jhorrocks/E+ via Getty Images

The third estimate of third-quarter real GDP was released yesterday, and the year-over-year rate of economic growth in the United States came in at 1.9 percent.

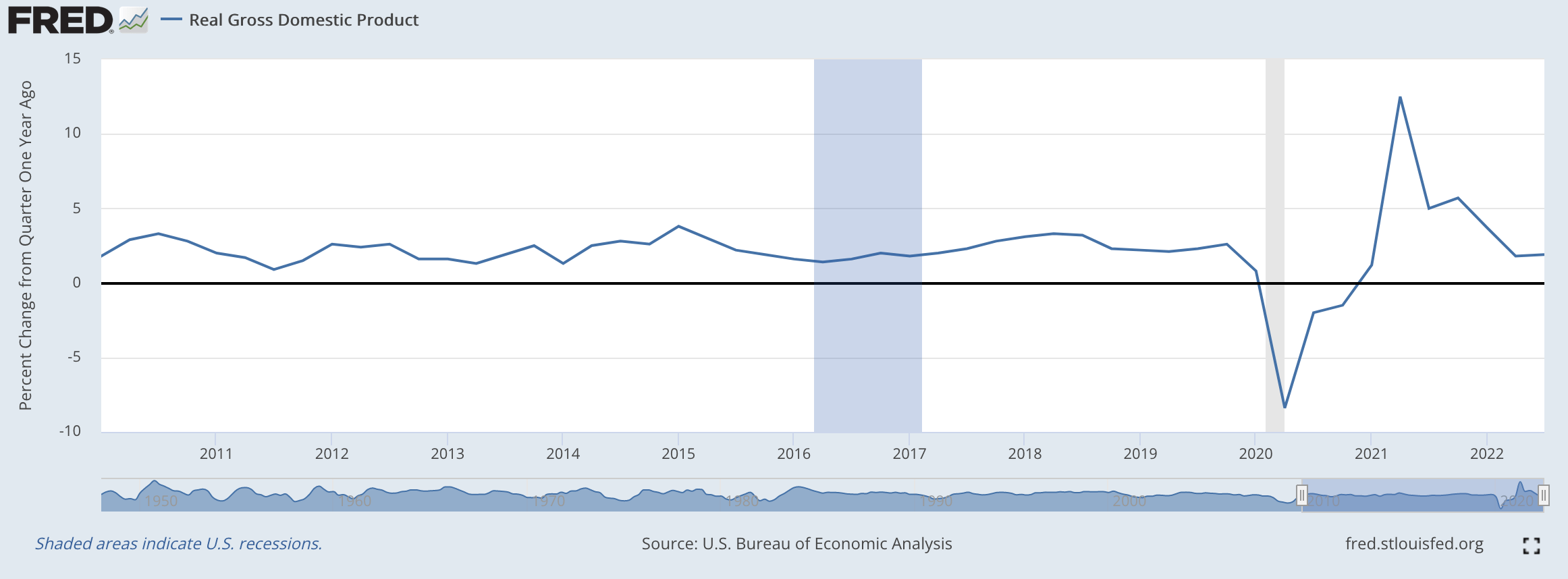

Note that we are still in a “crazy” period for the economic data since the numbers are still being impacted by the major disequilibrium state of the U.S. economy.

This can be seen in the following chart.

Real Gross Domestic Product: Year-over-year growth (Federal Reserve)

The year-over-year growth rate for the year 2021 was 5.7 percent.

So, it looks as if the economy is beginning to “steady out” but there is no real guarantee that this is the actual fact.

The last two years are obviously a substantial change from the decade following 2010, as the growth rate for this period of time worked out to about an annual compound rate of growth of approximately 2.3 percent.

For the past three years, the rate of growth of real Gross Domestic Product for the United States was 2.6 percent, fourth quarter-over-fourth quarter, in 2019, -1.5 percent, fourth quarter-over-fourth quarter, in 2020, and 5.7 percent in 2021.

What will the year 2022 look like from the perspective of the fourth quarter of 2021 to the fourth quarter of 2022?

Federal Reserve Projections

We have an estimate from the Federal Reserve’s Federal Open Market Committee year-end projections.

The Fed’s numbers indicate that the U.S. economy will grow, fourth quarter-over-fourth quarter in 2022, by only 0.5 percent.

Why the small growth rate for 2022?

Well, the growth rate of real GDP was near its peak levels in 2021, heavily distorted by real GDP numbers coming out during the Covid-19 pandemic.

It is understandable that the real rate of growth might drop off significantly.

But, the Fed’s estimate of a 0.5 percent year-over-year rate of growth indicates that the U.S. economy will not grow by much in the fourth quarter of 2022. But, note that the fourth quarter of 2021 was at the previous peak high for the size of the economy.

So, one of the reasons for the slow 2022 growth rate of 0.5 percent year-over-year is that the size of the economy in the fourth quarter was as large as it was.

So, this 2022 projection reflects, as much as anything, the distorted recovery taking place in the economy.

But, what about the Federal Reserve’s estimate for the growth rate of real GDP in 2023?

The Federal Reserve has suggested that the U.S. economy will only grow by 0.5 percent, fourth quarter-over-fourth quarter, in 2023.

The Federal Reserve is not saying that there will be a recession in 2023, but it is saying that its efforts to bring inflation under control will limit the amount of growth that can be expected for the year 2023.

Note that PCE inflation, the Fed’s target inflation rate, will drop, according to these projections, to 3.1 percent in 2023. This will be a drop from 5.6 percent to the expected rate of increase for this measure of price inflation in 2022.

So, the Fed expects that there will be a substantial improvement in the inflation picture in 2023.

Longer Term

Over the longer term, the Federal Reserve seems to be picturing an economy that is not much different from the one that preceded the disruptions caused by the Covid-19 pandemic.

The Fed’s expected rate of real GDP growth moves up to just under 2.0 percent for 2024, 2025, and the longer run.

Inflation, according to the Fed, will drop to 2.5 percent in 2024 and will reach 2.0 percent in the longer run.

The Fed is expecting to hit the target level it has been shooting for in the recent past.

No moving to a “new” 3.0 percent target here.

Wow! Everything looks rosy here.

The Fed, within the next three-to-four years, will achieve all its major goals with respect to the economy.

What a performance!

The Reality

It would be very nice if we could move the economy back into the Fed’s goal-orientated future and achieve it is the calm, steady way that is pictured in the Fed’s release.

However, I am not entirely sure that this will be the path.

There are many, many questions about 2023.

One of the questions pertains to the Federal Reserve, itself.

The Federal Reserve is now fighting inflation using a quantitative tightening model. That is, the Fed is reducing the amount of securities it has on its balance sheet in a (relatively) steady manner.

Although almost all of the attention directed toward the Fed’s policy efforts has been with respect to what it will do with its policy rate of interest, the real, longer-term impact on the economy will come from the actual amount of reduction that the Fed achieves in the securities portfolio.

The Federal Reserve got us into the position we are by the use of quantitative easing, its effort to “increase” the amount of securities in its securities portfolio on a regular basis. It overdid it!

Now, the question is about how the Fed will manage its quantitative tightening over time.

There is no evidence that the Fed can do an adequate job using this approach to achieve the monetary tightening it needs and nothing more or nothing less.

Furthermore, there is so much debt outstanding as a result of the Fed’s liberal injection of liquidity into the economy that it is understandable that in some areas we are now finding major collapses occurring.

The bankruptcies and failures in the world of cryptocurrencies are one such example. The problems in the SPAC area are another. And, there are several other areas that could be mentioned.

Furthermore, the U.S. economy is still in disequilibrium. Narratives of the state of the world just don’t go together as they once did.

The economy is still adjusting, and some of the adjustments that are taking place are of a major nature.

And, then there is the state of the world.

Enough said.

What can we expect from this picture?

Well, it seems as if the best picture we can draw of future economic growth looks like what occurred in the United States before 2020.

Mediocre growth…at best.

If the Fed is correct, U.S. economic growth will be even lower in the 2020s than it was in the 2010s.

And, it seems that all the dangers are related to the downside, with very little optimism anywhere.

Be the first to comment