriculture-related stocks.

Understanding TSCO’s report

Let’s start from an easy to understand infographic:

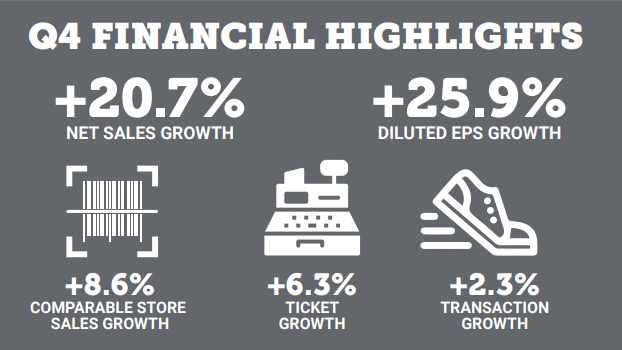

TSCO Q4 Infographic

Here are the metrics everyone looks at to assess retailers. Net sales grew by 20.7% and, even more importantly, comparable store sales grew by 8.6%. It is also important to understand how this growth was fueled. When the company says the average ticket grew by 6.3%, we can understand one thing: comp store sales was not only linked to pricing (and inflation). In fact, the company shows its transactions grew during the quarter by 2.3%.

If we zoom out and look at the whole year, we see the following results:

TSCO FY22 Infographic

To understand well the numbers, we should be aware that the fiscal year included an extra sales week which represented 1.8 percentage points of the 11.6% sales growth. Still, the company grew considerably.

If we think about it, the company actually accelerated during Q4 compared to the previous quarters (+11.6% for the whole year; +20.7% for Q4), showing strong momentum during winter. With sales topping $4 billion, this was the best quarter for the company ever. Now, don’t make the mistake of thinking that Q4 is usually Tractor Supply’s best one. It actually isn’t. To state the truth, sales are usually quite similar quarter after quarter, with the best quarters usually being Q2s. This is why this result is particularly impressive and bodes well for 2023.

To understand the size of the company, we have to know that net sales amounted to $14.20 billion. Overall, during the year gross margin decreased 17 basis points to 35.0% from 35.2%. Once again, this is excellent performance and we look at it through the last quarterly results, we have reasons to believe the company has overcome a tough environment for margins with success. In fact, as a percent of net sales, SG&A expenses were flat at 24.9% compared to fiscal 2021.

TSCO Q4 Results Presentation

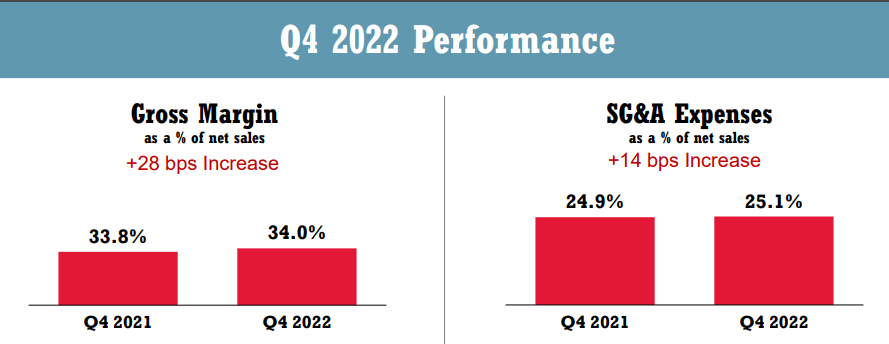

Now, revenue growth is not enough to make a company valuable. It is not hard to find companies whose revenue is growing while they are actually losing money. This year, we saw many good companies grow their revenues, while seeing margin compression due to higher costs. Well, Tractor Supply proves once again it is well managed. Let’s look once again at its margins. During Q4 gross profit increased 21.7% YoY to $1.36 billion from $1.12 billion. Most importantly, gross margin increased 28 bpts YoY to 34.0% from 33.8%. This is a very solid performance as it shows that after a whole year of high inflation, the company became nonetheless more profitable. Of course, it increased prices, but to a point its customers found reasonable.

Let’s talk about another important topic: shareholder returns. The current dividend yield is 1.72%, however it grew at a CAGR of 28.5% over the last 5 years. This is why I think the company is very interesting for the long term.

Overall, Tractor Supply returned $1.11 billion of capital in 2022, repurchasing 3.4 million shares for $700 million and paying $409 million in quarterly dividends through the year. Next year, the outlook is for a lower amount to be spent on share buybacks in the range between $575 to $675 million. I think it is thus reasonable to expect the amount spent on dividends to increase to around $500 million, which should lead to a dividend growth of approximately 20% or more, depending on the timing of the buyback and the number of outstanding shares.

The company keeps expanding, with 63 new Tractor Supply stores opened during last year, together with 9 new Petsense by Tractor Supply stores. Let’s also consider the acquisition of Orscheln Farm and Home, which made Tractor Supply acquire 81 stores that will be rebranded to Tractor Supply by the end of 2023.

In 2023, the company plans to open around 70 new stores and 10 to 15 new Petsense by Tractor Supply stores.

If we consider that every store generates more or less $6.7 million in revenue with an operating margin at 35% that leads to a gross profit of $2.4 million we are talking about an expansion plan that should generate in a short time an extra revenue close to $500 million, for an extra gross profit of $175 million. Although this translates into a 3.5% growth, investors should acknowledge Tractor Supply’s consistency, which has been able to make the company a very safe investment even during recessions.

This is why I already explained why I believe the company deserves to trade at a premium compared to other retailers.

Valuation

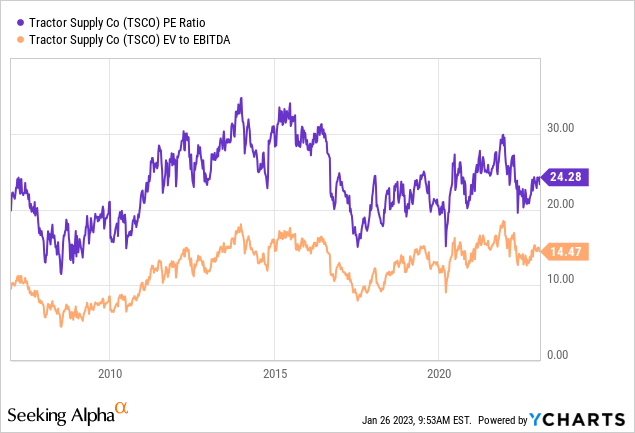

If we look at the company’s P/E and EV/EBITDA ratios, we see it trading in the higher part of its historical range.

In my past articles, I wrote I was willing to pay a 15% premium – compared to the general market – for the quality of this company. However, this led me to considering a 20 P/E multiple fair for this company. At the time of writing, the company is trading at $225 per share which gives a current P/E of 23 and a fwd P/E of 21.5. For me, this is a bit expensive and, even though I like the company, I don’t think it is the right moment to add. Actually, I believe some investors may actually lock in some gains at the moment, taking profit from the strong bump the stock saw after its earnings report.

Otherwise, I think those who are in for the long term should just hold, waiting for future pullbacks to increase their stake. In the meantime, it is very pleasant to own shares of a well-managed company able to compound well and to return excess cash to is shareholders.

Be the first to comment