Investment case

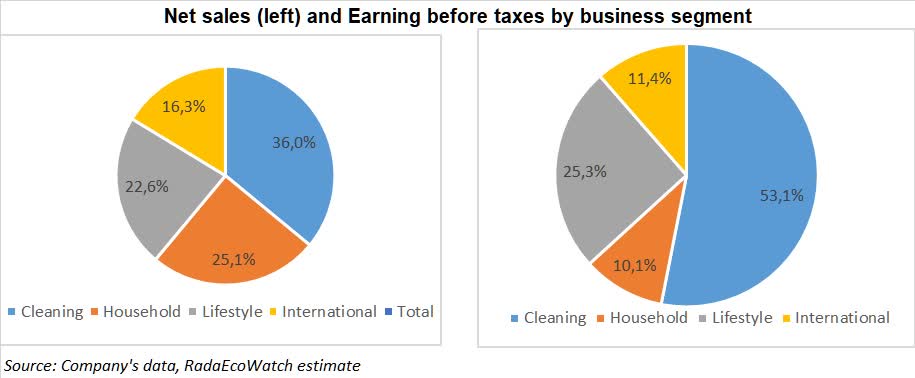

The Clorox company (NYSE:CLX) is a leading multinational manufacturer and marketer of consumer and professional products, which operates in four main area: cleaning, household products, lifestyle and international. As indicated by 2019 annual report, Cleaning is the largest and more profitable area of the company, with 36% of revenue and 53.1% of earning before taxes. Households represents 25.2% of revenue but only 10.1% of EBT as profitability has been penalized by the strong competition in the segment and by the recent losses of market share. Lifestyle has a share of 22% of revenue and 25.3% of EBT and, in our view it is the area with the best outlook in a medium-term scenario. Finally, International represents 16% of revenue but only 11% of EBT.

{kind=link}

Since January 29 the stock has outperformed the S&P500 by a wide margin: +9.7% against -5%.

We think that the overperformance is mainly due to investors’ concern on the impact of coronavirus disease on global economic outlook. In our view, investors treated Clorox a safe haven as:

- The strong presence in the cleaning industry (36% of revenue and 53% of earnings before taxes). The coronavirus outbreak could increase the demand of the company’s products in the segment to sanitize and disinfect houses and offices.

- The company obtains close to 85% of its revenue in the USA and it is only marginally exposed to a strong weakening of other countries’ economies.

- Clorox’s solid track record of dividend payment as the stock is included in the S&P aristocratic index having increased the annual dividend for at least 25 consecutive years. The current 2.5% dividend yield is attractive considering the 1% 10 years government bond yield.

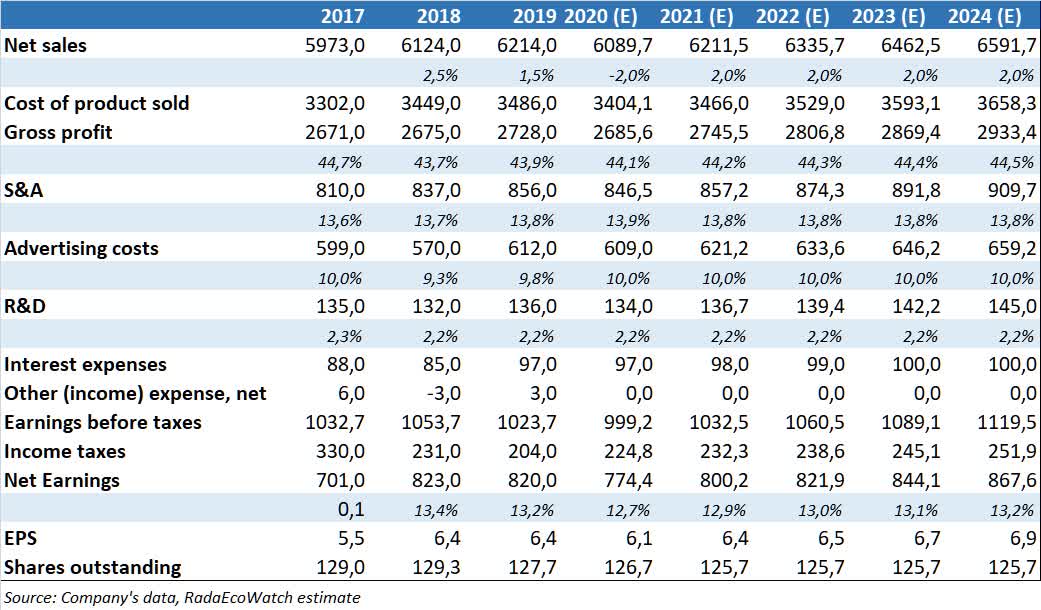

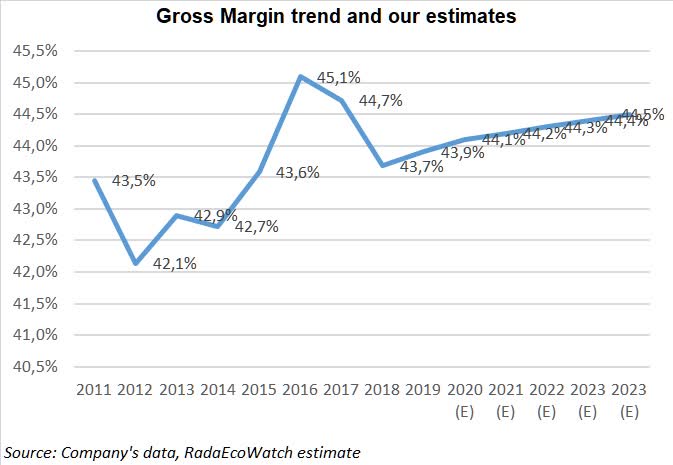

- On the company front, latest results confirmed the gross margin expansion and solid free cash flow generation that the management had indicated in the “IGNITE strategy“. In Q2 ’20 Gross margin rose by 40 basis points to 44.1% from 43.7% in the year-ago quarter despite the 2% revenue decline (flat at unchanged forex).

However, we think that the Clorox stock price upside potential from current value is limited as:

- Following the recent upward trend the stock is traded at historically high multiple valuation: P/E 2020 of 25.4x considering the high end of USD6.10/6.25 EPS range indicated by the company. At our estimate of a 6.11 EPS in 2020, the stock is trading at 26.1x 2020 P/E.

- Clorox management guided for a modest revenue growth in a medium-term scenario (zero/+2% in organic term in 2020 versus a medium term target of +2/4%). In this scenario, Ebit expansion would depend only by gross margin expansion, which will become harder to achieve going forward. According to our estimates, gross margin should rise to 44.1% in 2020, above the last 10-year average of 43.6%. We estimate a further improvement to 44.2% and 44.3% in 2021 and 2022 respectively. However, we thing that going forward a further improvement of gross margin would harder to achieve.

- Our DCF model returns an USD143.2 target price. It represents a 17% downside potential from Wednesday closing price (USD173.4).

In this scenario, we would not add Clorox to our portfolio now. In our view, only a decline of the stock to USD140 area would create a BUY opportunity.

Why the stock is on fire?

Clorox has enjoyed a solid upward trend year to date, rising by 12.4% to USD172.3. While the stock has underperformed the U.S. market at the beginning of the year, the trend reversed over the last month and especially during the last week sell-off. Since January 29, Clorox has advanced by 9.7%, while the S&P500 declined by 5%.

We think that Clorox overperformance depends from:

- The strong presence in the cleaning segment. As we indicated in the “investment case” section, this is the largest segment with 36% of revenue and 53% of earnings before taxes. In Q2 ’20, cleaning sales were flat and pre-tax earnings increased by 9%. The coronavirus outbreak could increase the demand of the company’s products in the segment to sanitize and disinfect houses and offices. In this scenario, segment sales could accelerate in H2 ’20, further pushing up marginality.

- The company obtains close to 85% of its revenue in the USA and it is only marginally exposed to a strong weakening of other countries’ economies.

- Clorox’s solid track record of dividend payment as the stock is included in the S&P aristocratic index having increased the annual dividend for at least 25 consecutive years. Annual dividend rose from USD1.88 in 2009 to USD3.94 in 2019, a 7.7% CAGR. The current 2.5% dividend yield is attractive considering the 1% 10 years government bond yield.

- On the company front, latest results confirmed the gross margin expansion (+175bp expected) and solid free cash flow generation (11-13%) that the management had indicated in the “IGNITE strategy” presentation.

Why we do not share the optimism on the stock

However, we do not think that the recent optimism on the company is justified.

- Following the recent upward trend, the stock is trading at 26x expected 2020 P/E according to our estimates on 2020 EPS. It is higher than the last 10 years average of 23.4x. While higher multiples are justified by record low government bond yields, we see little space to a further multiple expansion in the short term. According to our EPS estimates, at current stock price the P/e would return lo long term average in 2024.

- Latest results confirmed that the company has difficulties in growing revenue at a solid pace. Q2 ’20 revenue declined by 2% and organic revenue were flat. Revenue trend was well below the medium target of +2/4%. While gross margin improved by 40bp (from 43.7% to 44.1%) we think that for the company would be tough to continue increasing the bottom line only with an expansion of marginality. According to our estimates, gross margin should rise to 44.1% in 2020, above the last 10 years average of 43.6%. We estimate a further improvement to 44.2% and 44.3% in 2021 and 2022 respectively.

- Finally, we value the company with a DCF model (look at the following paragraph for more details). It returns a stock valuation well below Friday’s close price, signaling little possibilities for a continuation of the recent upward trend.

Valuation

We valued Clorox using a DCF based on the following assumptions:

- Ebit growing at 1.7% CAGR in the period 2019/2024.

- Capex of 3.4% of sales, in line with 2017-2019 average;

- A negative contribution from working capital and other voices (i.e. stock based compensation) as indicated in following table;

- WACC of 5.6%. We assumed a 90/10% Capital/Debt mix, with a 6% cost of equity (1.12% 10 year government bond yield +0.8 Beta and 6% equity risk premium) + a 3.1% cost of debt, as indicated by the company;

- A prudential perpetual growth rate of 1.5%.

We derive an USD143.2 per share target price. It represents a 17% downside potential from Wednesday closing price at USD173.4. At our target price, the stock would trade at 23.4x 2020 P/E and 22.7x 2021 P/E.

Conclusion

Clorox stocks have been on fire recently as investors saw the in the company a safe haven for the strong presence in the cleaning industry, the low exposure to international markets, the better than expected Q2 ’20 results and the solid track record of dividend payment. However, we think that the stock is expensive according to both multiples analysis and our DCF model. Moreover, company’s low revenue growth could weigh on margin expansion going forward.

In this scenario, we would not add Clorox to our portfolio now. In our view, only a decline of the stock to USD140 area would create a BUY opportunity.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment