ra2studio/iStock via Getty Images

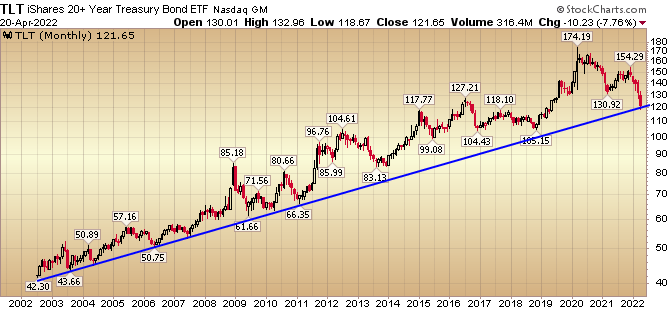

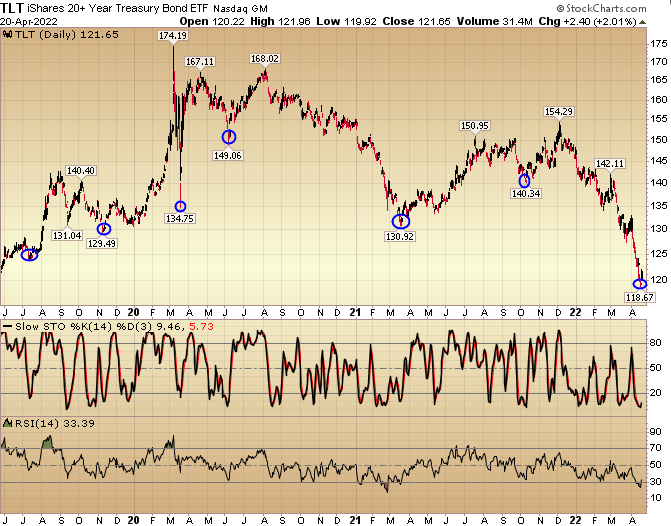

If you are wondering when Value Tech, Biotech and China Tech are going to finish their bear markets and roar higher, you need only look at one chart (which we referenced in the last couple of weeks). Here it is (originally) and denoted with multiple other takes:

stockcharts.com stockcharts.com

Bryan Rich

stockcharts.com

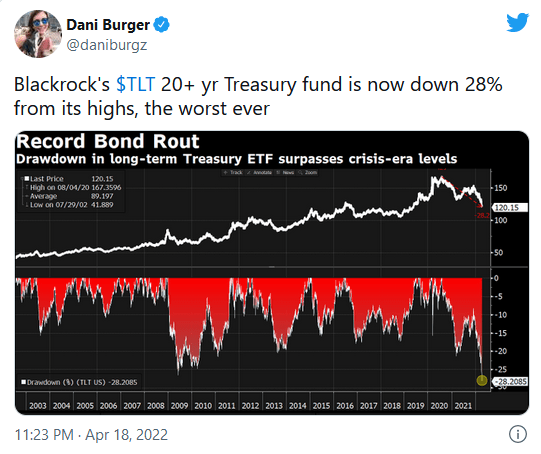

Twitter Twitter

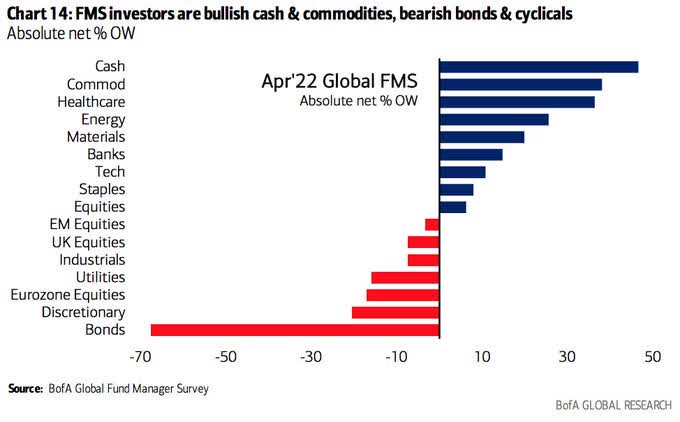

We have now come to a point where the market has priced in more rate hikes than are likely to occur. As a result, we believe (regarding yields) that either a) the rate of change will grind to a halt, or more likely b) reverse. Once bonds get bid it will be an abrupt rotation as no one is positioned for it:

BofA

Everything they’ve been crowding into will get sold down. Everything they’ve been puking out will get bid. So if you want to know when the tide will turn, WATCH BONDS – then buy what no one has wanted of late (Biotech, China Tech, Value Tech).

Marko Kolanovic of JP Morgan nails this concept in his Wednesday note:

J.P. Morgan

In last week’s “Peak Everything” article we drilled down on CPI and inflation. This week we started to see some more favorable data points:

BofA

CNBC

I laid out the case in extensive detail on CNBC Squawk Box-ASIA on Tuesday. Thanks to Ginny Goh, Martin Soong, Will Koulouris, Naman Tandon and Audrey Tay for having me on. Full 13-minute segment (Banks, Biotech, China Tech, Elon Musk, Twitter).

Here were my show notes for the segment:

-Earnings: Banks and Netflix (TECH)

-PROFIT SLUMPS: BAC Net income was $7.1 billion, 12% lower than for the first quarter of 2021. JPMorgan Chase (JPM) posted a 42% slump, while Wells Fargo (WFC) had a 21% drop.

–BAC – Beat: credit quality increased: Net loan charge-offs dropped 52%.

–JPM (only MC to miss top and bottom line) boosted reserves to brace for inflation and the war in Ukraine amid a sharp drop in deal activity.

–WFC grew its loan business by 2%, said the bank’s earnings will likely gain traction in the next two quarters on higher interest rates.

–GS: Investment banking business -36% (Ukraine/Omicron). Good trading (fixed income).

–Citi posted better-than-expected net interest income and trading, which offset higher expenses.

–TSM – The overall net profit margin in the Semiconductors and Semiconductor Equipment subsector hit 27.79% in 2021, 2 percentage points higher than at any point in the previous decade, and is expected to near 30% in 2022. Taiwan Semi predicted a gross profit margin of 56% to 58% in the June quarter. That’s up from 55.6% in the March quarter.

-Expect mild recession next year

Bad News: 2/10 spread inverted in recent weeks which likely means we will have a shallow recession in mid to late 2023.

Good News: Stock Market can still work up to new highs in coming months.

Why? Just as stimulus hits economy on a lagged basis (6-12 months after it starts), the same is true with tightening.

Earnings Estimates still going UP S&P 500: from $225 to $228.49 in ~last couple of months.

Inversions are BUY signals:

–Since 1977, there have been eight yield curve inversions. The S&P 500’s average return in the following year was +11.5%, with dividends +15.2%. Inversions are not a good signal to short stocks.

-The last four times the 2/10 yr yield curve inverted shows the S&P 500 rallied for another 17 months and gained 28.8% until the ultimate peak.

-Biotech

What to do given the likelihood of a shallow recession in 2023?

-Enter sectors that:

1) have reasonable valuations, and

2) can thrive in a slowing growth environment and have low correlation to GDP. GDP will slow from 5.9% 2021 to ~3.5-4% 2022.

Biotech (ETF: XBI – play a basket) Fits the Bill:

-XBI was up ~140% over the last “tightening cycle” (2016-2018) following a similar ~50% drawdown in 2015 like we just saw in last 12mo.

-Biotech valuations are historically low (relative to their average multiples since 1986). Implies the sector should appreciate:

~24% – to get back to average Price to Book multiple.

~155% – to get back to average Price to Operating Cash Flow multiple.

~112% – to get back to average Forward P/E multiple.

-16% of components of XBI trading at 2x cash on balance sheet or less.

-Many trading at a discount to cash on balance sheet.

-Lowest price/sales ratio in over a decade.

2 Catalysts:

- Doctor visits, screenings and scripts are accelerating as Covid winds down. Sales Reps are back on the road meeting with Doctors in person.

- M&A The cash balance of Russell 3000 Health Care companies exceeds $500B. This is up ~400% in the past 20 years. With Big Pharma losing their patents on many blockbuster drugs, but having tons of cash on their balance sheets, they will be forced to aggressively BUY innovation in the Biotech sector to maintain/accelerate growth.

-Buy US homebuilders?

-Too early to buy homebuilders – despite the fact valuations have come down. Need more time to consolidate as interest rate concerns have hit the sector. Revisit in a few months on weakness.

-Interest rate fears overblown as tightening cycle began in June 2004 and housing accelerated until 2007.

-72M millennials ~31 avg. age starting housing formation. Demand will persist. Starter houses may get smaller. Exurbs/remote work more affordable.

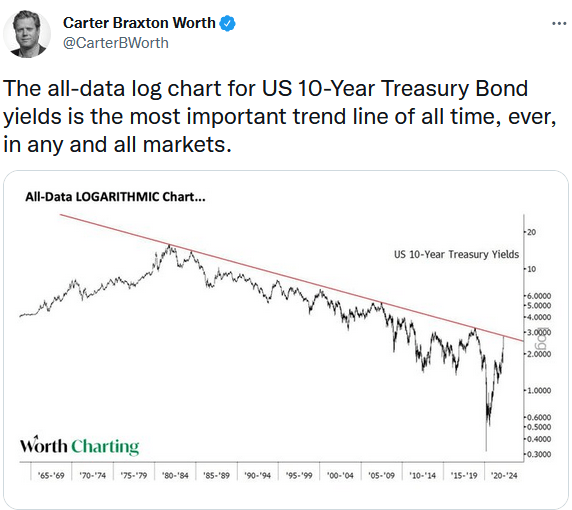

-Doesn’t buy bonds but thinks bonds will rally from April to Oct

-US 10yr Treasury yields are becoming too attractive to foreign buyers at these levels. One can borrow in yen or euros and mint money buying our Treasuries at these levels. I think we’re at a “sell the (Quant Tightening) rumor, buy the news” point in time.

-Treasury issuance will decline in coming months as receipts from income tax are used to fund government. Seasonality: This is one of the reasons that bonds outperform from April to October (on average last 20 years)

Any relief in yields will begin to favor that which no one is currently positioned for: 1) biotech, and 2) value (low multiple) tech. Out of Crowded Trade: Commodities/Cyclicals

-Buy China? Shutdown/Crackdown won’t last forever

-While the rest of the world is tightening policy, China is the only developed country that has been AGGRESSIVELY easing.

-As the shutdowns ease, the impact of the policy will begin to show up meaningfully in the economy – as we are now approaching six months since inception of the policy pivot. GDP was up 4.8% Q1.

-Hang Seng trading at a discount to book value. Did this 4x in past before REBOUNDS:

1998: 156.46% in 17 months

2008: 110.77% in 21 months

2016: 82.52% in 23 months

2020: 35.99% in 11 months

Alibaba more than doubled index returns during these periods:

-234% in 2016-2017

-70% in 2020

China Tech has been the least loved sector globally for months. That’s about to change. “The last shall be first.” As always, opinion follows trend. No one wanted BABA at $75. EVERYONE will want it again at $250.

Alibaba should grow Revenues and Earnings by >~30% each over next two yrs.

-I can buy it at a multiple that is 1/2 the S&P with ~2x the growth.

–Reminds me of Microsoft in 2013 before it took off on a historic run.

From 2006-2013 (7 years), Microsoft grew –

- Revenues (per share) by 112.14%

- Cash Flow (per share) by 193.05%

- Earnings (per share) by 120.83%

Next nine years up ~1,500%.

From 2014-2021 (7 years), Alibaba grew –

- Revenues (per share) by 894.93%

- Cash Flow (per share) by 559.46%

- Earnings (per share) by 601.92%

Alibaba’s stock has done nothing. You can buy at 2014 prices.

Stimulus: MSCI China up 31% on avg 12 mo. leading into CNC.

CGTN America

On Wednesday evening I joined Mike Walter on CGTN America (Global Business). Thanks to Mike and Kamelia Kilawan for having me on to discuss Tesla earnings, Elon Musk and the deal for Twitter.

Here were my show notes for the segment:

Elon Musk is the Thomas Edison of our day. The hits just keep on coming….

Financial Results:

-Revenue: $18.8B vs. $17.8B Expected. +81% yoy.

-EPS: $3.22 adj. vs. $2.26 Expected.

-EBITDA adj: $5.02B v $1.84B yoy.

-Free Cash Flow up 7.6x yoy to $2.2B

-Operating Margin record 19.2% in Q1

-Automotive Gross Margins record 32.9%.

-Cash $18B of cash end of Q1

-Valuation trades at 96x forward earnings.

Delivery Results:

-Tesla delivered a record 310,000 vehicles Q1 2022. +68% from the 185,000 vehicles in Q1 2021.

-Tesla will produce more than 1.5M cars in 2022 despite production and supply chain issues.

-Tesla says they will achieve 50% annual growth in vehicle deliveries for the foreseeable future.

-Musk says $TSLA could grow deliveries by 60% this year.

-Musk says ‘growing very rapidly’, aspire to reach 20M cars per year.

-Not demand limited, production limited. Waiting lists are long.

*CUSTOMER DEPOSITS ROSE TO $1.125B Q1, UP FROM $925MM

Production:

-Factories have been running below capacity for several quarters as supply chain became the main limiting factor.

-Will see a record output of Giga Shanghai this quarter. It’s possible we may pull a rabbit out of our hat and Q2 vehicle numbers will be higher than Q1.

-Shanghai factory production will be similar in Q2 but rapidly increase in Q3 and Q4.

-Elon Musk expects factories in Texas and Berlin to expand down the line.

Future:

-Tesla to launch its robotaxi in 2024. Robotaxi doesn’t have a steering wheel or pedals. Fully autonomous.

-Robotaxi ride will cost less than a bus or subway ticket. Will be lowest cost per mile travel that consumer has ever experienced.

-Musk said to pay attention to “optimus,” robot: “Optimus Humanoid Robot ultimately will be worth more than our car business worth more than Full Self Driving.”

-Insurance: Next Quarter TSLA could be the largest insurer of Teslas. Working to get to 80% of Tesla customers that have access in three states that are open. Real time insurance score = safer driving. Premiums lower.

Twitter Bid:

-Bought 9.2% of Twitter.

-Made unsolicited offer $54.20 ($43B) to buy Twitter.

-Board adopted poison pill to prevent Musk from buying more than 15% in the open market, but has not yet rejected.

-Board has FAILED to deliver value to shareholders since IPO in 2013.

-Musk needs to show “funding secured.”

-Apollo and one other PE considering providing debt financing.

-Clean up “shadow banning”: A social media platform’s policies are good if the most extreme 10% on left and right are equally unhappy

-Twitter must update on deal April 28 when it reports earnings.

-Over the weekend, he tweeted “Love Me Tender,”

-Musk tweeted ‘_______ is the Night,’ a possible reference to F. Scott Fitzgerald novel ‘Tender Is the Night’: Tender Offer – direct to shareholders.

-Tender: approach Twitter shareholders directly to buy their stock at a specific price over a defined period.

-By taking the bid directly to Twitter investors in a tender offer, Mr. Musk could pressure the board to withdraw opposition and its poison pill if he garnered enough shareholder support.

-Deal gets done >$60. Maybe $64.20!

Now Onto The Shorter Term View For The General Market:

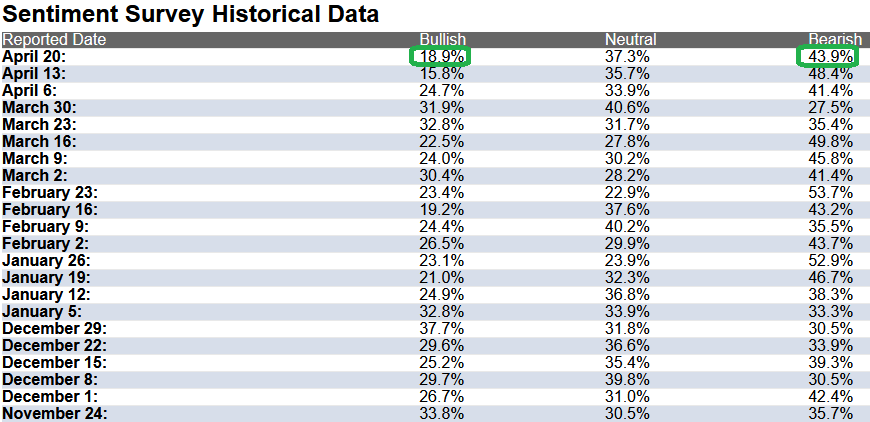

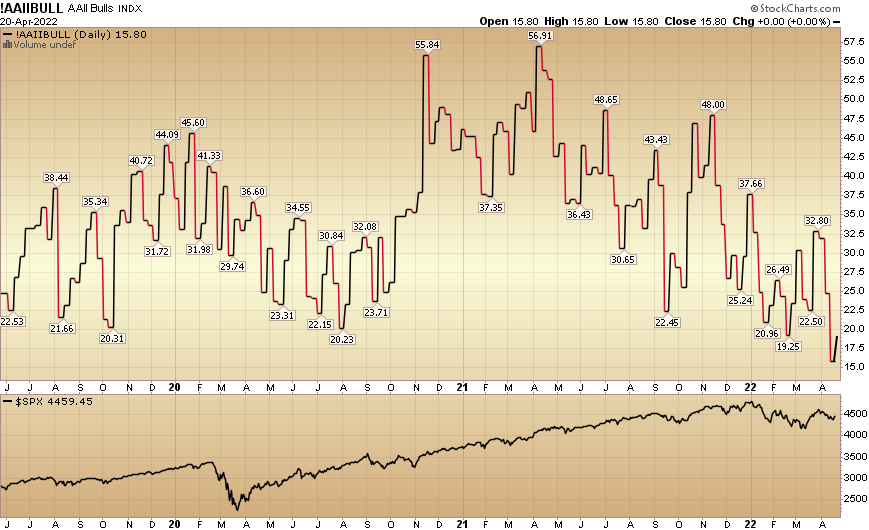

In this week’s AAII Sentiment Survey result, Bullish Percent (Video Explanation) ticked up to 18.9% from 15.8% last week. This is still near the most pessimistic sentiment in the history of the survey. Bearish Percent dropped to 43.9% from 48.4%. Retail investors are fearful.

AAII AAII

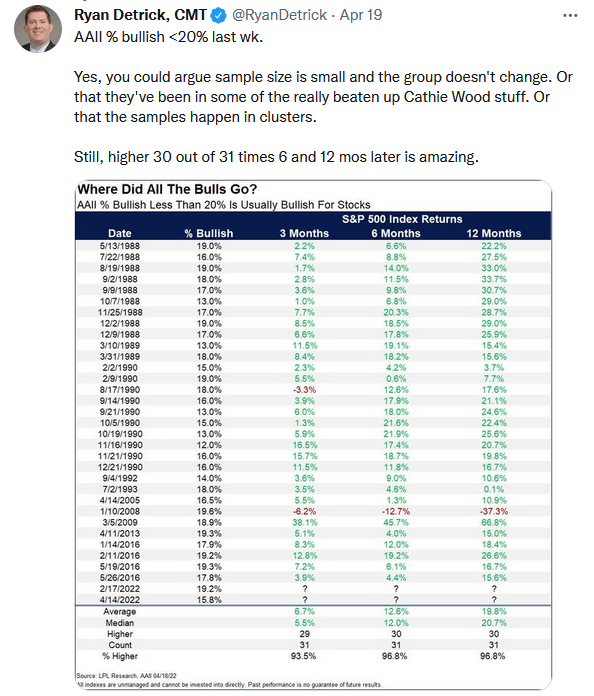

Last week’s “Bullish Percent” was the lowest in 30 years. Ryan Detrick of LPL pulled together some data the shows what can happen after sentiment becomes that pessimistic. If you can’t read the fine print, the color tells you everything you need to know:

Twitter

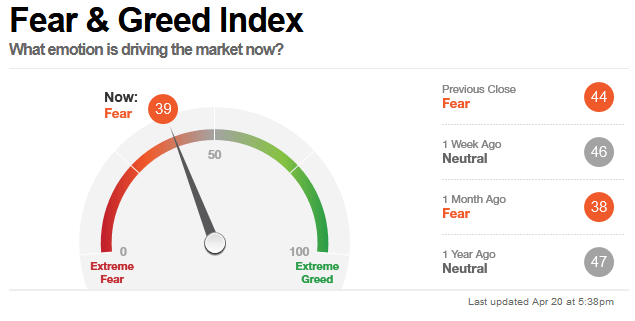

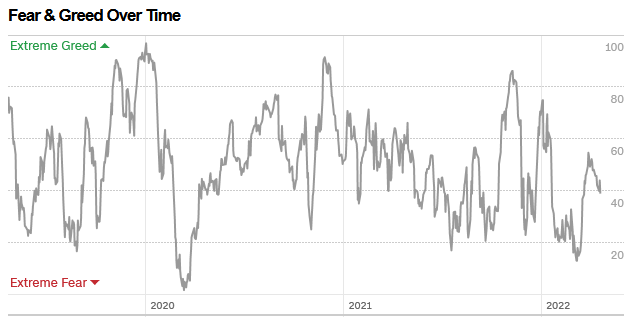

The CNN “Fear and Greed” Index ticked down from 46 last week to 39 this week. Sentiment is still cautious in the market. You can learn how this indicator is calculated and how it works here:

CNN CNN

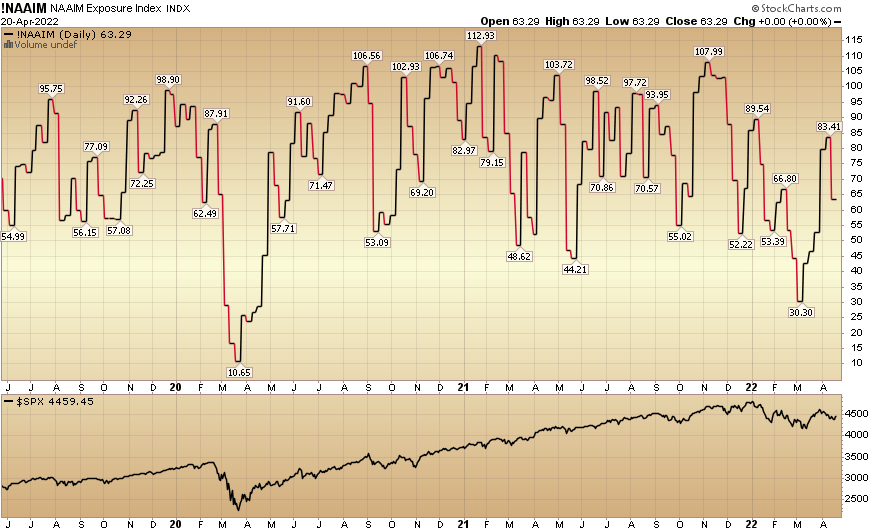

And finally, the NAAIM (National Association of Active Investment Managers Index) dropped to 63.29% this week from 83.41% equity exposure last week. Managers will have to chase any strength.

Stockcharts.com

Be the first to comment