skynesher/E+ via Getty Images

Description

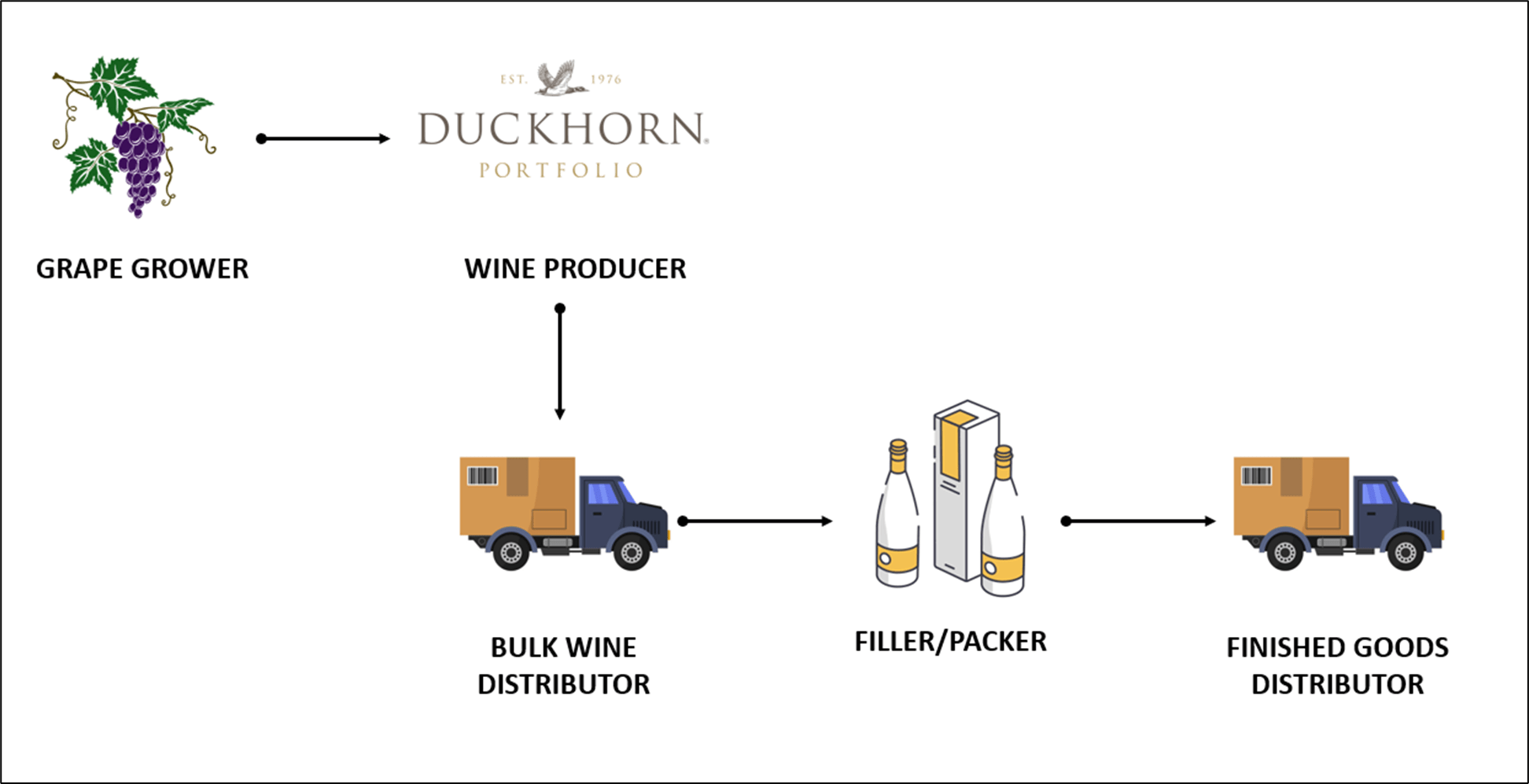

As stated in my previous article, The Duckhorn Portfolio, Inc. (NYSE: NYSE:NAPA) (the “Company”) is a producer of luxury wines (or wines sold for $15 or higher per 750ml bottle) with a solid supply chain but that presents some components that may be the cause of potential issues in the future and hence undermine the company’s operational performance.

Author’s Realization

Total Addressable Market (update)

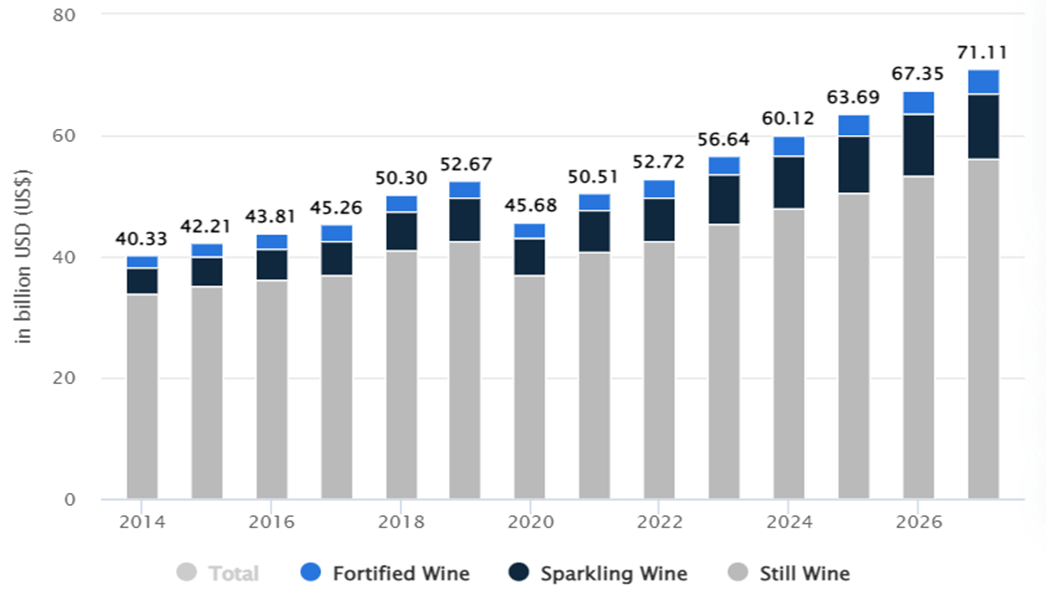

The Company keeps executing well and relative to the U.S. wine market (I decided to narrow the TAM to the U.S. vs previously assumed global TAM), holds a market share of ~ 0.71% 2022A (up from ~ 0.46% 2019A).

In fact, while the overall market grew at a CAGR of 0.0% over the 2019A-2022A period, the company’s revenue grew at a CAGR of 15.6% over the same period.

Statista

This is a positive trend that I expect to continue in the future driven by the premiumization and younger generations choosing wine over other types of alcohol.

Company Valuation

Valuation (update)

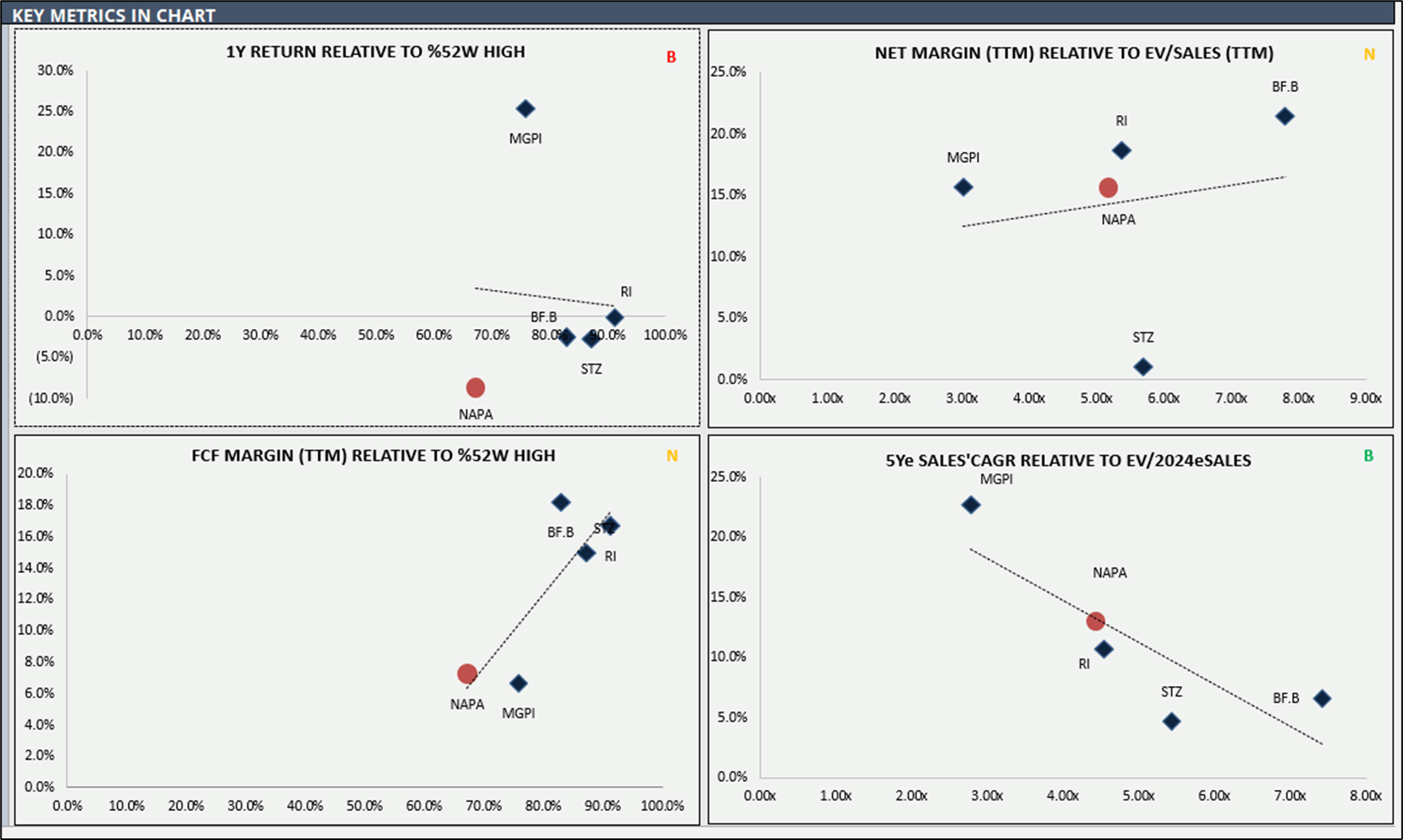

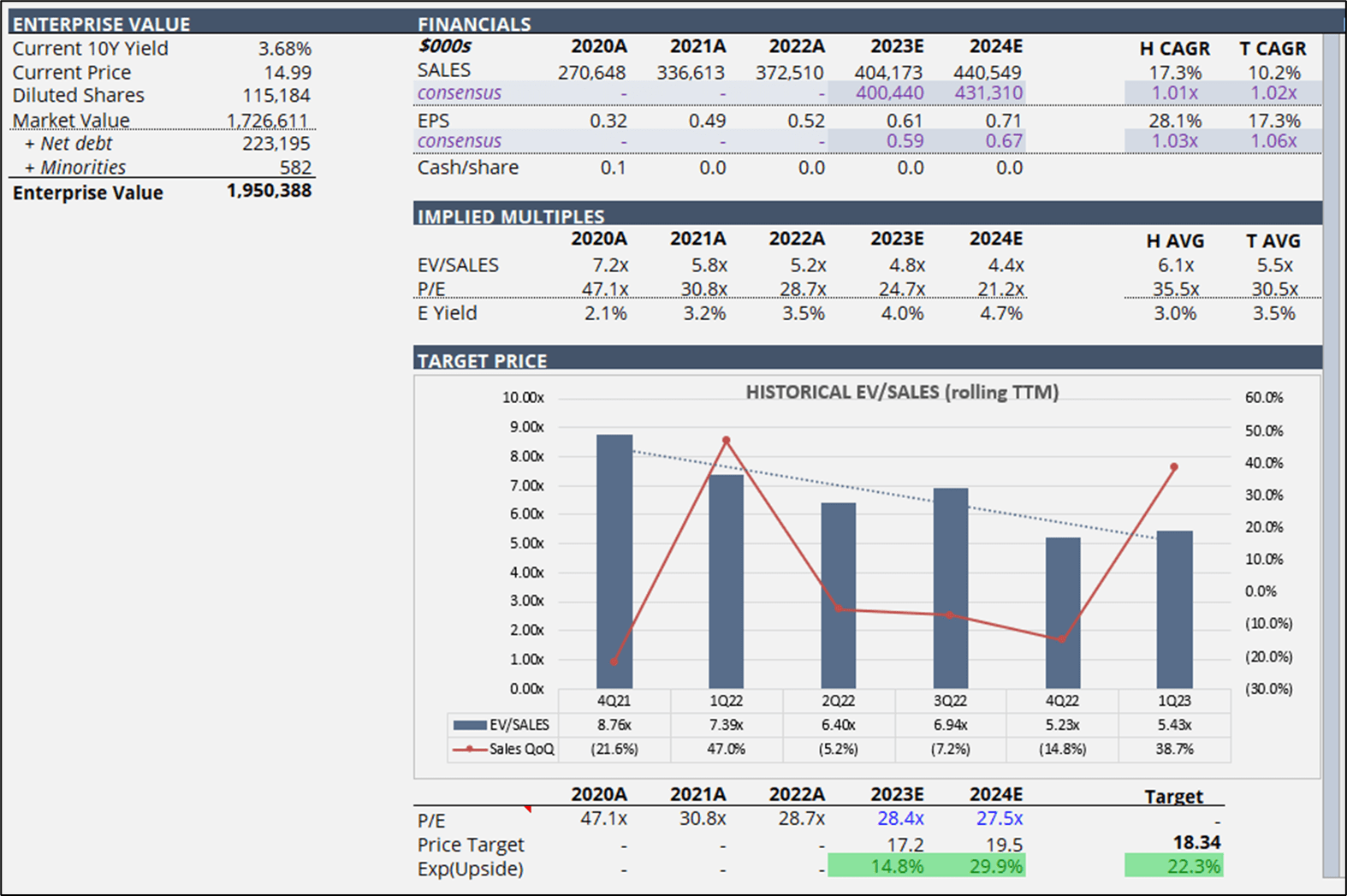

The company is trading at an EV/SALES of ~ 5.23x TTM, which is in line with the peers’ median EV/SALES of ~ 5.37x TTM.

Author’s Estimates

I believe that the company is undervalued on a fundamental basis.

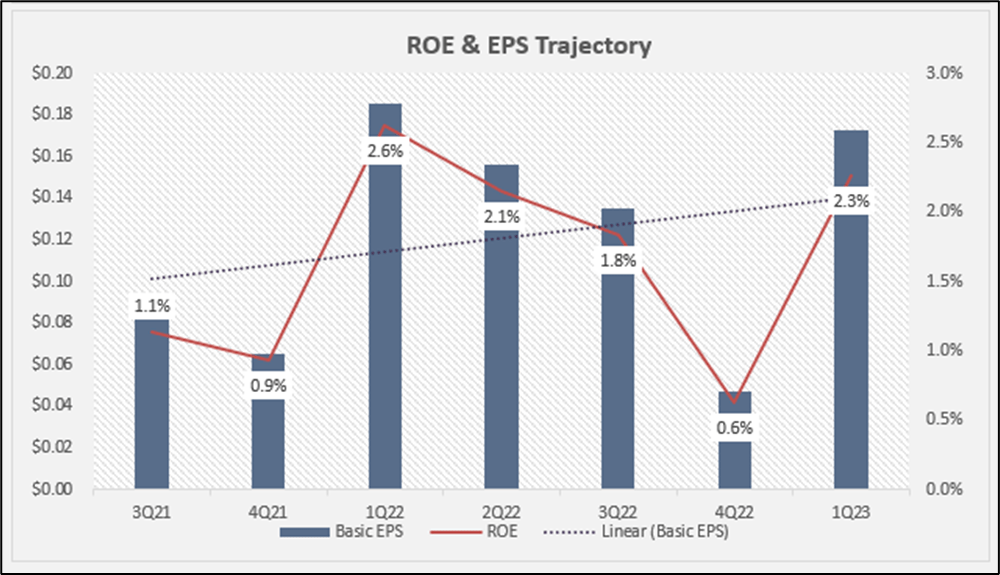

Personally, I do think that the management is doing a great job, and we can see it through two key metrics:

- Sales: sales CAGR over the last 3 years of ~ 18.0% driven entirely by volume (mostly by Duckhorn Vineyards and Decoy winery brands). Moreover, it is worth to note the company’s penetration rate in 2022A is ~ 21% up from ~ 19.0% in 2021A.

- Gross margins: effective management of the input costs. As stated during the 4Q22 earnings call:

We feel good with where we are right now. We’re able to offset our COGS inflationary increases. So we think we’re in a really good place and still very competitive within the luxury segment

Author’s Estimates

The balance sheet is healthy and interest-bearing debt doesn’t represent an issue given the company’s interest coverage ratio of ~ 12.0x TTM. However, expect the ratio to go lower since the interest rate swap used to hedge the exposure to interest rates will expire in March 2023. This will increase non-operating expenses and hence will put downward pressure on margins.

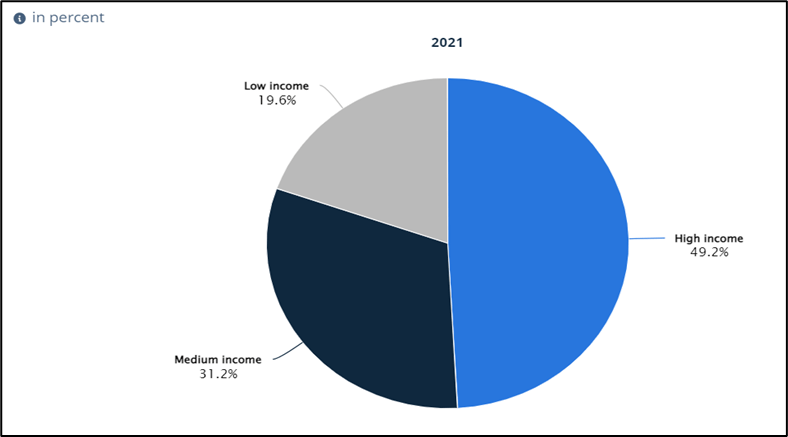

Overall, I keep seeing good reasons that make me willing to invest in this company. In fact, I believe that the company will be able to effectively navigate this economic slowdown through product quality and diversification, and the fact that sales growth is driven entirely by volume is sufficient proof of it. Nevertheless, it is important to underline that a recession will negatively affect all the companies notwithstanding the industry they operate in, however, the good news here is that, historically, the luxury segment provides a better hedge again an economic slowdown since the consumers are less likely to be squeezed.

Below you can see wine consumers by income (the chart clearly supports the above statement).

Statista

Having said that, and in line with the current macro environment and company-related trends, I expect the company to keep executing well and notwithstanding macro-headwinds, I do see an expansion on the bottom line.

Author’s estimates

In terms of downside risks, here are a few:

- Competition, In the U.S., the wine industry is relatively concentrated among a small number of players and such intense competition may adversely affect the company’s top-line growth. If the competition will be perceived as being a key driver of slower growth, it would negatively affect the company’s share price.

- Recession, historically, the wine sector performed very well notwithstanding the recessionary period, however, with low-income customers being squeezed and medium-income starting to, a hard landing may adversely affect the company’s operating performance.

- Natural Disasters, agricultural risks, water availability (this is very important in my opinion), wildfires, floods, disease, and pests could adversely affect the quality and quantity of grapes and thus adversely affect the company’s operating performance.

Final Remarks

I rate shares as BUY with an estimated fair value of $18.34/share, which would represent a 22.3% upside from the current price of $14.99.

What am I doing personally? Having said that, I must admit that my timing when I first recommended the company was bad, and like many of you I had to intervene through active trading to keep the return positive on the name.

I am looking to build back my position but this time I will start building ~ $15.0/share as I prefer to have a larger cushion of protection vs my fair value.

Be the first to comment